Strategi Mengikut Trend Berdasarkan Purata Bergerak

Gambaran Keseluruhan

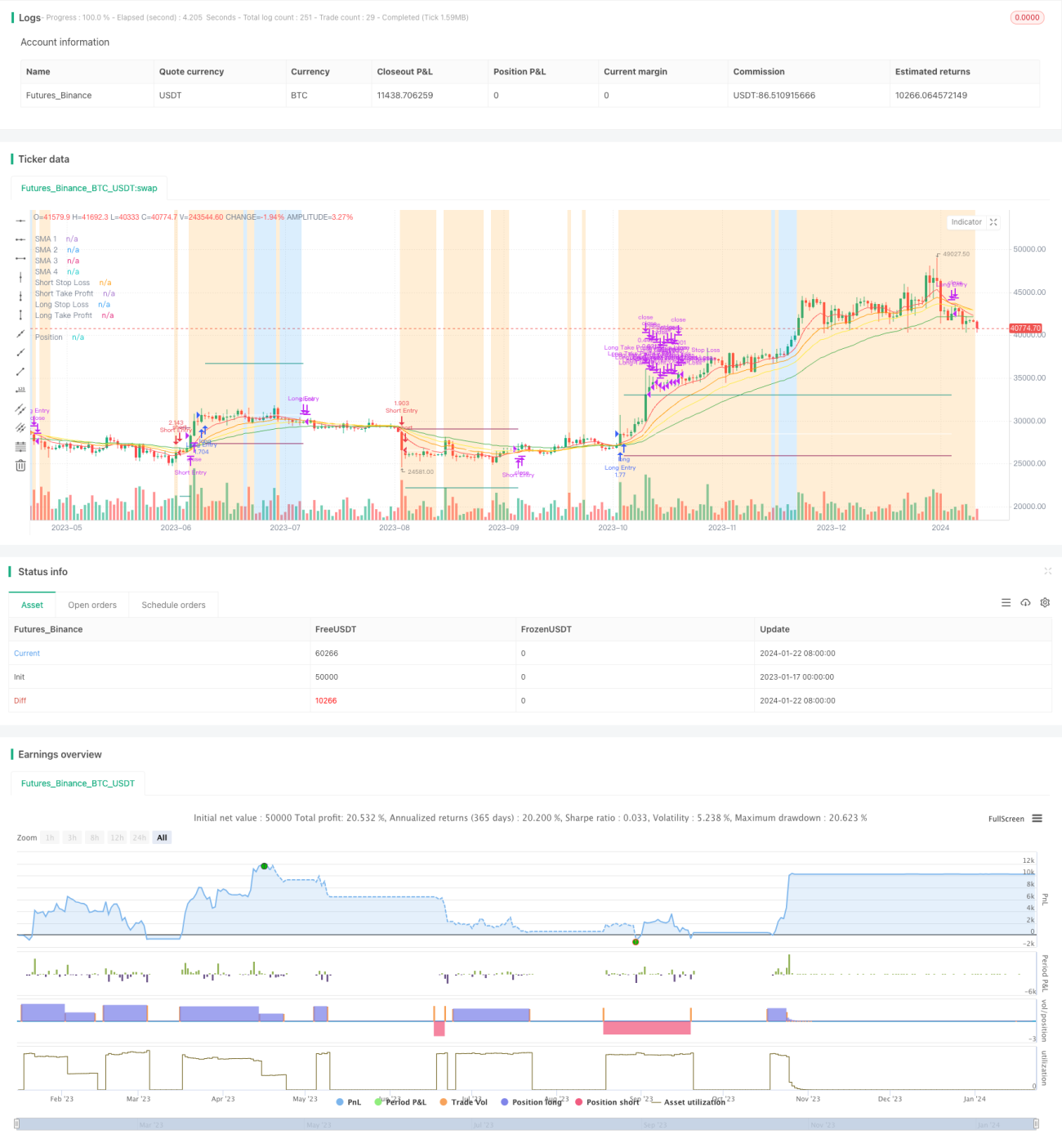

Strategi ini merupakan strategi pengikut arah aliran (trend following) yang mudah berdasarkan purata bergerak (moving average). Ia menentukan arah aliran semasa dan tempoh aliran dengan membandingkan hubungan antara saiz purata bergerak dalam tempoh yang berbeza. Apabila purata bergerak jangka pendek melintasi purata bergerak jangka panjang dari bawah ke atas, ia akan membeli (long), dan apabila purata bergerak jangka pendek melintasi purata bergerak jangka panjang dari atas ke bawah, ia akan menjual (short). Pada masa yang sama, strategi ini juga menetapkan titik henti rugi (stop loss) dan titik ambil untung (take profit) untuk mengawal risiko.

Prinsip Strategi

Strategi ini menggunakan 4 purata bergerak dengan tempoh yang berbeza: MA5, MA10, MA15 dan MA25. Keempat-empat purata bergerak ini dipanggil MA1, MA2, MA3 dan MA4. MA1 adalah yang paling pendek, manakala MA4 adalah yang paling panjang.

Apabila MA1 > MA2 > MA3 > MA4, ia menunjukkan harga berada dalam arah aliran menaik (uptrend), maka ia akan membeli (long); apabila MA1 < MA2 < MA3 < MA4, ia menunjukkan harga berada dalam arah aliran menurun (downtrend), maka ia akan menjual (short).

Keadaan untuk membuka kedudukan beli dan jual juga perlu memenuhi penapis henti rugi ATR (ATR stop filter), iaitu nilai ATR mestilah lebih besar daripada purata bergerak mudah (SMA) 40 tempoh ATR. Ini dapat mengelakkan isyarat palsu apabila turun naik harga terlalu kecil.

Kelebihan Strategi

Strategi ini mempunyai kelebihan berikut:

- Konsep yang mudah difahami dan mudah dilaksanakan.

- Menggunakan beberapa kumpulan purata bergerak untuk menentukan arah aliran adalah boleh dipercayai.

- Menetapkan titik ambil untung dan henti rugi dapat mengawal kerugian maksimum bagi setiap transaksi dengan berkesan.

- Penapis henti rugi ATR dapat mengelakkan isyarat palsu apabila turun naik harga terlalu kecil.

Analisis Risiko

Strategi ini juga mempunyai risiko berikut:

- Dalam pasaran yang sangat tidak menentu (oscillating market), ia mudah menghasilkan isyarat palsu.

- Penetapan parameter (tempoh purata bergerak, dll.) yang tidak sesuai boleh menyebabkan prestasi strategi yang kurang baik.

- Tidak mengambil kira kesan asas (fundamental) dan berita penting terhadap harga.

Untuk mengurangkan risiko ini, parameter boleh dioptimumkan dengan sewajarnya, atau menambah syarat penapis lain untuk meningkatkan kestabilan strategi.

Arah Pengoptimuman

Arah pengoptimuman strategi ini termasuk:

- Menguji kombinasi parameter tempoh purata bergerak yang berbeza untuk mencari parameter terbaik.

- Menambah penapis penunjuk teknikal lain, seperti MACD, KDJ, dll. untuk menilai kebolehpercayaan isyarat.

- Menambah penapis volum dagangan, hanya berdagang apabila volum dagangan meningkat.

- Melakukan pengoptimuman parameter yang terperinci mengikut perbezaan parameter bagi setiap instrumen.

- Menambah algoritma pembelajaran mesin untuk menilai isyarat.

Kesimpulan

Secara keseluruhannya, strategi ini adalah strategi pengikut arah aliran yang agak mudah, yang menentukan arah aliran melalui purata bergerak dan menetapkan ambil untung serta henti rugi yang munasabah untuk mengawal tahap risiko. Ruang pengoptimuman strategi ini masih besar. Melalui pelarasan parameter, penambahan penapis dan cara lain, kestabilan dan keuntungan strategi dapat dipertingkatkan lagi.

- 1