Strategi Perdagangan Persilangan Bawah Bollinger Bands dengan Pullback RSI

Gambaran Keseluruhan

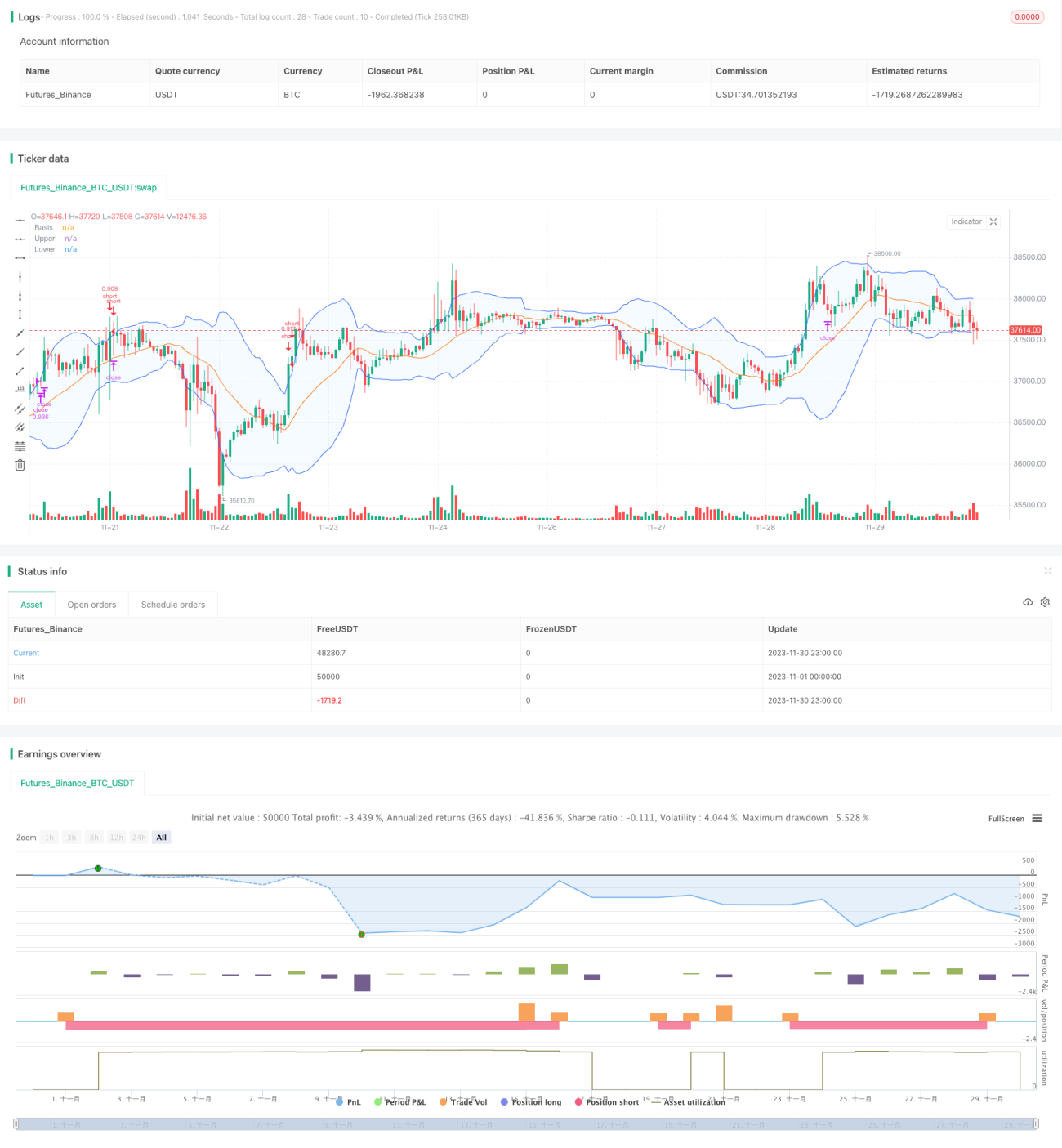

Strategi ini menggunakan indikator Bollinger Bands untuk menilai sama ada harga telah memasuki kawasan terlebih beli atau terlebih jual, digabungkan dengan indikator RSI untuk mengesan peluang pembetulan. Apabila berlaku persilangan mati di kawasan terlebih beli, strategi akan membuka posisi jual (short), dan akan menutup posisi (stop loss) apabila harga naik melebihi jalur atas Bollinger Bands.

Prinsip Strategi

Strategi ini berdasarkan prinsip-prinsip berikut:

- Apabila harga penutup menembusi ke atas jalur atas Bollinger Bands, ini menunjukkan aset telah memasuki kawasan terlebih beli dan terdapat peluang untuk pembetulan.

- Indikator RSI dapat menilai kawasan terlebih beli/terlebih jual dengan berkesan; RSI > 70 menunjukkan kawasan terlebih beli.

- Apabila harga penutup turun semula dari jalur atas, buka posisi jual (short).

- Apabila RSI turun dari kawasan terlebih beli atau titik henti rugi tercapai, tutup posisi untuk henti rugi.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

- Menggunakan Bollinger Bands untuk menilai kawasan terlebih beli/terlebih jual, meningkatkan kadar kejayaan dagangan.

- Menggabungkan indikator RSI untuk menapis peluang pecah palsu, mengelakkan kerugian yang tidak perlu.

- Nisbah untung rugi yang tinggi, mengawal risiko secara maksimum.

Analisis Risiko

Strategi ini mengandungi risiko berikut:

- Harga terus naik selepas menembusi jalur atas, menyebabkan kerugian semakin besar.

- RSI tidak turun tepat pada masanya, menyebabkan kerugian semakin besar.

- Posisi sehala (single-sided) tidak dapat berdagang dalam pasaran yang mendatar (sideways).

Risiko boleh dikurangkan dengan cara berikut:

- Melaraskan titik henti rugi dengan sesuai untuk menutup kerugian tepat pada masanya.

- Menggabungkan indikator lain untuk mengesan isyarat penurunan RSI.

- Menggabungkan indikator purata bergerak untuk menilai sama ada pasaran memasuki fasa mendatar.

Hala Tuju Pengoptimuman

Strategi ini boleh dioptimumkan dari aspek berikut:

- Mengoptimumkan parameter Bollinger Bands untuk menyesuaikan dengan lebih banyak instrumen dagangan.

- Mengoptimumkan parameter RSI untuk meningkatkan keberkesanan indikator.

- Menambah kombinasi indikator lain untuk menilai titik perubahan trend.

- Menambah logik dagangan untuk posisi beli (long).

- Menggabungkan strategi henti rugi untuk melaraskan titik henti rugi secara dinamik.

Kesimpulan

Secara keseluruhan, strategi ini adalah strategi dagangan jangka pendek klasik di kawasan terlebih beli. Ia menggunakan Bollinger Bands untuk menentukan titik masuk/keluar dan RSI untuk menapis isyarat. Risiko dikawal melalui henti rugi yang munasabah. Prestasi boleh ditingkatkan melalui pengoptimuman parameter, kombinasi indikator, dan penambahan logik pembukaan posisi.

- 1