Strategi kuantitatif jangka pendek berdasarkan RSI dan VWAP

Gambaran Keseluruhan

Strategi ini dinamakan "Strategi Jangka Pendek RSI-VWAP". Strategi ini menggunakan indikator RSI dan harga purata berwajaran volum (VWAP) sebagai penunjuk teknikal, menetapkan isyarat beli dan jual, seterusnya menghasilkan keputusan dagangan. Strategi ini bertujuan untuk menangkap fenomena terlebih beli dan terlebih jual pasaran dalam jangka pendek bagi meraih pulangan yang lebih tinggi.

Prinsip Strategi

- Menggunakan indikator RSI untuk menilai sama ada pasaran berada dalam keadaan terlebih beli atau terlebih jual. Nilai RSI melebihi 80 adalah zon terlebih beli, manakala di bawah 20 adalah zon terlebih jual.

- Indikator RSI menggunakan VWAP dan bukannya harga penutup sebagai sumber data. VWAP lebih mencerminkan harga purata dagangan pada hari tersebut.

- Apabila nilai RSI menaik dari zon terlebih jual melepasi 20, ia menghasilkan isyarat beli. Apabila nilai RSI menurun dari zon terlebih beli melepasi 80, ia menghasilkan isyarat jual.

- Strategi ini hanya mengambil posisi beli, tidak mengambil posisi jual. Iaitu hanya membeli semasa terlebih jual dan menjual semasa terlebih beli.

Analisis Kelebihan

- Menggunakan VWAP sebagai sumber data RSI menjadikan penilaian pasaran oleh indikator RSI lebih tepat, mengelak daripada terkeliru dengan penembusan palsu.

- Hanya mengambil posisi beli mengurangkan kekerapan dagangan, sesuai untuk memperoleh pulangan yang stabil dalam jangka panjang.

- Parameter RSI adalah 17, sesuai untuk dagangan jangka pendek.

- Mengamalkan kaedah dagangan jangka pendek dengan kekerapan transaksi yang rendah, mengurangkan kos dagangan, membantu meraih kadar pulangan yang lebih tinggi.

Analisis Risiko

- Ujian semula strategi kuantitatif mempunyai risiko overfitting, keputusan dagangan sebenar mungkin tidak sepadan dengan ujian semula.

- Hanya mengambil posisi beli tidak dapat menangkap peluang dalam pasaran menurun dengan segera.

- Kriteria terlebih beli dan terlebih jual mungkin tidak sesuai untuk semua instrumen, parameter perlu disesuaikan bagi instrumen yang berbeza.

- Mana-mana indikator teknikal boleh menghasilkan isyarat palsu, tidak dapat mengelakkan kerugian sepenuhnya.

Risiko boleh dikurangkan dengan melonggarkan kriteria terlebih beli/terlebih jual secara sederhana, menggabungkan indikator lain untuk pengesahan isyarat, dan melaraskan julat parameter.

Hala Tuju Pengoptimuman

- Menguji kesan parameter yang berbeza terhadap prestasi strategi, mengoptimumkan panjang RSI dan ambang terlebih beli/terlebih jual.

- Menambah strategi henti rugi, seperti henti rugi bergerak atau henti rugi berdasarkan masa, untuk mengunci sebahagian keuntungan dan mengurangkan pengeluaran.

- Menggabungkan indikator lain untuk penapisan isyarat, meningkatkan ketepatan isyarat.

- Menetapkan julat parameter yang berasingan berdasarkan ciri-ciri instrumen yang berbeza, membolehkan strategi menyesuaikan diri dengan lebih baik kepada pelbagai instrumen.

Kesimpulan

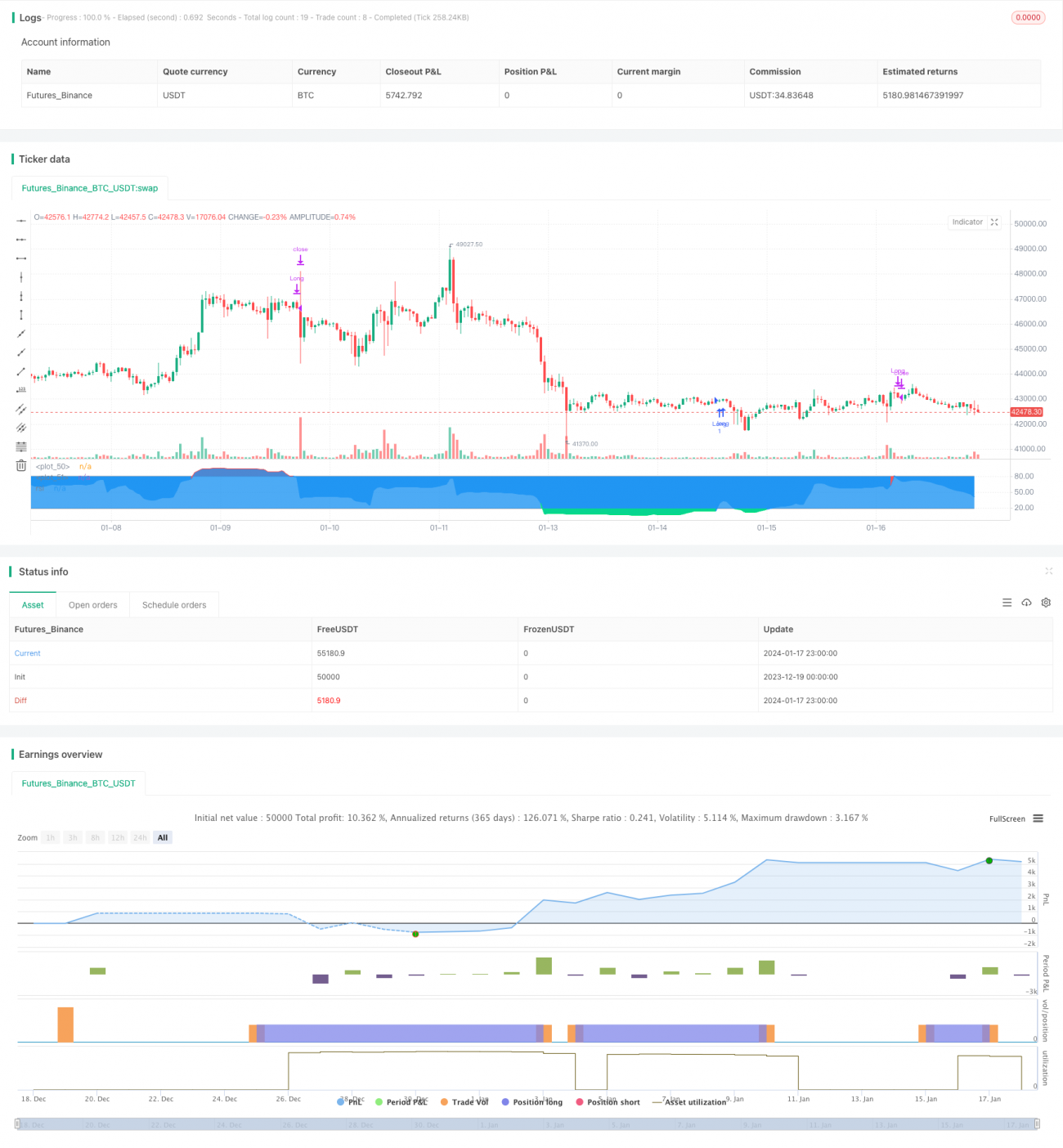

Secara keseluruhan, strategi ini adalah strategi jangka pendek yang ringkas dan praktikal. Penggunaan VWAP menjadikan penilaian indikator RSI lebih tepat, dan hanya mengambil posisi beli mengurangkan kekerapan dagangan. Strategi ini mempunyai konsep yang jelas, mudah difahami dan dilaksanakan, sesuai untuk pemula dalam dagangan kuantitatif. Walau bagaimanapun, mana-mana strategi yang bergantung pada satu indikator sukar untuk menjadi sempurna, ia masih memerlukan pengoptimuman berterusan untuk menghasilkan prestasi dagangan sebenar yang lebih baik.

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Xaviz

//#####©ÉÉÉɶN###############################################- 1