Strategi momentum mudah berdasarkan SMA, EMA dan volum

Gambaran Keseluruhan

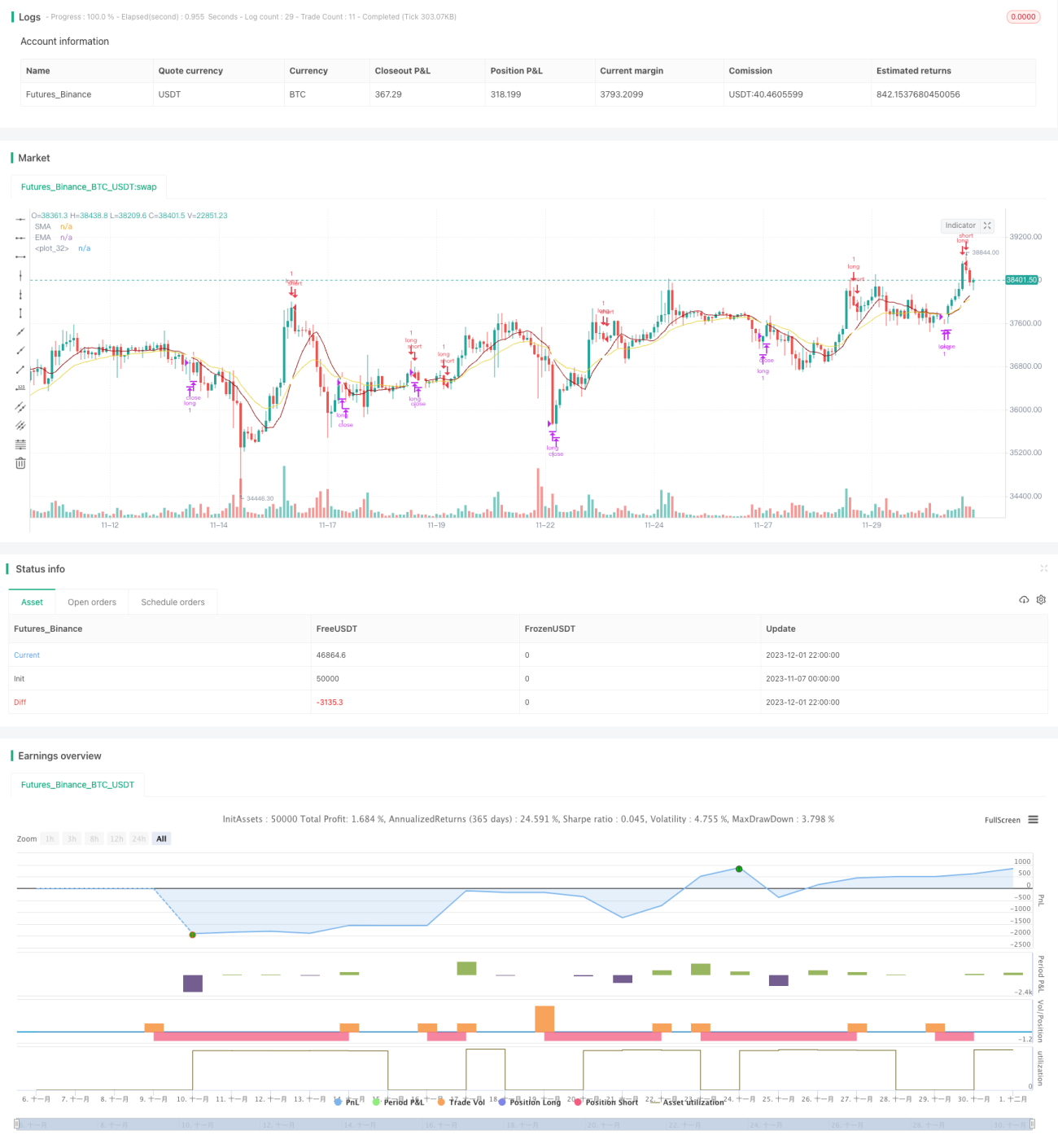

Strategi ini ialah strategi momentum intraday mudah yang hanya mengambil posisi panjang (tidak pernah posisi pendek). Ia menggunakan indikator SMA, EMA dan volum untuk cuba memasuki pasaran pada masa yang optimum (iaitu apabila harga dan momentum sama-sama meningkat). Kelebihannya ialah pelaksanaannya yang mudah dan keupayaan untuk mengenal pasti arah aliran.

Prinsip Strategi

Logik penjanaan isyarat Entry strategi ini adalah: apabila indikator SMA lebih tinggi daripada indikator EMA dan sama ada 3 batang lilin berturut-turut atau 4 batang lilin berturut-turut membentuk arah aliran menaik, dan harga terendah batang lilin di tengah lebih tinggi daripada harga pembukaan batang lilin yang memulakan kenaikan, isyarat Entry akan dihasilkan.

Logik penjanaan isyarat Exit adalah: apabila indikator SMA menembusi ke bawah indikator EMA, isyarat Exit akan dihasilkan.

Strategi ini hanya mengambil posisi panjang, tidak pernah posisi pendek. Logik Entry dan Exitnya mempunyai keupayaan tertentu untuk mengenal pasti arah aliran menaik yang berterusan.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

- Logik strategi adalah mudah, senang difahami dan dilaksanakan;

- Menggunakan indikator teknikal biasa seperti SMA, EMA dan volum, dengan parameter yang fleksibel untuk dilaraskan;

- Mempunyai keupayaan untuk mengenal pasti arah aliran menaik yang berterusan, dan dapat merebut sebahagian peluang dalam arah aliran tersebut.

Analisis Risiko

Strategi ini juga mempunyai risiko berikut:

- Tidak dapat mengenal pasti pasaran yang menurun atau menyisi, mungkin menyebabkan pengunduran yang besar;

- Tidak dapat memanfaatkan peluang posisi pendek, tidak boleh melindung nilai terhadap arah aliran menurun, mungkin terlepas peluang keuntungan yang baik;

- Indikator volum tidak berkesan untuk data frekuensi tinggi, memerlukan pelarasan parameter;

- Boleh menggunakan stop loss untuk mengawal risiko.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari beberapa aspek berikut:

- Menambah peluang dagangan posisi pendek, melaksanakan dagangan dua hala (panjang dan pendek), untuk meraih keuntungan daripada arah aliran menurun;

- Menggunakan indikator yang lebih maju seperti MACD, RSI, dsb. dalam strategi gabungan untuk meningkatkan keupayaan menilai arah aliran;

- Mengoptimumkan logik stop loss untuk mengurangkan risiko pengunduran;

- Melaraskan parameter, menguji data dengan tempoh yang berbeza, untuk mencari kombinasi parameter terbaik.

Rumusan

Secara keseluruhannya, strategi ini adalah strategi penjejakan arah aliran yang sangat mudah, yang menentukan masa kemasukan melalui indikator SMA, EMA dan volum. Kelebihannya ialah mudah dan senang dilaksanakan, sesuai untuk pembelajaran peringkat permulaan, tetapi ia tidak dapat mengenal pasti arah aliran menyisi dan menurun, dan mempunyai risiko tertentu. Ia boleh diperbaiki dengan memperkenalkan posisi pendek, mengoptimumkan indikator dan stop loss, dsb.

- 1