Strategi Super Trend Suria

Gambaran Keseluruhan

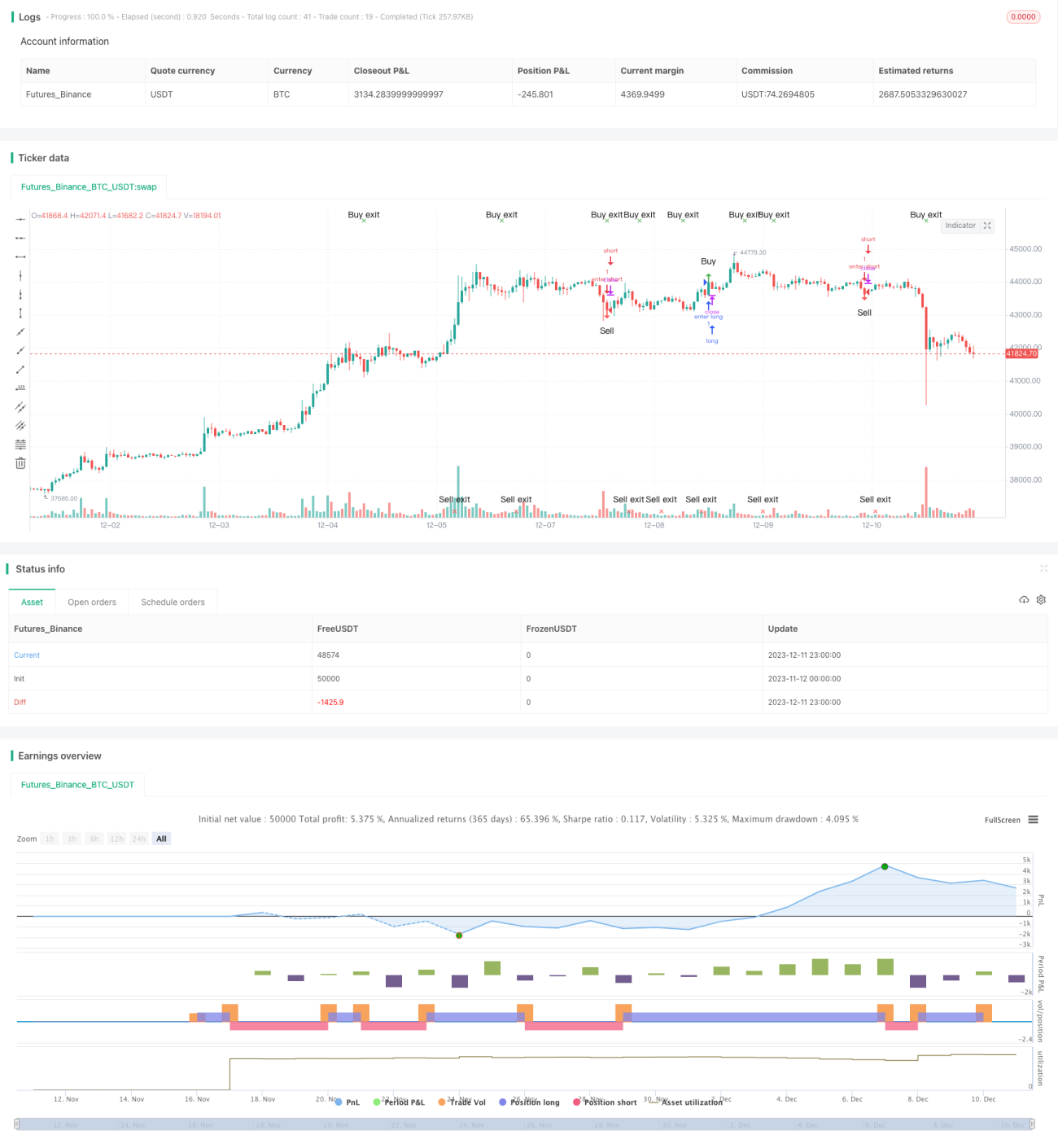

Strategi Super Trend Cahaya Matahari adalah strategi pengesanan trend berdasarkan penunjuk ATR dan SuperTrend. Ia dapat meramalkan pembalikan trend dengan tepat, sangat sesuai digunakan sebagai penunjuk masa. Strategi ini dapat meningkatkan kesabaran dan ketabahan pelabur, membantu mereka memasuki dan keluar dari pasaran pada masa yang tepat.

Prinsip Strategi

Strategi ini menggunakan penunjuk SuperTrend untuk menentukan arah trend semasa. Apabila penunjuk SuperTrend mengalami perubahan arah, kami menganggap mungkin berlaku pembalikan trend. Selain itu, strategi juga menggunakan arah badan lilin (K-line body) untuk pertimbangan tambahan. Apabila isyarat pembalikan berpotensi muncul tetapi arah badan lilin konsisten dengan sebelumnya, isyarat tidak sah akan ditapis.

Secara khusus, strategi menjana isyarat dagangan berdasarkan logik berikut:

- Gunakan penunjuk SuperTrend untuk menentukan arah trend utama

- Apabila arah penunjuk SuperTrend berubah, menghasilkan isyarat pembalikan berpotensi

- Jika pada masa ini arah badan lilin konsisten dengan sebelumnya, tapis isyarat pembalikan tersebut

- Jika arah badan lilin berubah, sahkan isyarat pembalikan, hasilkan isyarat dagangan

Analisis Kelebihan

- Berdasarkan penunjuk SuperTrend, mampu menentukan titik pembalikan trend dengan tepat

- Menggabungkan arah badan lilin untuk menapis isyarat tidak sah, meningkatkan kualiti isyarat

- Sesuai sebagai penunjuk masa untuk membimbing pelabur memilih masa masuk dan keluar yang munasabah

- Boleh digunakan secara meluas dalam mana-mana jangka masa dan pelbagai instrumen, sangat mudah menyesuaikan diri

Risiko dan Penyelesaian

- Penunjuk SuperTrend mudah menghasilkan isyarat berlebihan, perlu penapisan tambahan

Penyelesaian: Strategi ini menggunakan arah badan lilin untuk pertimbangan tambahan, berkesan menapis isyarat tidak sah - Tetapan parameter SuperTrend mudah terlebih optimum atau terlebih optimum

Penyelesaian: Gunakan parameter lalai, elakkan pelarasan berlebihan oleh manusia - Tidak dapat mengendalikan pembalikan dalam pasaran yang sangat pantas

Penyelesaian: Laraskan parameter tempoh ATR dengan sesuai untuk menghadapi pasaran yang lebih pantas

Arah Pengoptimuman

- Cuba gabungan parameter tempoh ATR yang berbeza

- Tambah penunjuk Volume atau volatiliti untuk penapisan isyarat tambahan

- Gabungkan dengan sistem penunjuk lain untuk meningkatkan prestasi strategi

- Bina mekanisme stop loss untuk mengawal kerugian setiap dagangan

Kesimpulan

Strategi Super Trend Cahaya Matahari adalah strategi berkesan yang berdasarkan penunjuk SuperTrend untuk menentukan pembalikan trend. Ia menggabungkan arah badan lilin untuk pertimbangan tambahan, berkesan menapis isyarat tidak sah, meningkatkan kualiti isyarat. Strategi ini mudah dikendalikan, mudah menyesuaikan diri, dan boleh digunakan secara meluas dalam pelbagai instrumen dan jangka masa. Melalui pengoptimuman parameter yang munasabah dan penambahan mekanisme stop loss, prestasi strategi dapat ditingkatkan lagi.

- 1