🎯 이게 무슨 전략이지? 20개 지표가 총출동!

아시나요? 이 전략은 마치 내 거래에 초지능 AI 어시스턴트를 붙인 것과 같습니다! 동시에 20개의 다양한 시장 신호를 모니터링하고, 대부분의 지표가 "괜찮다"고 말할 때만 거래 신호를 줍니다. 마치 집을 살 때 입지, 가격, 평형, 교통... 모든 면이 마음에 들어야 결정하는 것과 같죠!

강조! 이건 평범한 단일 지표 전략이 아니라 '다차원 공진 시스템'입니다. 한 친구만 주식이 좋다고 하면 반신반의할 수 있지만, 20명의 전문가 친구들이 모두 좋다고 하면 더 확신이 생기지 않나요?

📊 핵심 무기고 대공개

추세 식별 삼총사 🗡️

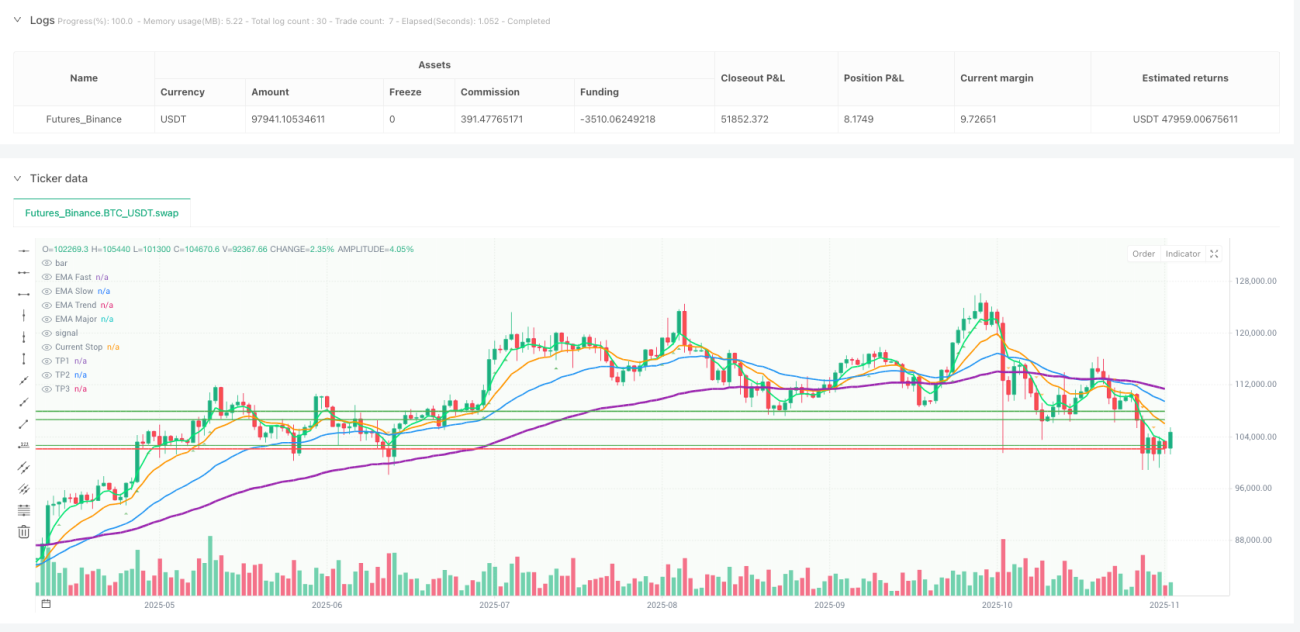

- 빠른 EMA(5) vs 느린 EMA(13): 단기 추세 전환 포착

- 추세 필터 EMA(34): 중기 방향 확인

- 주 추세 EMA(89): 큰 방향 파악, 작은 변동에 흔들리지 않음

다중 시간 프레임 분석 ⏰

이 기능 정말 좋아요! 전략이 1시간과 4시간 추세를 동시에 보는데, 운전할 때 앞길만 보는 게 아니라 내비게이션 전체 경로도 보는 것과 같습니다. '단기 시간 프레임에서는 상승, 장기 시간 프레임에서는 하락'이라는 난처한 상황을 피할 수 있어요!

스마트 리스크 관리 🛡️

- 동적 포지션 조정: 시장 변동성에 따라 베팅 크기 자동 조절

- 분할 이익 실현: 욕심내지 않고 일부는 좋을 때 챙기기

- 트레일링 스탑로스: 수익 보호의 신

🔥 20중 보험의 거래 로직

매수 신호 조건:

- 추세 상승: 모든 EMA가 상승 배열

- 모멘텀 충분: RSI, MACD, 스토캐스틱 RSI 모두 청신호

- 거래량 동반: 거래량 동반 상승이 진짜 상승

- 시장 구조 양호: 고점 계속 상승

- 유동성 지지: 주요 지지선 유지

매도 신호는 정반대!

함정 피하기 가이드 ⚠️: 전략에 '볼린저 밴드 압착 감지'가 있어 시장이 너무 조용할 때 거래를 중단함으로써 횡보장에서 휘둘리지 않도록 합니다!

💰 수익 극대화의 비밀 무기

분할 이익 실현 전략 📈

- 첫 번째 이익 실현: 위험 대비 수익 2배일 때 30% 포지션 매도

- 두 번째 이익 실현: 3.5배일 때 40% 추가 매도

- 남은 포지션: 트레일링 스탑로스로 보호하며 수익을 극대화

스마트 스탑로스 업그레이드 🎯

2.5배 수익 달성 후 스탑로스가 자동으로 원가로 이동하여 이 거래가 최소한 손해 보지 않도록 합니다. 마치 수익에 보험을 든 것과 같죠!

동적 트레일링 스탑로스 🏃♂️

수익이 일정 수준 이상이면 스탑로스가 그림자처럼 가격을 따라 움직이며 수익을 보호하면서도 상승 여지를 남깁니다.

🚀 이 전략이 이렇게 대단한 이유는?

- 전방위 커버: 기술적 분석, 자금 관리, 리스크 통제 하나도 빠짐없음

- 스마트 필터링: 20개 조건이 단계별로 선별하여 성공률 대폭 향상

- 적응성 뛰어남: 다중 시간 프레임 분석으로 다양한 시장 환경에 적합

- 인간 친화적 설계: 자동 실행으로 감정적 거래 방지

이 전략은 노련한 트레이딩 팀을 코드로 옮겨놓은 것과 같아서, 24시간 쉬지 않고 최적의 거래 기회를 찾아줍니다!

/*backtest

start: 2024-11-12 00:00:00

end: 2025-11-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('Amir Mohammad Lor ', shorttitle='MPF', overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=15, pyramiding=0, max_bars_back=1000)

// === INPUTS ===- 1