Strategi Tangkapan Pembalikan

Gambaran Keseluruhan

Strategi Penangkapan Pembalikan (Reversal Capture Strategy) ialah strategi dagangan pembalikan yang menggabungkan penunjuk turun naik Bollinger Bands dengan penunjuk momentum RSI. Ia menetapkan saluran Bollinger Bands dan garis terlebih beli/terlebih jual RSI sebagai isyarat, mencari peluang pembalikan apabila arah aliran berubah untuk berdagang.

Prinsip Strategi

Strategi ini menggunakan Bollinger Bands sebagai penunjuk teknikal utama, disokong oleh penunjuk momentum seperti RSI untuk mengesahkan isyarat dagangan. Logiknya adalah seperti berikut:

- Menentukan arah aliran jangka panjang, sama ada menaik atau menurun. Menggunakan persilangan EMA 50 hari dan EMA 21 hari (golden cross/death cross) untuk menentukan.

- Dalam aliran menurun, apabila harga menembusi garisan bawah Bollinger Bands ke atas, dan pada masa yang sama RSI baru melantun dari kawasan terlebih jual serta membentuk golden cross, ini menunjukkan bahawa kawasan terlebih jual telah membentuk dasar, dan dianggap sebagai isyarat beli.

- Dalam aliran menaik, apabila harga menembusi garisan atas Bollinger Bands ke bawah, dan pada masa yang sama RSI baru jatuh dari kawasan terlebih beli serta membentuk death cross, ini menunjukkan bahawa kawasan terlebih beli telah mula membuat pembetulan, dan dianggap sebagai isyarat jual.

- Isyarat beli dan jual di atas mesti dipenuhi serentak untuk mengelakkan isyarat palsu.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

- Menggabungkan penunjuk turun naik dan penunjuk momentum, isyarat lebih boleh dipercayai.

- Risiko dagangan pembalikan lebih rendah, sesuai untuk dagangan jangka pendek.

- Peraturan yang jelas, mudah untuk melaksanakan dagangan automatik.

- Menggabungkan dagangan arah aliran, mengelakkan pembukaan kedudukan yang tidak teratur dalam pasaran yang tidak menentu.

Analisis Risiko

Strategi ini juga mempunyai risiko berikut:

- Risiko isyarat palsu penembusan saluran Bollinger Bands, memerlukan penapisan oleh RSI.

- Risiko kegagalan pembalikan, memerlukan henti rugi tepat pada masanya.

- Risiko ketepatan masa pembalikan yang tidak tepat, mungkin masuk awal atau terlepas titik terbaik.

Untuk mengatasi risiko di atas, kedudukan henti rugi boleh ditetapkan untuk mengawal pendedahan risiko, dan pada masa yang sama mengoptimumkan parameter, menyesuaikan kitaran Bollinger Bands atau parameter RSI.

Arah Pengoptimuman

Strategi ini terutamanya boleh dioptimumkan dari arah berikut:

- Mengoptimumkan parameter Bollinger Bands, menyesuaikan tempoh kitaran dan saiz sisihan piawai untuk mencari kombinasi parameter terbaik.

- Mengoptimumkan tempoh purata bergerak untuk menentukan tempoh terbaik bagi pengesanan arah aliran.

- Melaraskan parameter RSI untuk mencari julat kawasan terlebih beli/terlebih jual yang terbaik.

- Menambah penunjuk lain seperti KDJ, MACD, dan lain-lain untuk memperkayakan sebab kemasukan sistem.

- Menambah algoritma pembelajaran mesin, menggunakan teknologi AI untuk mencari parameter terbaik secara automatik.

Kesimpulan

Secara keseluruhannya, Strategi Penangkapan Pembalikan adalah strategi dagangan jangka pendek yang berkesan. Ia menggabungkan penentuan arah aliran dan isyarat pembalikan, bukan sahaja dapat menapis isyarat palsu dalam pasaran yang tidak menentu, tetapi juga mengelakkan pertentangan dengan arah aliran dalam pasaran berarah, dengan risiko terkawal. Melalui pengoptimuman parameter dan model secara berterusan, prestasi strategi yang lebih baik boleh dicapai.

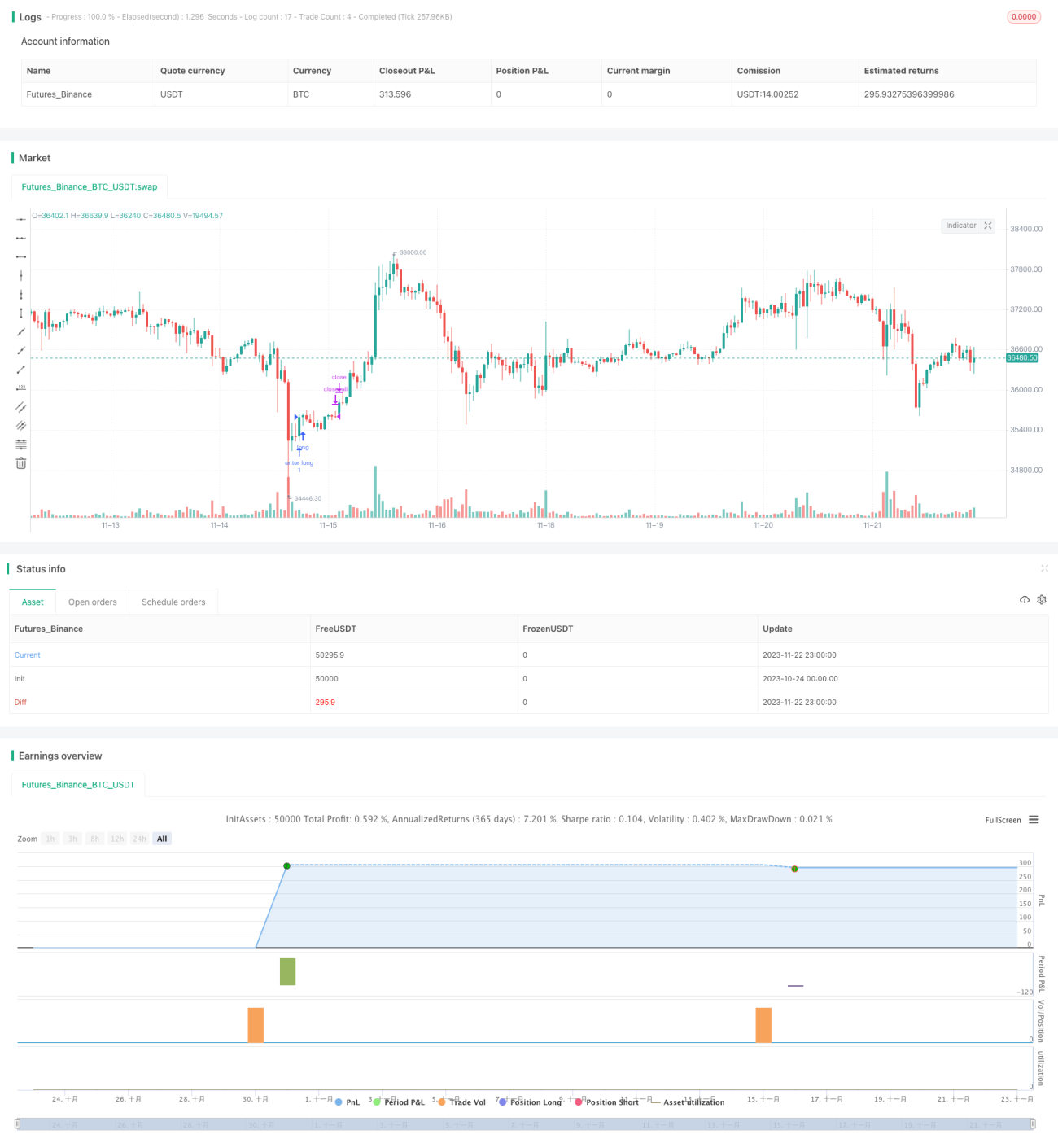

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This is an Open source work. Please do acknowledge in case you want to reuse whole or part of this code.

// Please see the documentation to know the details about this.

//@version=5- 1