Strategi perdagangan kuantitatif yang menggabungkan tren dan ayunan

Gambaran Keseluruhan

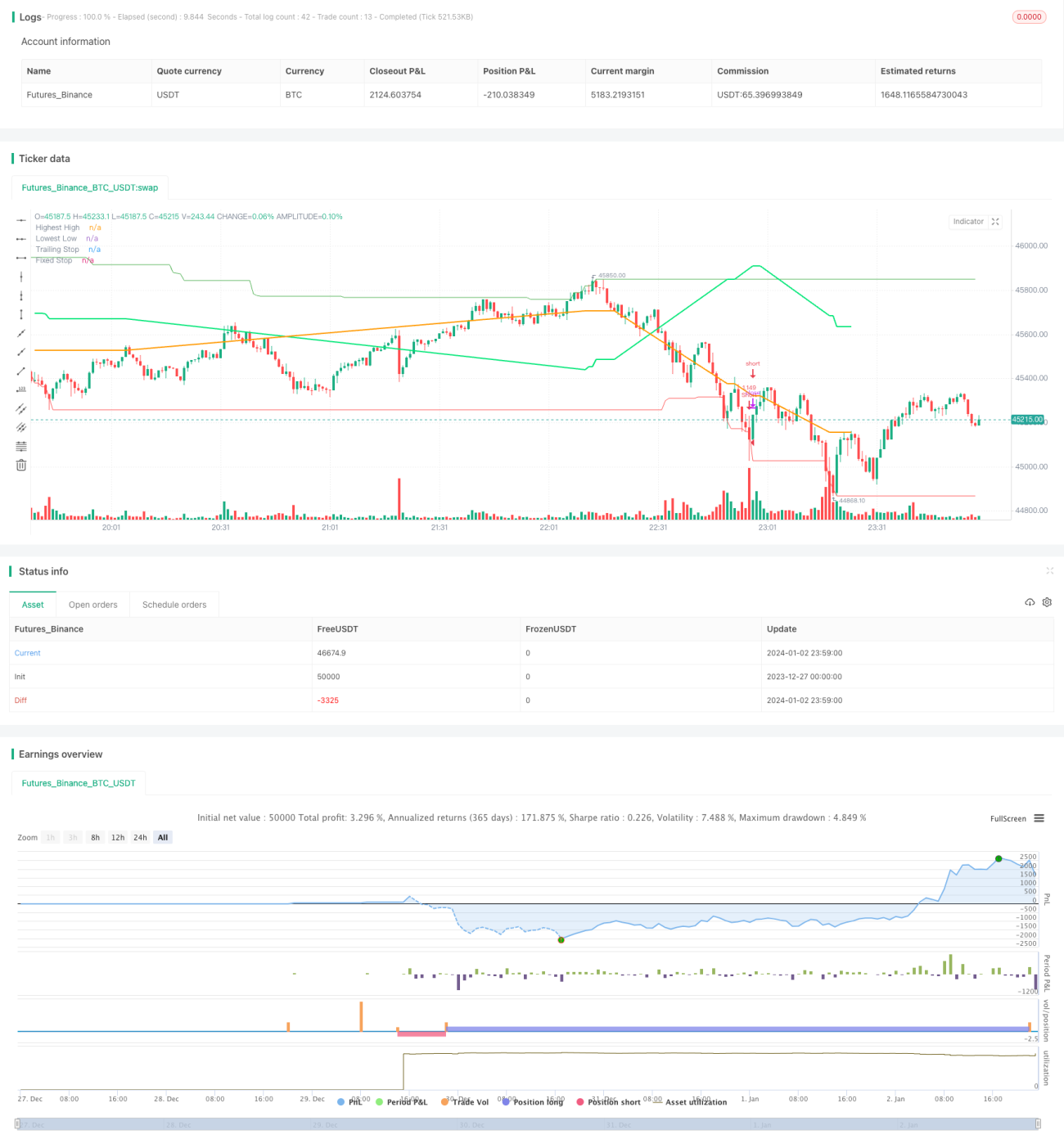

Strategi Ayunan Dwi-Trend adalah strategi perdagangan kuantitatif yang menggabungkan trend dan ayunan. Ia menggunakan gabungan dua indikator untuk mengenal pasti arah dan kekuatan trend, dan mencari masa masuk yang baik semasa pasaran bergerak dalam julat (ayunan).

Prinsip Strategi

Strategi ini terutamanya menggunakan dua indikator awam: Trend Surfers dan Mawreez's Trend Oscillator.

Trend Surfers adalah indikator henti rugi pengikut trend. Ia mengira harga tertinggi dan terendah dalam tempoh tertentu untuk menilai pergerakan harga dan mencadangkan tahap henti rugi. Contohnya, apabila harga menembusi harga tertinggi 168 bar terakhir, ia adalah isyarat kenaikan; apabila harga menembusi harga terendah 168 bar terakhir, ia adalah isyarat penurunan.

Mawreez's Trend Oscillator pula adalah indikator ayunan dwi-garisan. Ia serupa dengan MACD, menggunakan perbezaan DI untuk menilai arah dan kekuatan trend. Apabila lengkung indikator berada di atas garis sifar, ia menandakan kenaikan; di bawah garis sifar menandakan penurunan.

Peraturan dagangan strategi ini adalah:

- Masuk beli (Long): Apabila Trend Surfers menembusi garis tertinggi dan Mawreez's Trend Oscillator menunjukkan kenaikan.

- Masuk jual (Short): Apabila Trend Surfers menembusi garis terendah dan Mawreez's Trend Oscillator menunjukkan penurunan.

Kaedah henti rugi adalah gabungan henti rugi pengikut trend dan henti rugi tetap.

Analisis Kelebihan

Strategi ini menggabungkan indikator trend dan ayunan, mampu menangkap trend dan mencari harga masuk yang baik dalam pasaran julat, dengan kelebihan berikut:

- Penapisan dwi-indikator dapat mengelakkan isyarat palsu dengan berkesan.

- Gabungan trend dan ayunan memudahkan pengumpulan saham pada harga rendah dalam julat atau meletakkan kedudukan ringan pada harga tinggi.

- Pelbagai kaedah henti rugi dapat mengawal risiko dengan baik.

Analisis Risiko

Strategi ini juga mempunyai beberapa risiko:

- Gabungan dwi-indikator mudah terlepas isyarat (missed trades).

- Indikator trend dan ayunan mungkin memberi isyarat bercanggah.

- Henti rugi tetap mungkin terlalu awal (stop out prematurely).

Untuk mengelakkan risiko ini, langkah berikut boleh diambil:

- Longgarkan parameter indikator untuk mengurangkan kadar penapisan.

- Tambah peraturan penentuan trend untuk mengelakkan percanggahan isyarat.

- Laraskan tahap henti rugi secara dinamik.

Hala Tuju Pengoptimuman

Strategi ini masih mempunyai ruang untuk pengoptimuman selanjutnya:

- Uji kombinasi parameter dan kitaran masa yang berbeza untuk mencari parameter terbaik.

- Tambah peraturan bantuan seperti turun naik, volum dagangan, dsb.

- Gunakan teknik pembelajaran mesin untuk mengoptimumkan indikator dan parameter secara dinamik.

Kesimpulan

Strategi Ayunan Dwi-Trend menggabungkan kelebihan indikator pengikut trend dan ayunan. Ia dapat mengenal pasti arah trend dan merebut peluang julat. Dengan pengoptimuman parameter dan peraturan, keuntungan strategi ini dapat dipertingkatkan lagi. Strategi ini mempunyai prospek pembangunan yang baik.

- 1