Strategi Trailing Stop Loss Penembusan V2

Gambaran Keseluruhan

Strategi ini menggabungkan kelebihan strategi pecahan (breakout) dan strategi henti rugi pengesanan trend (trend trailing stop loss) bagi menangkap isyarat pecahan sokongan dan rintangan dalam carta jangka panjang, sambil menggunakan purata bergerak untuk penjejakan henti rugi, membolehkan keuntungan dijana mengikut arah trend jangka panjang sambil mengawal risiko.

Prinsip Strategi

-

Strategi mula-mula mengira beberapa set purata bergerak dengan parameter berbeza, masing-masing digunakan untuk penentuan arah trend, sokongan/rintangan, dan penjejakan henti rugi.

-

Kemudian, titik tertinggi dan terendah dalam tempoh tertentu dikenal pasti sebagai zon sokongan dan rintangan untuk entry. Apabila harga menembusi zon ini, isyarat dihasilkan.

-

Strategi menggunakan penembusan titik tertinggi sebagai isyarat beli (long), dan penembusan titik terendah sebagai isyarat jual (short).

-

Selepas entry, kedudukan dipegang dengan paras henti rugi ditetapkan pada titik terendah yang ditembusi.

-

Apabila kedudukan mula untung, paras henti rugi ditukar kepada penjejakan purata bergerak. Apabila harga jatuh di bawah purata bergerak, titik henti rugi ditetapkan pada paras terendah lilin (kandil) tersebut.

-

Dengan ini, keuntungan dapat dikunci sambil memberi ruang yang mencukupi untuk kedudukan mengikuti pergerakan trend.

-

Strategi juga menambah purata julat sebenar (Average True Range) untuk memastikan penembusan hanya berlaku dalam julat yang sesuai, mengelakkan penembusan yang terlalu melampau.

Analisis Kelebihan Strategi

-

Menggabungkan dua kelebihan strategi pecahan dan strategi henti rugi pengesanan trend.

-

Mampu membeli penembusan berdasarkan trend jangka panjang, meningkatkan kebarangkalian keuntungan.

-

Strategi henti rugi melindungi kedudukan dan juga memberi ruang yang mencukupi untuk pergerakan.

-

Penapisan turun naik (volatility filter) mengelakkan penembusan yang tidak menguntungkan akibat pergerakan melampau.

-

Perdagangan automatik, sesuai untuk sebahagian masa mengikuti dagangan.

-

Boleh disesuaikan dengan purata bergerak tempoh berbeza untuk operasi.

-

Boleh melaraskan cara penjejakan henti rugi secara fleksibel.

Analisis Risiko Strategi

-

Strategi pecahan mudah terdedah kepada risiko pecahan palsu (false breakout). Boleh melonggarkan pengesahan pecahan.

-

Memerlukan turun naik yang mencukupi untuk menghasilkan isyarat pecahan, mudah tidak berkesan dalam pasaran tidak menentu.

-

Sebahagian pecahan mungkin terlalu singkat untuk ditangkap. Boleh mengurangkan jangka masa untuk mencari lebih banyak peluang.

-

Henti rugi penjejakan mungkin terlalu kerap berhenti rugi dalam pasaran berombak. Boleh melonggarkan jarak henti rugi.

-

Penapisan turun naik mungkin terlepas sebahagian peluang. Boleh mengurangkan parameter penapisan.

Hala Tuju Pengoptimuman Strategi

-

Menguji pelbagai kombinasi parameter purata bergerak untuk mencari parameter terbaik.

-

Menguji mekanisme pengesahan pecahan yang berbeza, seperti saluran, corak lilin, dsb.

-

Mencuba pelbagai cara penjejakan henti rugi untuk mencari henti rugi terbaik.

-

Mengoptimumkan strategi pengurusan modal, seperti skor posisi.

-

Menambah penapisan dengan penunjuk teknikal statistik untuk meningkatkan ketepatan penapisan.

-

Menguji keberkesanan strategi pada instrumen berbeza.

-

Menambah algoritma pembelajaran mesin untuk meningkatkan prestasi strategi.

Ringkasan

Strategi ini menggabungkan idea pecahan dan penjejakan henti rugi trend. Dengan andaian arah jangka panjang yang betul, ia dapat mengoptimumkan ruang keuntungan. Kuncinya ialah mencari kombinasi parameter terbaik dan digabungkan dengan strategi pengurusan modal yang baik untuk menangkap peluang jangka panjang sambil mengawal risiko. Strategi ini berpotensi menjadi strategi trend jangka panjang yang lebih dipercayai melalui pengoptimuman lanjut.

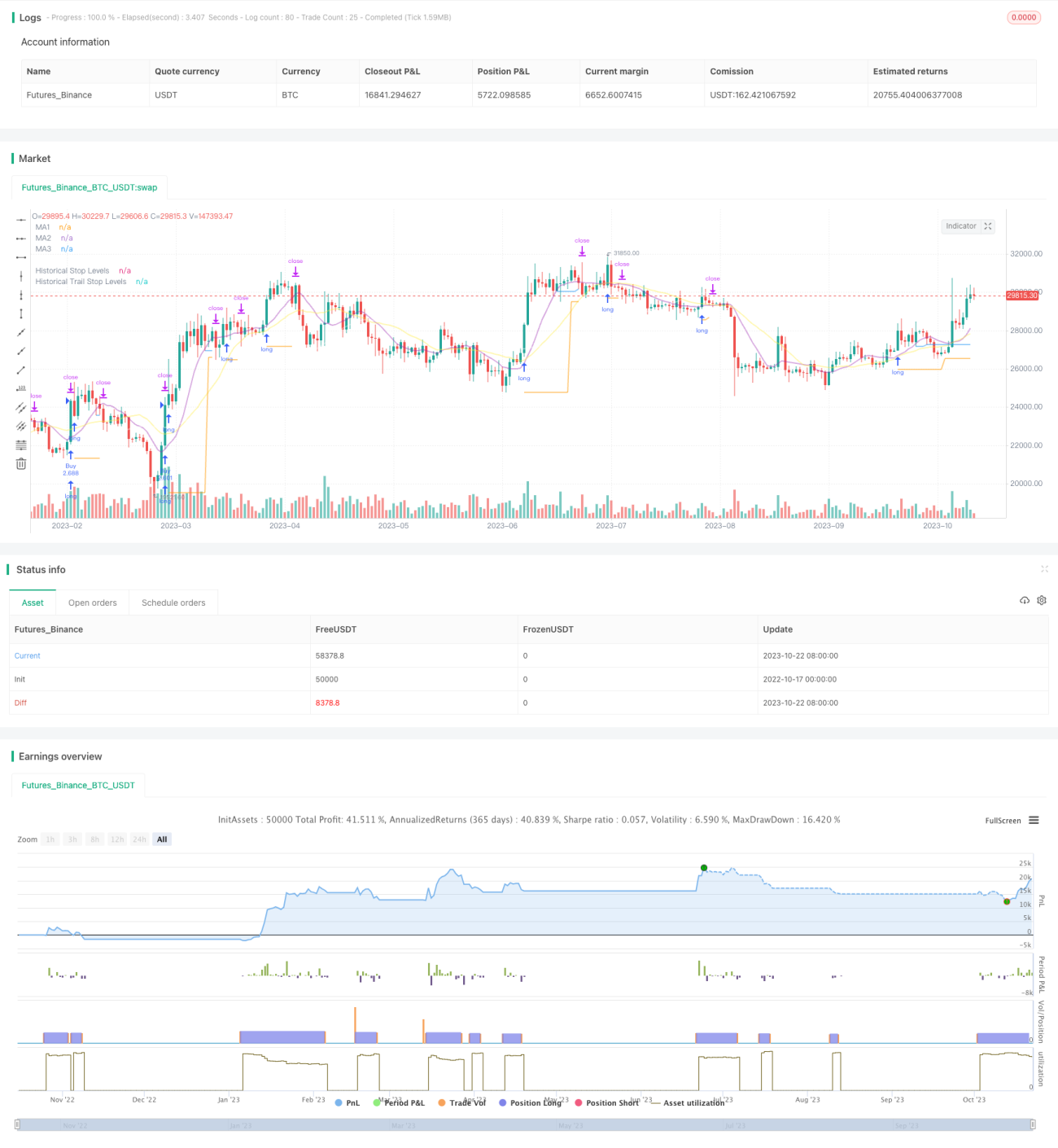

/*backtest

start: 2022-10-17 00:00:00

end: 2023-10-23 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © millerrh

// The intent of this strategy is to buy breakouts with a tight stop on smaller timeframes in the direction of the longer term trend.- 1