Strategi Dagangan Kuantitatif Tiga Purata Bergerak

Gambaran Keseluruhan: Strategi ini merupakan strategi analisis teknikal biasa yang menggunakan beberapa penunjuk purata bergerak biasa seperti EMA serta penunjuk tambahan seperti RSI, MACD, PSR untuk membentuk peraturan masuk dan henti rugi, mencari peluang beli rendah jual tinggi.

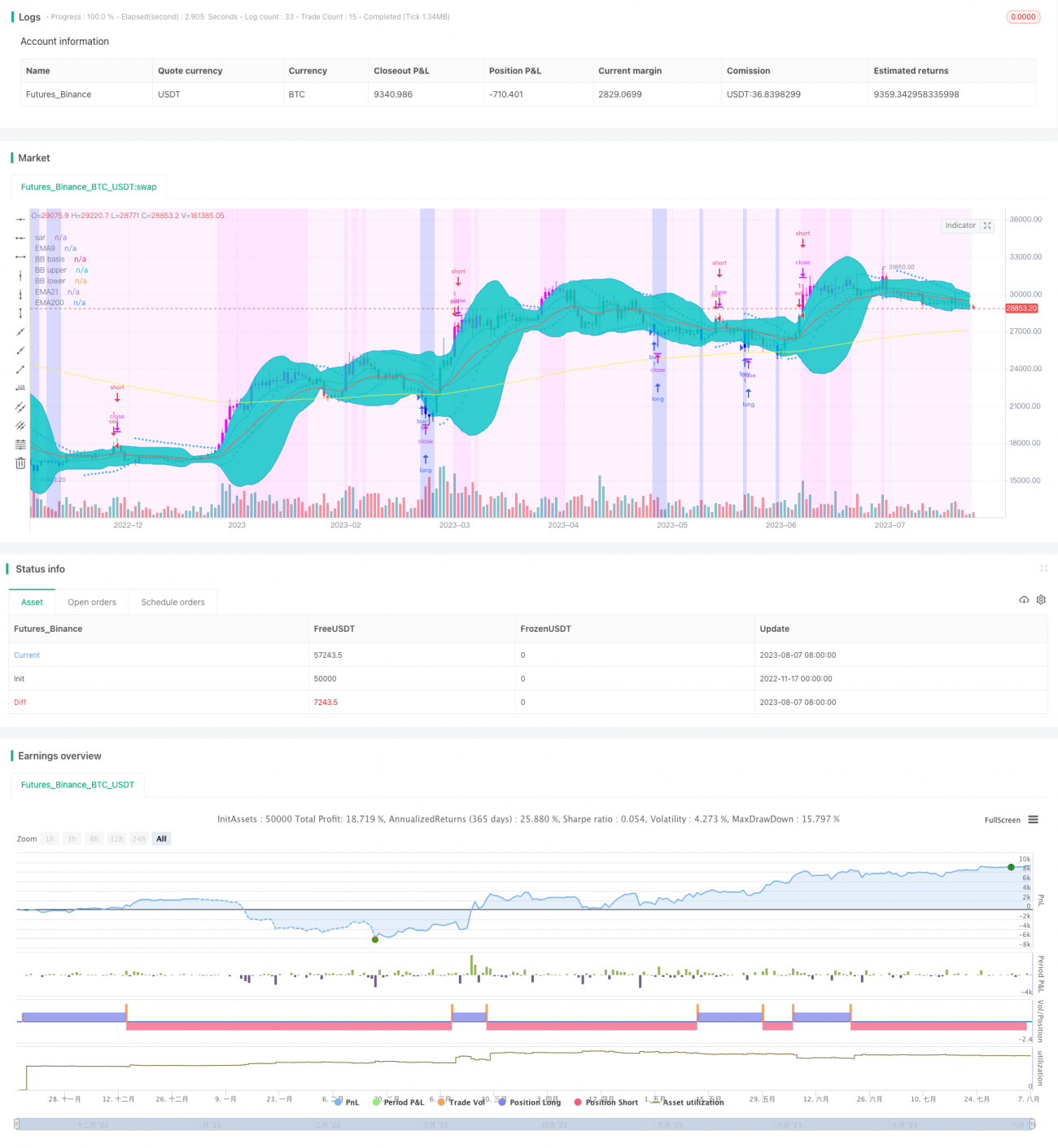

Prinsip Strategi: Teras strategi ini ialah purata bergerak 5, 9, 21 hari. Apabila purata bergerak jangka pendek melintasi ke atas purata bergerak jangka panjang, ia menandakan arah menaik; apabila purata bergerak jangka pendek melintasi ke bawah purata bergerak jangka panjang, ia menandakan arah menurun. Selain itu, RSI digunakan untuk menentukan keadaan terlebih beli/terlebih jual, MACD untuk menilai arah aliran, PSR untuk mengenal pasti sokongan dan rintangan bagi dagangan gabungan. Warna latar belakang menunjukkan sentimen pasaran untuk membantu penilaian arah aliran. Parameter boleh disesuaikan untuk mengkonfigurasi peraturan masuk.

Analisis Kelebihan Strategi:

- Penunjuk MA jelas dan intuitif, mudah untuk menentukan arah aliran.

- RSI berkesan mengenal pasti keadaan terlebih beli/terlebih jual, MACD menilai arah aliran pendek-panjang, PSR mencari tahap harga utama. Penunjuk saling melengkapi.

- Pelbagai peraturan masuk dan tetapan parameter memberikan fleksibiliti tinggi.

- Banyak penunjuk dan kombinasi parameter yang boleh dioptimumkan, boleh disesuaikan dengan keadaan pasaran yang berubah-ubah.

Analisis Risiko:

- Operasi kitaran pendek sukar menangkap arah aliran besar, berisiko terlepas pembalikan.

- Tetapan parameter yang tidak betul boleh menyebabkan terlalu banyak isyarat palsu atau terlepas isyarat sebenar.

- Penunjuk teknikal semata-mata mudah dieksploitasi oleh institusi arbitraj yang menyebabkan kerugian.

- Mudah terkena henti rugi dalam pasaran yang sangat tidak menentu.

Cara Mengatasi:

- Tangkap arah aliran jangka sederhana-panjang dengan sesuai, elakkan operasi kontra arah dalam jangka pendek.

- Optimumkan kombinasi parameter, gunakan henti rugi untuk mengawal risiko.

- Perhatikan kemungkinan pengunduran dari paras tinggi dan lantunan dari paras rendah.

Arah Pengoptimuman:

- Laraskan parameter MA, uji kombinasi terbaik.

- Tambah penunjuk tambahan lain untuk menapis isyarat.

- Tambah metrik pembelajaran mesin untuk menganggar kebarangkalian.

- Gabungkan perubahan volum untuk meningkatkan ketepatan isyarat.

- Tambah strategi henti rugi untuk mengelakkan kerugian daripada membesar.

Kesimpulan: Strategi ini mengintegrasikan pelbagai isyarat penunjuk tambahan, memanfaatkan kekuatan penunjuk MA untuk mengenal pasti peluang beli rendah jual tinggi jangka pendek. Dengan pengoptimuman parameter dan kombinasi penunjuk, keberkesanan strategi boleh ditingkatkan secara berterusan, tetapi kekerapan operasi dan risiko perlu dikawal sederhana bagi mengelakkan kerugian tunggal yang besar daripada menghakis keuntungan keseluruhan.

/*backtest

start: 2022-11-17 00:00:00

end: 2023-08-08 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("f.society v7", title="f.society v7", overlay=true)

//@Author: rick#1414

// ------------------------------------------------------ 1