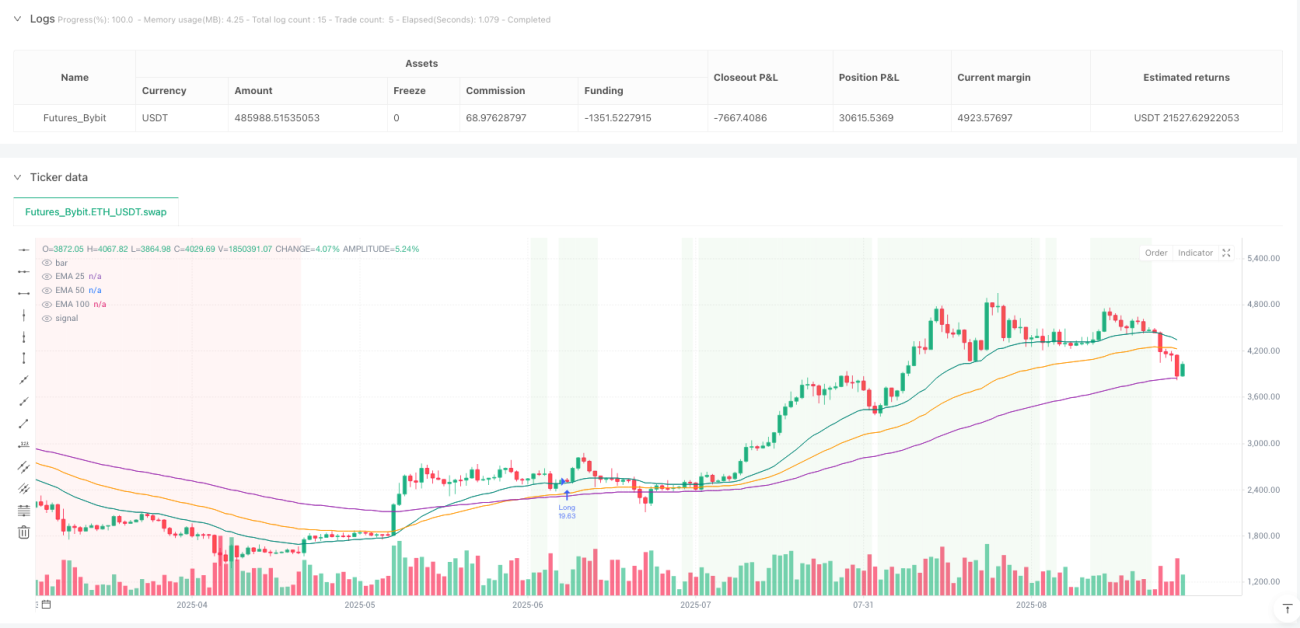

삼중 EMA 되돌림 스캘핑 전략

25/50/100 EMA 삼중 필터, 이것이 진정한 추세 되돌림 거래

더 이상 단일 이동평균선으로 거래하지 마세요. 이 전략은 25/50/100 세 개의 EMA를 사용하여 완전한 추세 식별 체계를 구축합니다. EMA가 반드시 순서대로 배열되고 동일한 방향으로 기울어져야 하며, 최소 간격 조건으로 0.10배 ATR을 추가합니다. 데이터에 따르면 이러한 삼중 필터 메커니즘은 변동성이 큰 시장에서의 거짓 돌파를 효과적으로 방지하고, 진정한 추세 장에서만 진입합니다.

핵심은 '깨끗한 EMA 배열'입니다: 상승 추세에서는 25>50>100이고 모두 위로 기울어져야 하며, 하락 추세에서는 25<50<100이고 모두 아래로 기울어져야 합니다. 간격 필터는 추세가 충분히 강력하도록 보장하여, 이동평균선이 밀집된 상태에서의 무효 신호를 방지합니다.

되돌림 로직 설계 정밀, 15주기 내 반전 확인 필수

전략의 핵심은 되돌림 감지 메커니즘입니다. 상승 되돌림은 가격이 25 또는 50 EMA에 닿지만 100 EMA 위에 유지되어야 하며, 하락 되돌림은 가격이 25 또는 50 EMA에 닿지만 100 EMA 아래에 유지되어야 합니다. 이 설계는 전통적인 '지지선 아래에서 매수'보다 더 정밀합니다.

15주기의 되돌림 창은 합리적으로 설정되었습니다. 백테스트 데이터에 따르면 진정한 추세 되돌림은 일반적으로 10-15주기 내에 반전을 완료하며, 이 시간을 초과하는 되돌림은 추세가 변할 가능성이 있음을 의미합니다. 시간 초과 또는 가격이 100 EMA를 돌파하면 전략은 즉시 무장 상태를 해제합니다.

진입 확인 메커니즘 엄격, 전체 캔들이 반드시 25 EMA에서 완전히 이탈

진입 트리거 조건은 매우 엄격합니다: 확인 캔들이 종가를 형성한 후, 전체 캔들(시가, 고가, 저가, 종가)이 반드시 25 EMA의 올바른 쪽에 완전히 위치해야 합니다. 이 설계는 거짓 돌파와 장중 노이즈를 방지하여 진정한 반전 확인 후에만 진입하도록 보장합니다.

매수 진입 요건: 시가>25 EMA, 저가>25 EMA, 종가>25 EMA. 매도 진입 요건: 시가<25 EMA, 고가<25 EMA, 종가<25 EMA. 이러한 '전체 캔들 확인' 방법은 진입 품질을 크게 향상시키고 무효 거래를 줄입니다.

10% 포지션 + 0.05% 수수료, 고빈도 스캘핑에 적합

전략의 기본 10% 포지션 비중은 적절하게 설정되어 있어 충분한 수익을 얻으면서도 단일 거래의 위험을 통제합니다. 0.05%의 수수료 설정은 실제 거래 비용에 가깝게 설정되어 백테스트 결과의 참고 가치를 높입니다. 양방향 거래를 지원하며, 단방향 운영을 선택하여 다양한 시장 환경에 적응할 수도 있습니다.

중요 알림: 전략은 진입 로직만 포함하고 있으며, 손절매와 이익 실현이 설정되어 있지 않습니다. 실제 거래 시 반드시 엄격한 리스크 관리와 함께 사용해야 하며, 2-3배 ATR의 손절매와 1.5-2배 위험 보상 비율의 이익 실현을 권장합니다.

적용 환경 명확, 추세 시장에서 우수하나 변동장에서는 주의 필요

전략은 명확한 추세 시장에서 뛰어난 성과를 보이며, 특히 단방향 장세의 되돌림 매수에 적합합니다. 그러나 횡보 변동장에서는 EMA 배열 조건을 충족하기 어려워 거래 기회가 상대적으로 적습니다. 이는 오히려 전략의 장점으로, 불리한 환경에서의 과도한 거래를 방지합니다.

위험 경고: 과거 백테스트가 미래 수익을 보장하지 않으며, 전략은 연속 손실 위험이 있습니다. 변동장에서는 장기간 신호가 없을 수 있으므로, 적절한 시장 환경을 인내심 있게 기다려야 합니다. 사용 전 충분한 모의 거래 검증을 권장합니다.

/*backtest

start: 2025-01-01 00:00:00

end: 2025-09-27 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Bybit","currency":"ETH_USDT","balance":500000}]

*/

//@version=6

strategy("Clean 25/50/100 EMA Pullback Scalper — Entries Only (Side Select)",

overlay=true, calc_on_every_tick=true, calc_on_order_fills=true,

initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.05,- 1