Strategi Pembalikan Bawah Rangka Masa Berbilang Masa

Gambaran keseluruhan

Strategi ini menggunakan gabungan beberapa indikator bentuk asas untuk mengenal pasti masa-masa perubahan besar, mengambil strategi berhenti kehilangan trend, dan bertujuan untuk mendapatkan keuntungan melebihi berhenti.

Prinsip

Strategi ini adalah berdasarkan kepada beberapa indikator berikut untuk menilai pembalikan dasar:

-

Noro's BottomSensivity: menentukan sama ada garis K mempunyai bentuk bawah tertentu.

-

Indeks Keinginan Kepastian ((CVI): menilai psikologi kosong berhadapan dengan perubahan.

-

Penunjuk akhir ((UCS): menilai keadaan yang melampaui jatuh dari garis rata-rata.

-

RSI: menilai keadaan oversold.

-

Komposisi bentuk: termasuk pelbagai bentuk asas seperti kerucut, paku.

Strategi ini menggunakan beberapa kombinasi indikator dasar, menghasilkan isyarat beli apabila jumlah bentuk dasar yang ditetapkan oleh parameter strategi dipenuhi. Strategi ini juga memasukkan penilaian indikator RSI untuk penyaringan penipuan palsu, dan hanya akan mencetuskan pembelian apabila oversold.

Pengguna boleh menyesuaikan penggunaan dan parameter setiap indikator penghakiman bawah, mewujudkan fleksibiliti yang tinggi. Pada masa yang sama, strategi untuk memasukkan penapis rata-rata SMA, mengelakkan melakukan lebih banyak di bawah trend.

Kelebihan

-

Menggunakan pelbagai penunjuk untuk meningkatkan kepastian

-

Parameter penunjuk yang boleh disesuaikan untuk pelbagai jenis

-

Penapisan rata SMA untuk mengelakkan penarikan

-

Ia boleh dikonfigurasikan hanya untuk laluan K merah untuk mengurangkan risiko.

-

Alarm pop-up, pemantauan dalam masa nyata

Risiko

-

Penghakiman gabungan mungkin terlepas bahagian bawah

-

Bottomline tidak selalu bertukar

-

Perhatian perlu diberikan kepada jumlah transaksi untuk menyokong perubahan.

Arah pengoptimuman

-

Mengoptimumkan konfigurasi parameter penunjuk, menyesuaikan untuk pelbagai jenis

-

Meningkatkan pengurusan kedudukan dan mengurangkan kos dengan menambah stok

-

Meningkatkan strategi berhenti kerugian dan mengesan trend berhenti kerugian

ringkaskan

Strategi ini memanfaatkan penilaian pelbagai indikator untuk meningkatkan ketepatan pengenalan asas, dan mengawal risiko dengan berkesan dengan mengesan trend untuk menghentikan kerugian dan mengunci keuntungan. Namun, masih perlu memperhatikan apakah jumlah perdagangan dapat menyokong trend pembalikan. Pengguna boleh mengoptimumkan parameter berdasarkan ciri-ciri varieti untuk menyesuaikan diri dengan keadaan pasaran yang berbeza.

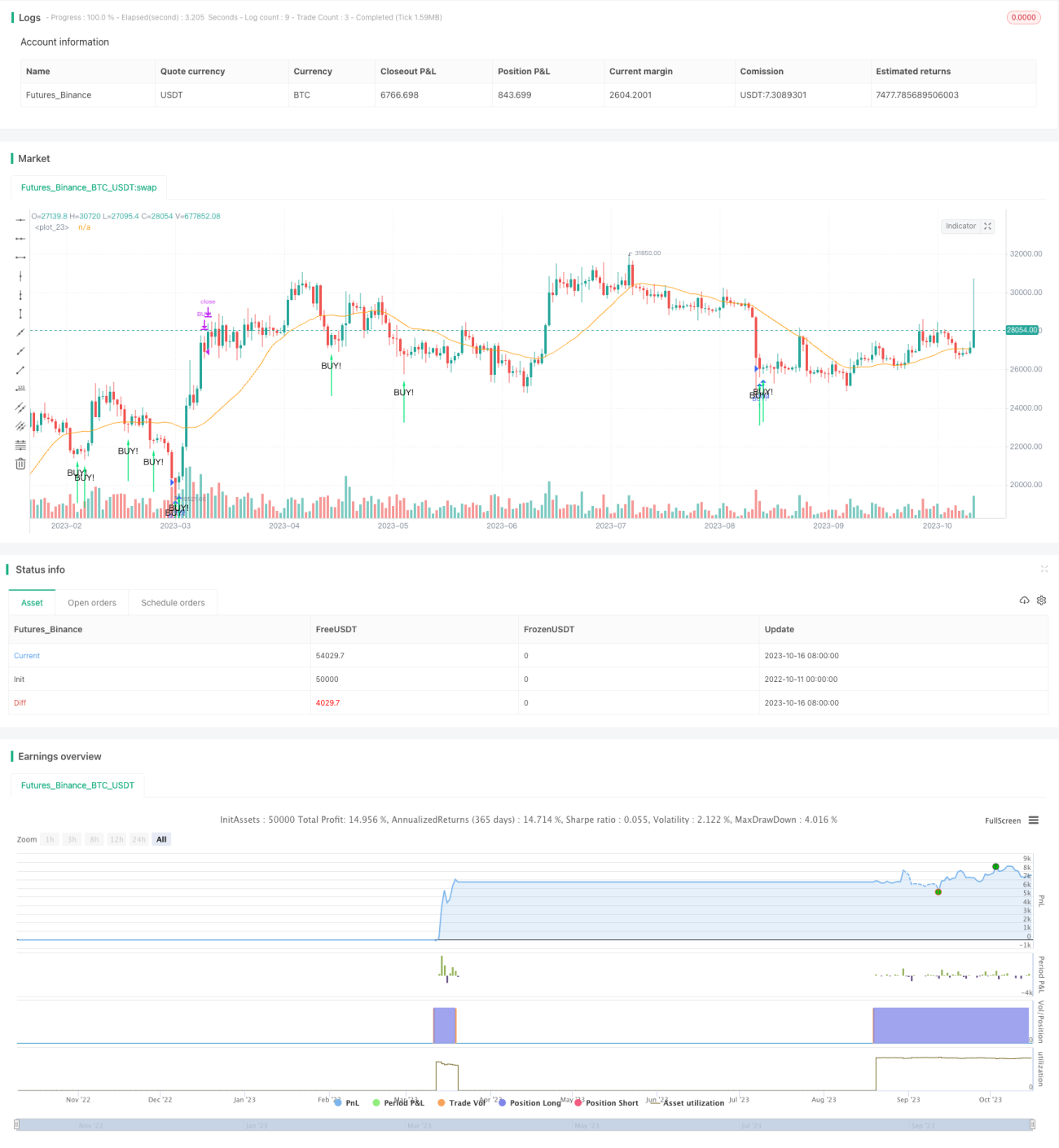

/*backtest

start: 2022-10-11 00:00:00

end: 2023-10-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// the original indicator is Noro's BottomSensivity v0.6

//@version=4

strategy("Noro's BottomSensivity v0.6 strategy + rsi + Alarm", shorttitle="Bottom 0.6 StRsiAlarm", overlay=true)

- 1