Strategi Pengurusan Modal Dinamik Multi-Faktor

Gambaran Keseluruhan

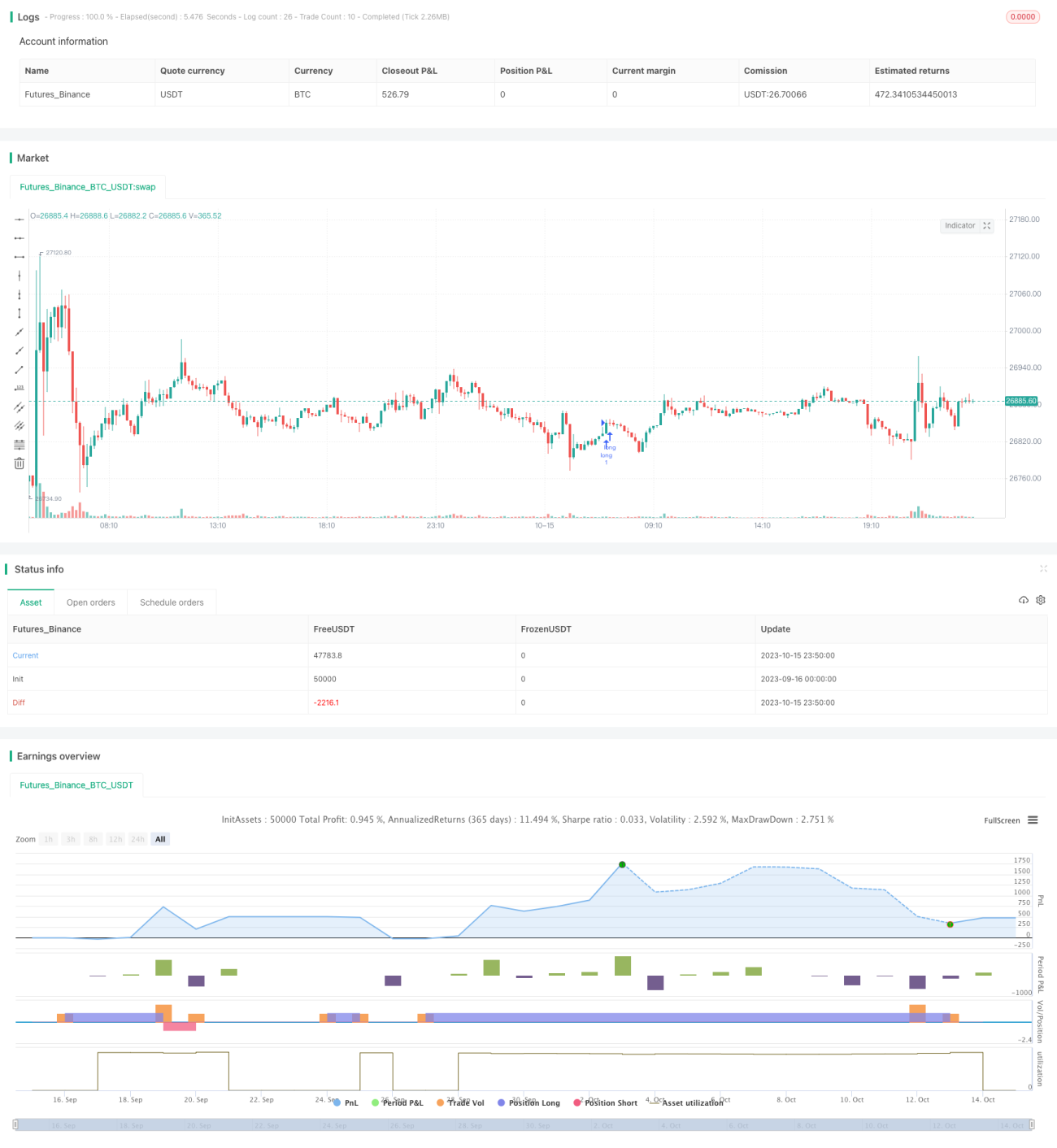

Strategi ini menggunakan pelbagai petunjuk teknikal seperti MACD, RSI, PSAR dan prinsip pengurusan modal dinamik untuk melaksanakan perdagangan mengikut arah aliran dan pembalikan dalam pelbagai jangka masa. Strategi ini boleh digunakan untuk perdagangan jangka pendek, jangka sederhana dan jangka panjang.

Prinsip

Strategi menggunakan petunjuk PSAR untuk menentukan arah aliran. Persilangan EMA pantas dan perlahan dengan garis tengah BB bertindak sebagai titik pengesahan pertama. Arah histogram MACD bertindak sebagai titik pengesahan kedua. Kawasan terlebih beli/terlebih jual RSI bertindak sebagai titik pengesahan ketiga. Apabila semua syarat di atas dipenuhi, isyarat dagangan dihasilkan.

Selepas memasuki pasaran, tetapkan titik henti rugi dan ambil untung. Titik henti rugi ditetapkan berdasarkan gandaan tertentu nilai ATR. Titik ambil untung juga ditetapkan dengan cara yang sama. Pada masa yang sama, tetapkan peratusan kerugian terapung sebagai henti rugi. Apabila kerugian mencapai peratusan tertentu daripada jumlah ekuiti akaun, posisi akan ditutup.

Keuntungan terapung juga mempunyai tetapan peratusan. Apabila keuntungan mencapai peratusan tertentu daripada jumlah ekuiti akaun, posisi akan ditutup untuk mengambil untung.

Pengurusan modal dinamik mengira saiz posisi berdasarkan jumlah ekuiti akaun, ATR, dan gandaan henti rugi yang ditetapkan. Pada masa yang sama, tetapkan volum dagangan minimum.

Kelebihan

-

Pengesahan pelbagai faktor mengelakkan penembusan palsu dan meningkatkan ketepatan kemasukan.

-

Pengurusan modal dinamik mengawal risiko setiap dagangan dan melindungi akaun dengan berkesan.

-

Titik henti rugi dan ambil untung ditetapkan berdasarkan ATR, boleh disesuaikan dengan turun naik pasaran.

-

Tetapan peratusan kerugian terapung dan keuntungan terapung mengunci keuntungan dan mengelakkan pemberian semula.

Risiko

-

Gabungan pelbagai faktor mungkin terlepas sebahagian peluang dagangan.

-

Tetapan peratusan yang terlalu tinggi boleh menyebabkan kerugian yang lebih besar.

-

Nilai ATR yang tidak sesuai boleh menyebabkan titik henti rugi dan ambil untung terlalu longgar atau terlalu agresif.

-

Tetapan pengurusan modal yang tidak betul boleh menyebabkan saiz posisi terlalu besar untuk satu dagangan.

Arah Pengoptimuman

-

Laraskan pemberat faktor kemasukan untuk mengoptimumkan ketepatan isyarat.

-

Uji tetapan parameter peratusan yang berbeza untuk mencari kombinasi terbaik.

-

Pilih gandaan ATR yang munasabah berdasarkan ciri-ciri instrumen yang berbeza.

-

Laraskan parameter pengurusan modal secara dinamik berdasarkan hasil uji balik.

-

Optimumkan tetapan tempoh masa dan uji sesi dagangan.

Kesimpulan

Strategi ini menggabungkan pelbagai petunjuk teknikal untuk menentukan arah aliran, menambah pengurusan modal dinamik untuk mengawal risiko, dan mencapai keuntungan yang stabil dalam pelbagai jangka masa. Berdasarkan hasil uji balik, pemberat faktor, parameter kawalan risiko dan tetapan pengurusan modal boleh dioptimumkan lagi untuk mendapatkan hasil yang lebih baik.

- 1