Strategi Bollinger Bands dengan ATR Trailing Stop

Gambaran Keseluruhan

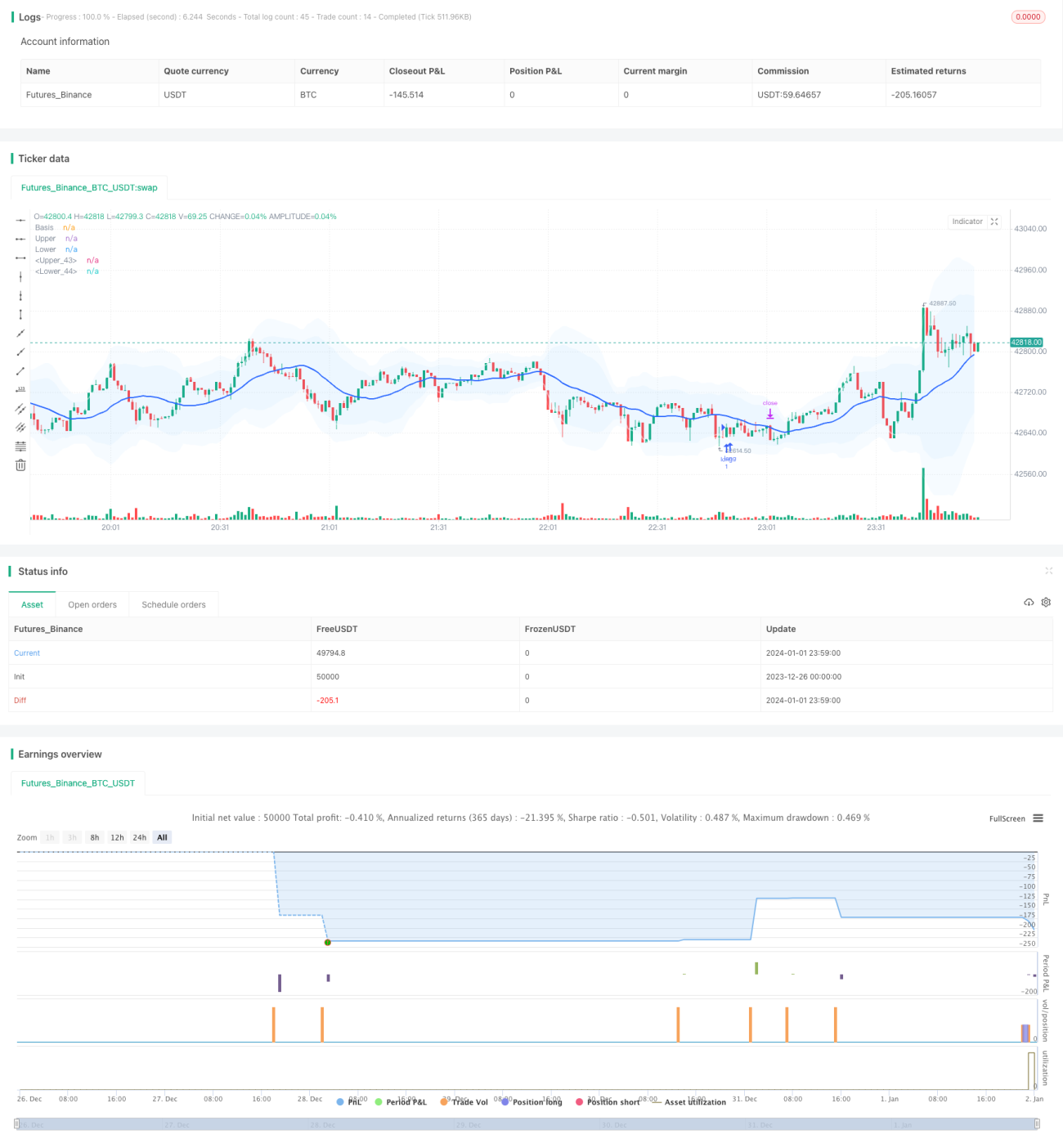

Strategi ini menggabungkan penggunaan Penunjuk Jalur Bollinger dan Penunjuk Purata Julat Sebenar (ATR), membentuk strategi dagangan pecahan dengan fungsi hentian mengekor (trailing stop). Apabila harga menembusi jalur atas atau bawah Jalur Bollinger pada sisihan piawai yang ditentukan, isyarat dagangan dijana. Pada masa yang sama, penunjuk ATR digunakan untuk mengira tahap henti rugi (stop loss) dan ambil untung (take profit), membolehkan kawalan nisbah untung-rugi. Selain itu, strategi ini juga mempunyai fungsi penapisan masa dan pengoptimuman parameter.

Prinsip Strategi

Langkah pertama, kira garisan tengah, garisan atas dan garisan bawah. Garisan tengah ialah Purata Bergerak Mudah (SMA) harga, manakala garisan atas dan bawah adalah gandaan integer sisihan piawai harga. Apabila harga menembusi ke atas dari garisan bawah, ambil posisi beli (long); apabila harga menembusi ke bawah dari garisan atas, ambil posisi jual (short).

Langkah kedua, kira penunjuk ATR. Penunjuk ATR mencerminkan purata amplitud turun naik harga. Tetapkan tahap henti rugi untuk posisi beli dan jual berdasarkan nilai ATR. Pada masa yang sama, tetapkan tahap ambil untung berdasarkan nilai ATR untuk mengawal nisbah untung-rugi.

Langkah ketiga, gunakan penapis masa, hanya berdagang dalam tempoh masa yang ditetapkan, mengelakkan turun naik yang kuat daripada peristiwa berita penting.

Langkah keempat, mekanisme hentian mengekor (trailing stop). Berdasarkan kedudukan ATR terkini, laraskan tahap henti rugi secara masa nyata untuk mengunci lebih banyak keuntungan.

Analisis Kelebihan

- Penunjuk Jalur Bollinger sendiri mencerminkan pusat harga, lebih berkesan daripada purata bergerak tunggal;

- Henti rugi ATR menjadikan nisbah untung-rugi setiap dagangan terkawal, mengurus risiko dengan berkesan;

- Hentian mengekor boleh melaras secara automatik berdasarkan turun naik pasaran, mengunci lebih banyak keuntungan;

- Strategi ini mempunyai parameter yang kaya, membolehkan kombinasi yang boleh disuaikan secara peribadi.

Analisis Risiko

- Apabila pasaran utama berayun dan menyesuaikan diri, kerugian kecil yang kerap mungkin berlaku;

- Pecahan Jalur Bollinger untuk pembalikan mungkin gagal;

- Risiko dagangan pada waktu malam dan semasa berita penting adalah tinggi, perlu dielakkan.

Langkah mengatasi:

- Patuhi prinsip pengurusan risiko dengan ketat, kawal kerugian setiap dagangan;

- Optimumkan parameter untuk meningkatkan kadar kemenangan;

- Gunakan penapis masa untuk mengelakkan tempoh berisiko tinggi.

Arah Pengoptimuman

- Uji kombinasi parameter yang berbeza untuk konfigurasi optimum

- Tambah penunjuk momentum seperti OBV untuk pemasaan

- Tambah modul pembelajaran mesin untuk pengoptimuman

Kesimpulan

Strategi ini menggabungkan penggunaan Penunjuk Jalur Bollinger untuk menilai pusat arah aliran dan arah pecahan, Penunjuk ATR untuk mengira ambil untung dan henti rugi bagi memastikan nisbah untung-rugi, serta hentian mengekor untuk mengunci keuntungan. Kelebihan strategi ini adalah kebolehsuaian yang tinggi, risiko terkawal, sesuai untuk Dagangan Intraday jangka pendek. Pengoptimuman parameter dan pembelajaran mesin boleh meningkatkan lagi kadar kemenangan dan keuntungan strategi.

- 1