Strategi Dagangan Persilangan Purata Bergerak (MA) Jenis Mengikut Trend

Gambaran Keseluruhan

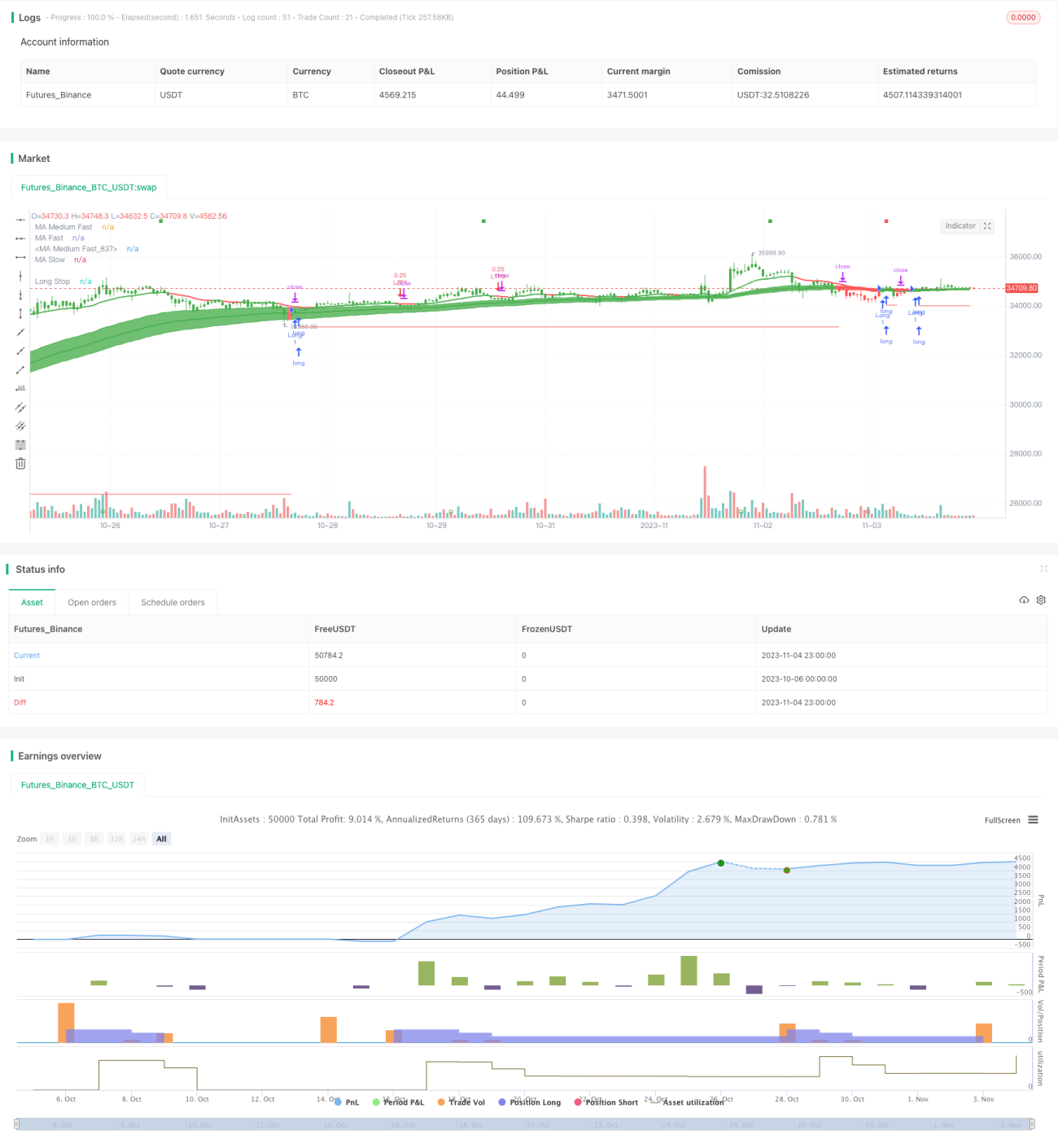

Strategi ini adalah strategi perdagangan pengikut arah aliran berdasarkan purata bergerak. Ia menggunakan tiga Purata Bergerak Hull dengan tetapan parameter yang berbeza untuk menentukan arah aliran harga, dan menggabungkan penapis ATR pantas untuk mengenal pasti potensi pembalikan arah aliran lebih awal. Apabila tiga purata bergerak (cepat, sederhana, perlahan) berlaku persilangan ke atas atau ke bawah, isyarat beli atau jual akan dijana. Strategi ini juga dilengkapi dengan fungsi stop loss bergerak dan take profit bergerak untuk menguruskan risiko dengan berkesan.

Prinsip Strategi

Strategi ini menggunakan tiga Purata Bergerak Hull untuk menentukan arah aliran harga, termasuk satu Hull MA yang lebih pantas, satu Hull MA sederhana, dan satu Hull MA yang lebih perlahan. Arah aliran ditentukan berdasarkan persilangan antara ketiga-tiganya:

- Apabila garis pantas melintasi ke atas garis sederhana, ia menunjukkan harga memasuki arah aliran menaik, dan isyarat beli dikeluarkan.

- Apabila garis pantas melintasi ke bawah garis sederhana, ia menunjukkan harga memasuki arah aliran menurun, dan isyarat jual dikeluarkan.

Untuk meningkatkan sensitiviti dalam mengenal pasti pembalikan arah aliran, strategi ini memperkenalkan penapis ATR pantas berdasarkan RSI. Penapis ini dapat mengukur kebolehubahan harga; apabila arah aliran harga berubah, nilainya akan berubah dengan ketara. Oleh itu, kita boleh meramalkan pembalikan arah aliran harga lebih awal berdasarkan penembusan ke atas atau ke bawah penapis ATR.

Secara khusus, fungsi filtr melaksanakan logik pengiraan penapis ATR pantas ini. Ia mengira saiz ATR berdasarkan nilai RSI. Apabila nilai ATR melintasi ke atas atau ke bawah lengkung RSI, ia mungkin menandakan perubahan arah aliran harga.

Selain itu, strategi ini menetapkan syarat stop loss bergerak dan take profit bergerak, yang membolehkan pengurusan risiko automatik berdasarkan peratusan stop loss dan take profit yang ditetapkan.

Analisis Kelebihan

- Menggunakan tiga garis Hull MA untuk menentukan arah aliran dapat menapis gangguan pasaran dengan berkesan dan mengenal pasti arah aliran jangka sederhana dan panjang.

- Penggunaan penapis ATR pantas meningkatkan keupayaan untuk meramalkan pembalikan arah aliran lebih awal.

- Secara automatik merebut peluang pembalikan arah aliran, melaraskan kedudukan tepat pada masanya, tidak terlepas beli atau jual.

- Stop loss dan take profit bergerak mewujudkan keseimbangan dinamik antara risiko dan ganjaran.

- Parameter boleh disesuaikan, sesuai untuk pasaran dan instrumen perdagangan yang berbeza.

Analisis Risiko

- Strategi persilangan MA mudah menghasilkan isyarat palsu kenaikan dan penurunan, memerlukan penapis ATR sebagai pengesahan tambahan.

- Dalam pasaran yang sangat berayun, MA kerap mengalami persilangan, perlu memantau dengan teliti arah aliran lengkung ATR.

- Titik stop loss yang terlalu kecil mudah menyebabkan stop loss tercetus, manakala terlalu besar sukar untuk mengawal kerugian. Parameter perlu disesuaikan mengikut situasi tertentu.

- Strategi ini lebih sesuai untuk pasaran yang cenderung mengikut arah aliran, tidak sesuai untuk pasaran yang berayun.

- Melalui pengoptimuman parameter, kombinasi terbaik kitaran MA dan ATR boleh dipilih untuk mengurangkan kadar isyarat palsu.

Hala Tuju Pengoptimuman

- Boleh mencuba menukar jenis MA kepada DEMA, TEMA dan varian EMA yang lain untuk melihat sama ada ia dapat menapis lebih banyak gangguan.

- Penapis ATR boleh digantikan dengan garis MIDDLE Keltner Channel untuk menguji peningkatan dalam pengesanan pembalikan arah aliran.

- Boleh menguji kombinasi parameter MA yang berbeza untuk mencari pasangan parameter terbaik.

- Boleh menguji parameter kitaran ATR untuk mencari kesan pelicinan yang terbaik.

- Boleh menambah indikator volum untuk membantu menilai kemungkinan penembusan benar atau palsu.

- Boleh menguji sama ada menambah indikator lain seperti MACD dapat meningkatkan kebolehpercayaan isyarat.

Kesimpulan

Strategi ini menggabungkan pelbagai fungsi: penentuan arah aliran dengan purata bergerak, pengesanan awal pembalikan dengan penapis ATR, dan pengurusan risiko automatik melalui stop loss dan take profit bergerak. Ia dapat mengikuti arah aliran secara automatik, merebut peluang pembalikan tepat pada masanya, dan melalui pengoptimuman parameter boleh disesuaikan dengan pelbagai instrumen dan jangka masa. Ini adalah strategi perdagangan pengikut arah aliran yang sangat praktikal. Kelebihannya adalah logik strategi yang ringkas dan jelas serta kaedah kawalan risiko yang cekap. Namun, perlu juga memberi perhatian kepada isyarat palsu dan penetapan titik stop loss. Dengan pengoptimuman lanjut, hasil strategi yang lebih baik boleh diharapkan.

- 1