Strategi Pengesanan Trend Persilangan Dua MA

Gambaran Keseluruhan

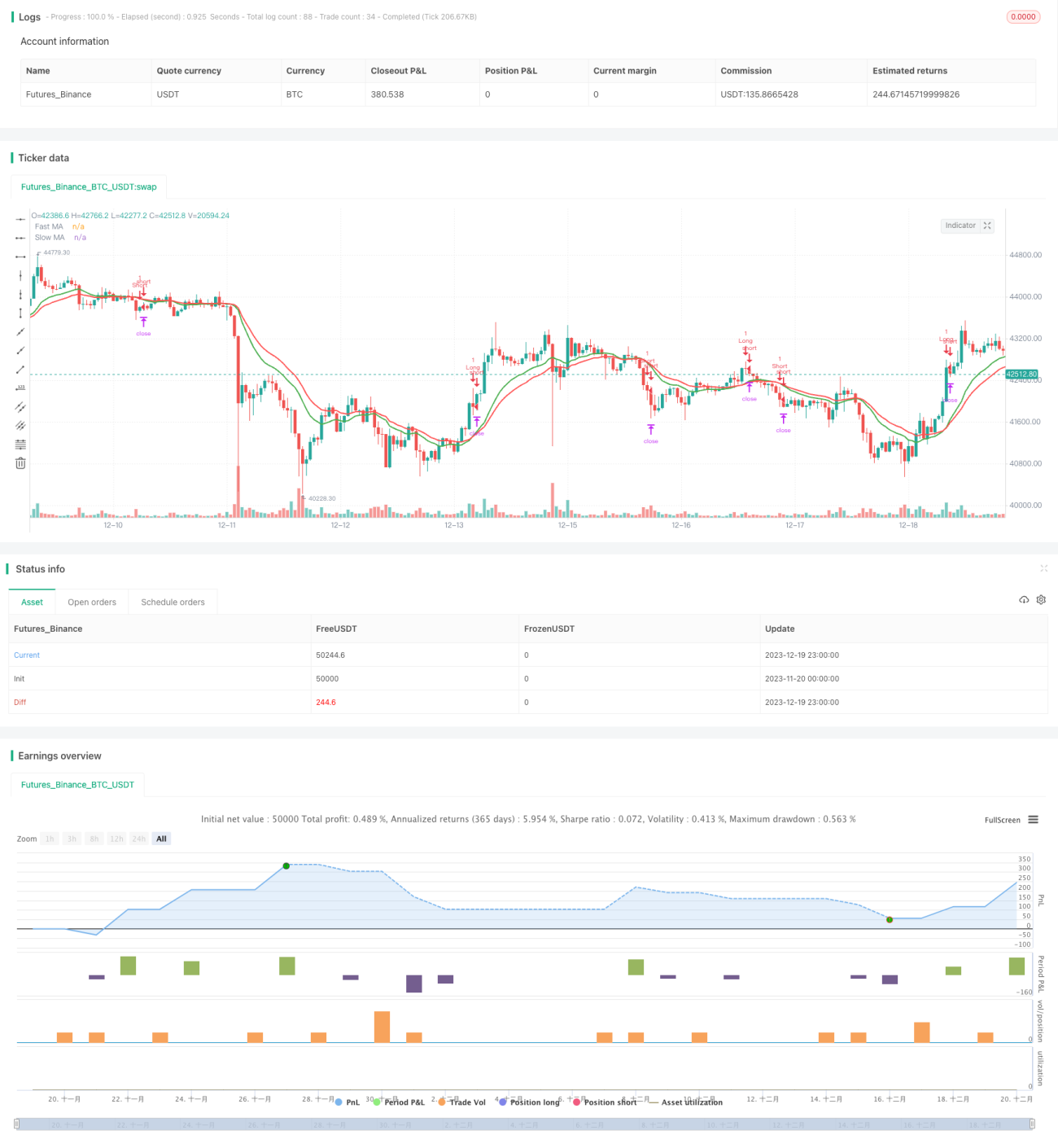

Strategi ini menggunakan kaedah persilangan purata bergerak berganda (double moving average crossover) yang tipikal untuk menjejak arah aliran, digabungkan dengan mekanisme pengurusan risiko seperti stop loss, take profit, dan trailing stop, bertujuan untuk meraih keuntungan besar daripada pergerakan arah aliran pasaran.

Prinsip Strategi

- Kira purata bergerak eksponen (EMA) untuk tempoh pantas n hari sebagai purata bergerak jangka pendek;

- Kira purata bergerak eksponen (EMA) untuk tempoh perlahan m hari sebagai purata bergerak jangka panjang;

- Apabila purata bergerak jangka pendek menembusi purata bergerak jangka panjang dari bawah ke atas, ambil posisi beli (long); apabila menembusi dari atas ke bawah, ambil posisi jual (short);

- Syarat tutup posisi: penembusan songsang (contohnya, jika posisi beli diambil, penembusan songsang akan menutup posisi).

- Gunakan stop loss, take profit, trailing stop dan lain-lain untuk menguruskan risiko.

Analisis Kelebihan

- Menggunakan dua EMA dapat menilai titik perubahan arah aliran harga dengan baik, serta meraih keuntungan daripada arah aliran.

- Digabungkan dengan stop loss, take profit, dan trailing stop, dapat mengawal kerugian setiap dagangan, mengunci keuntungan, dan mengurangkan pengeluaran (drawdown).

- Parameter yang boleh disesuaikan adalah banyak, membolehkan pelarasan dan pengoptimuman mengikut instrumen dan persekitaran pasaran yang berbeza.

- Logik strategi adalah mudah dan jelas, mudah difahami dan diubah suai.

- Menyokong dagangan beli dan jual, dapat menyesuaikan dengan pelbagai jenis pasaran.

Analisis Risiko

- Strategi purata bergerak berganda sangat sensitif terhadap penembusan palsu, mudah terperangkap.

- Penetapan parameter yang tidak sesuai boleh menyebabkan dagangan yang kerap, meningkatkan kos dagangan dan kehilangan slippage.

- Strategi itu sendiri tidak dapat menentukan titik perubahan arah aliran; lebih baik digabungkan dengan penunjuk lain untuk penilaian yang lebih berkesan.

- Dalam pasaran yang tidak menentu (oscillating), ia cenderung menghasilkan isyarat dagangan tetapi keuntungan sebenar adalah rendah.

- Memerlukan pengoptimuman parameter untuk menyesuaikan dengan instrumen dan persekitaran pasaran yang berbeza.

Risiko boleh dikurangkan melalui cara berikut:

- Menggabungkan penunjuk lain untuk menapis penembusan palsu.

- Mengoptimumkan tetapan parameter untuk mengurangkan kekerapan dagangan.

- Menambah penunjuk penentuan arah aliran untuk mengelakkan dagangan dalam pasaran tidak menentu.

- Melaraskan pengurusan saiz posisi untuk mengurangkan risiko setiap dagangan.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari beberapa aspek berikut:

- Mengoptimumkan tempoh kitaran purata bergerak pantas dan perlahan untuk menyesuaikan dengan instrumen dan persekitaran pasaran yang berbeza.

- Menambah penunjuk lain untuk menentukan arah aliran dan menapis isyarat penembusan palsu. Contoh tipikal termasuk MACD, KDJ, dsb.

- Boleh mempertimbangkan untuk menukar EMA kepada SMA atau purata bergerak wajaran (WMA).

- Melaraskan jarak stop loss secara dinamik berdasarkan ATR.

- Berdasarkan kaedah pengurusan saiz posisi, boleh melaraskan saiz posisi setiap dagangan secara fleksibel.

- Berdasarkan gabungan penunjuk korelasi dan volatiliti, melakukan pengoptimuman penyesuaian parameter.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi penjejakan arah aliran menggunakan dua EMA yang tipikal. Ia mempunyai kelebihan meraih keuntungan daripada pergerakan arah aliran, digabungkan dengan mekanisme pengurusan risiko seperti stop loss, take profit, dan trailing stop. Namun, ia juga mempunyai beberapa masalah tipikal, seperti sensitiviti tinggi terhadap bunyi dan pasaran tidak menentu, mudah terperangkap. Dengan memperkenalkan penunjuk tambahan, pengoptimuman parameter, pelarasan dinamik, dan penggunaan gabungan, kesan strategi ini dapat dipertingkatkan lagi. Secara keseluruhan, jika parameter ditetapkan dengan sesuai dan sepadan dengan pergerakan instrumen, strategi ini boleh memberikan hasil yang baik.

- 1