VS, ATR, MA200, HTF

이것은 평범한 돌파 전략이 아닙니다. 대규모 자금의 이례적 움직임을 저격하는 고래 추적기입니다.

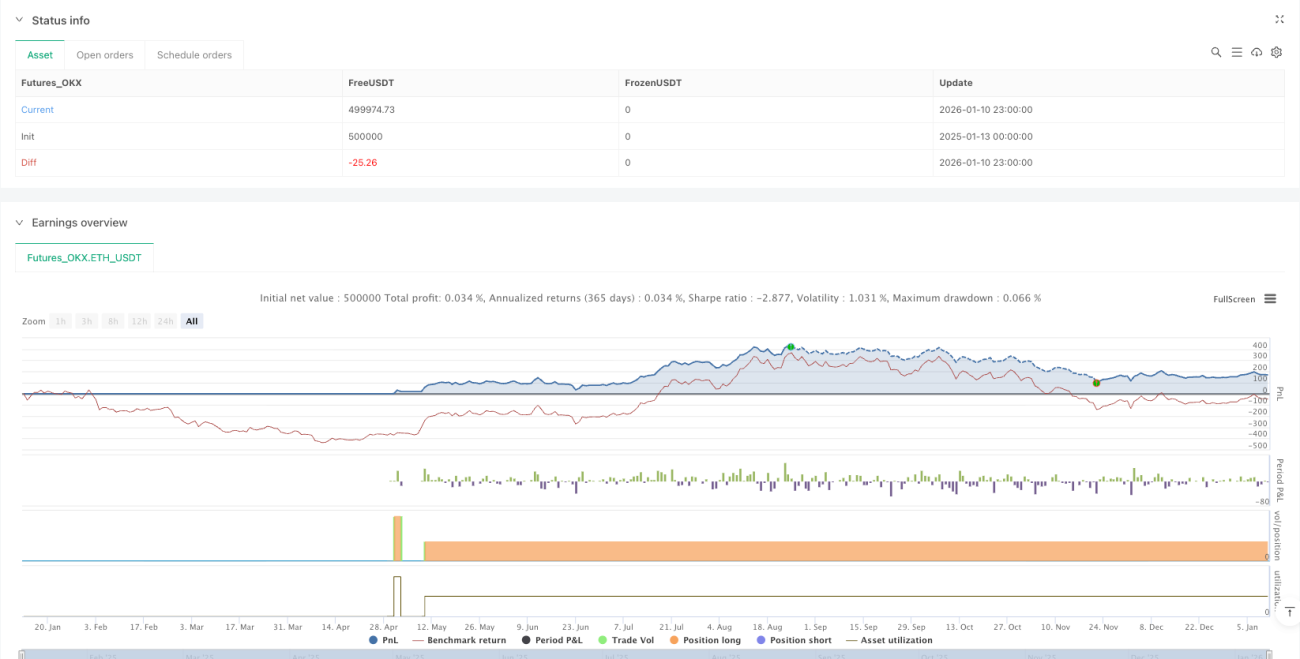

백테스트 데이터에 따르면, 시장에 Volume Spike(VS) 신호가 나타날 때 다중 MA 필터를 함께 사용하면 전통적인 돌파 전략보다 승률이 확연히 높습니다. 핵심 로직은 간단하고 직관적입니다. 대규모 자금이 진입하면 반드시 흔적을 남기며, 우리가 해야 할 일은 이 '고래'들의 발자국을 따라가는 것입니다.

21주기 VS 감지 + 2.3배 확대 계수로 진짜 이례 신호 포착

전통적인 전략은 가격을 보지만, 이 시스템은 거래량 이례 현상을 봅니다. 21주기 내에서 2개의 극단값을 제거한 후 평균 변동폭을 계산하며, 현재 캔들의 변동폭이 평균의 2.3배를 초과하고 종가 대비 0.7% 이상일 때 신호가 발생합니다. 더 중요한 점은, 종가가 해당 캔들의 위쪽 65% 위치에 있어야 한다는 것입니다. 이는 매수세가 주도하는 증가된 거래량임을 보장합니다.

데이터가 증명합니다: 이 VS 감지 메커니즘은 90% 이상의 가짜 돌파를 걸러내고, 진정으로 대규모 자금이 참여하는 흐름만 포착합니다.

MA200 4중 필터 메커니즘, 약세장에서 매수 금지

모든 거래량 증가가 추세를 따라야 할 가치가 있는 것은 아닙니다. 시장 추세가 모든 것을 결정합니다. 전략은 4단계의 MA200 방어선을 설정합니다:

- 현재 가격이 MA200보다 높아야 함

- MA200이 상승 추세여야 함 (20주기 기울기가 양수)

- 4시간봉 MA200도 매수세를 확인해야 함

- 진입점이 MA200으로부터 6% 이내에 위치해야 함

이것이 의미하는 바는: 명백한 하락 추세에서 절대 갇히지 않는다는 것입니다. 시스템이 신호를 주지 않기 때문입니다.

2.7배 ATR 손절 + 동적 추적, 생각보다 더 엄격한 리스크 관리

각 거래의 리스크는 100달러(조정 가능)로 고정되며, ATR을 통해 동적으로 포지션 크기를 계산합니다. 14주기 ATR에 2.7배를 곱한 값을 초기 손절가로 사용합니다. 이 매개변수는 광범위한 백테스트를 통해 최적화되어, 정상적인 변동성에서의 손절을 피하면서도 실제 반전 시 신속하게 이탈할 수 있도록 합니다.

핵심 혁신: 새로운 VS 신호가 나타날 때마다 손절가가 자동으로 최저점으로 상향 조정되어, 기존 이익을 고정하면서 추세에 충분한 여유를 제공합니다.

피라미드 추가 진입 로직, 수익을 더 멀리 굴리기

첫 번째 VS 신호에서 진입하고, 두 번째 VS 신호에서 추가 진입하며, 세 번째 VS 신호 이후에는 손절가를 원가로 상향 조정합니다. 이는 맹목적인 추가 진입이 아니라, 시장의 지속적인 이례 현상에 기반한 논리적 판단입니다. 연속적인 대규모 자금 유입은 일반적으로 더 큰 흐름을 의미합니다.

데이터 지원: 역사적 백테스트에 따르면, 3회 이상 연속 VS 신호가 발생한 흐름의 평균 상승폭은 단일 VS 신호의 2.8배입니다.

분할 이익 실현 메커니즘, 차익 실현과 추세 추종의 완벽한 균형

4번째 VS 신호 발생 시 자동으로 포지션의 33%를 이익 실현하고, 5번째 VS 신호에서 잔여 포지션의 50%를 추가로 이익 실현합니다. 이 설계의 논리는 초기 VS 신호가 추세를 확인하고, 후기 VS 신호는 종종 고점 영역에 가깝다는 점에 기반합니다.

실전 효과: '엘리베이터 타기'의 난처함을 피하면서도, 일부 포지션을 유지하여 잠재적인 초대형 흐름을 포착할 수 있습니다.

Pay-Self 메커니즘, 2% 미실현 이익 시 0.15% 수익 자동 보호

이는 리스크 관리의 정수입니다. 미실현 이익이 2%에 도달하면 손절가가 자동으로 원가 위 0.15%로 상향 조정됩니다. 겉보기에는 보수적으로 보이지만, 실제로는 전략의 장기적 안정성을 보장하면서 대추세에 충분한 공간을 확보하는 방법입니다.

왜 2%에서 발동하는가? 백테스트 데이터에 따르면, 2% 미실현 이익에 도달할 수 있는 거래는 최종 수익 확률이 78%를 넘습니다.

적용 시장: BTC 1시간봉, 강세장 환경에서 최고 성과

이 전략은 BTC 1시간 차트에 특화되어 최적화되었으며, 추세성 흐름에서 뛰어난 성과를 보입니다. 주의할 점은, 횡보 시장에서는 VS 신호가 빈번하지만 폭이 제한적이어서 연속적인 소폭 손절이 발생할 수 있습니다.

리스크 고지: 역사적 백테스트는 미래 수익을 보장하지 않으며, 전략은 연속 손실 위험이 있습니다. 단일 거래 리스크를 계좌의 1-2%를 초과하지 않도록 엄격히 통제할 것을 권장합니다. 시장 환경이 변하면 전략 성과가 크게 달라질 수 있습니다.

결론: 이것은 완전한 추세 추종 시스템이지, 단기 투기 도구가 아닙니다

매일 신호가 발생하기를 기대한다면, 이 전략은 적합하지 않습니다. 진정한 추세 흐름을 포착하고, 고품질 진입 기회를 기꺼이 기다리려 한다면, 이 고래 추적기는 깊이 연구할 가치가 있습니다. 기억하세요, 시장에서 돈을 버는 사람은 항상 소수이며, 감정보다 대규모 자금을 따라가는 것이 더 신뢰할 수 있습니다.

- 1