Strategi Pasangan Dwi Landasan Momentum dan Pembalikan

Gambaran Keseluruhan

Strategi ini menggabungkan pelbagai penunjuk teknikal untuk melaksanakan momentum songsang dan padanan dwi-landasan, menghasilkan isyarat dagangan. Strategi ini menggunakan corak 123 untuk menentukan titik pusing balik, dan berpasangan dengan penunjuk ergodic CSI untuk membentuk isyarat padanan, membolehkan pengesanan arah aliran. Strategi ini bertujuan untuk menangkap arah aliran jangka sederhana pendek dan memperoleh keuntungan yang lebih tinggi.

Prinsip Strategi

Strategi ini mengandungi dua bahagian:

- Corak 123 untuk menentukan titik pusing balik

- Penunjuk ergodic CSI untuk menjana isyarat padanan

Corak 123 menentukan pusing balik harga berdasarkan hubungan harga penutup tiga batang lilin terkini. Logik penentuan khusus adalah:

Jika harga penutup batang lilin kedua lebih tinggi daripada yang pertama, dan penunjuk stokastik cepat dan perlahan semasa kedua-duanya di bawah 50, maka ia adalah isyarat beli.

Jika harga penutup batang lilin kedua lebih rendah daripada yang pertama, dan penunjuk stokastik cepat dan perlahan semasa kedua-duanya di atas 50, maka ia adalah isyarat jual.

Penunjuk ergodic CSI mempertimbangkan pelbagai faktor seperti harga, julat sebenar, penunjuk arah aliran, dan lain-lain untuk menilai pergerakan pasaran secara menyeluruh dan menjana zon beli dan jual.

Apabila penunjuk berada di atas zon beli, ia menghasilkan isyarat beli; apabila di bawah zon jual, ia menghasilkan isyarat jual.

Akhirnya, isyarat pusing balik dari corak 123 dan isyarat landasan dari ergodic CSI digabungkan dengan operasi "DAN" untuk mendapatkan isyarat strategi akhir.

Kelebihan Strategi

- Menangkap arah aliran jangka sederhana pendek, potensi keuntungan yang lebih besar

- Penentuan corak pusing balik dapat menangkap titik perubahan dengan berkesan

- Padanan dwi-landasan dapat mengurangkan isyarat palsu

Risiko Strategi

- Saham individu mungkin menunjukkan perbezaan, menyebabkan kerugian henti

- Corak pusing balik mudah terjejas oleh pasaran yang tidak menentu

- Ruang pengoptimuman parameter terhad, kesan turun naik yang ketara

Arah Pengoptimuman

- Mengoptimumkan parameter untuk meningkatkan keberkesanan keuntungan strategi

- Menambah logik henti rugi untuk mengurangkan kerugian setiap dagangan

- Menggabungkan model pelbagai faktor untuk meningkatkan kualiti pemilihan saham

Kesimpulan

Strategi ini berjaya menjejaki arah aliran jangka sederhana pendek dengan berkesan melalui corak pusing balik dan padanan dwi-landasan. Berbanding dengan penunjuk teknikal tunggal, strategi ini mempunyai kestabilan dan tahap keuntungan yang lebih tinggi. Langkah seterusnya adalah untuk terus mengoptimumkan parameter, serta menambah modul henti rugi dan pemilihan saham bagi mengurangkan penguncupan dan meningkatkan prestasi keseluruhan.

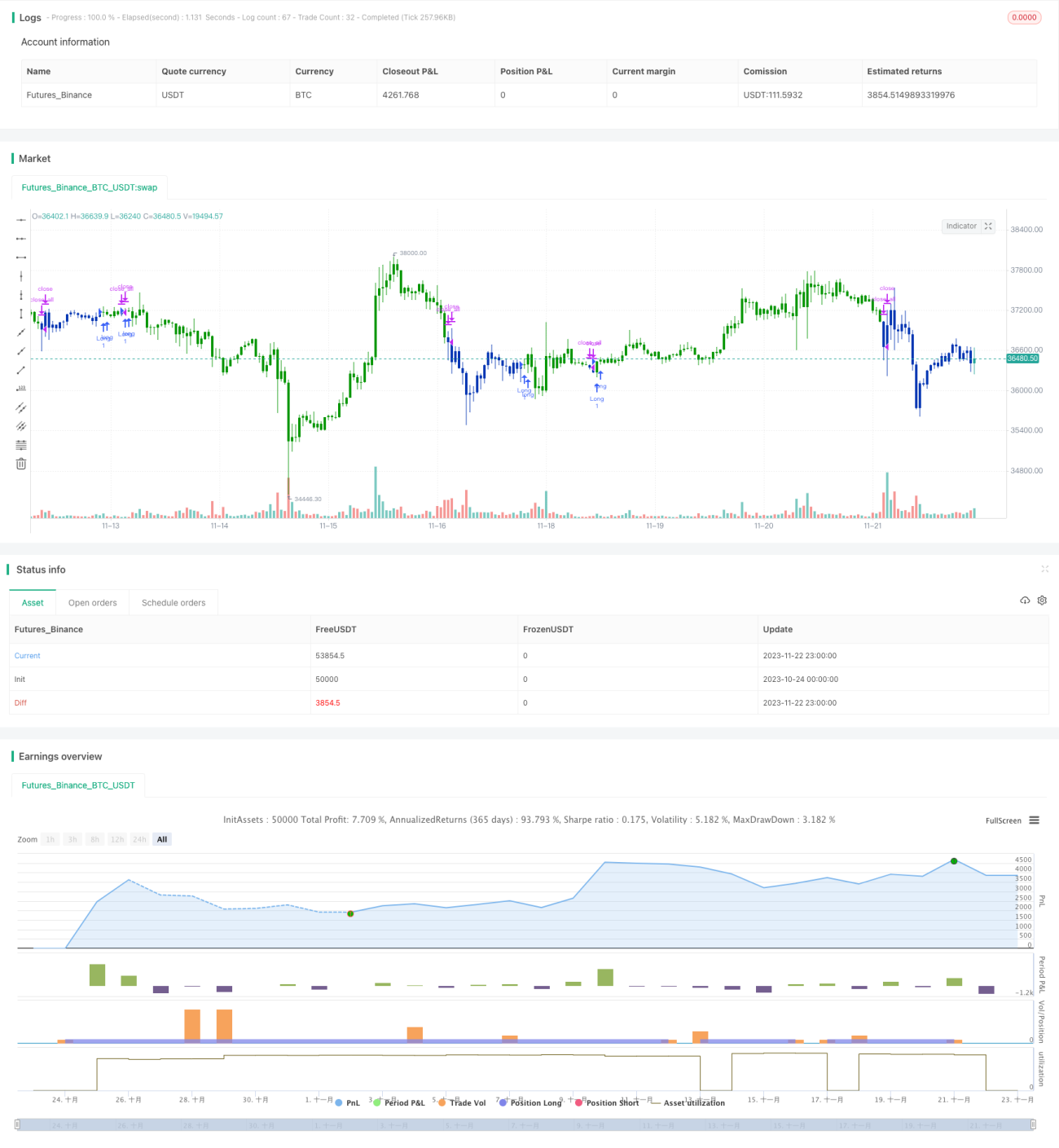

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 22/07/2020

// This is combo strategies for get a cumulative signal. - 1