Strategi Perdagangan Ayunan Sokongan dan Rintangan

1

Follow

1802

Followers

Gambaran Keseluruhan

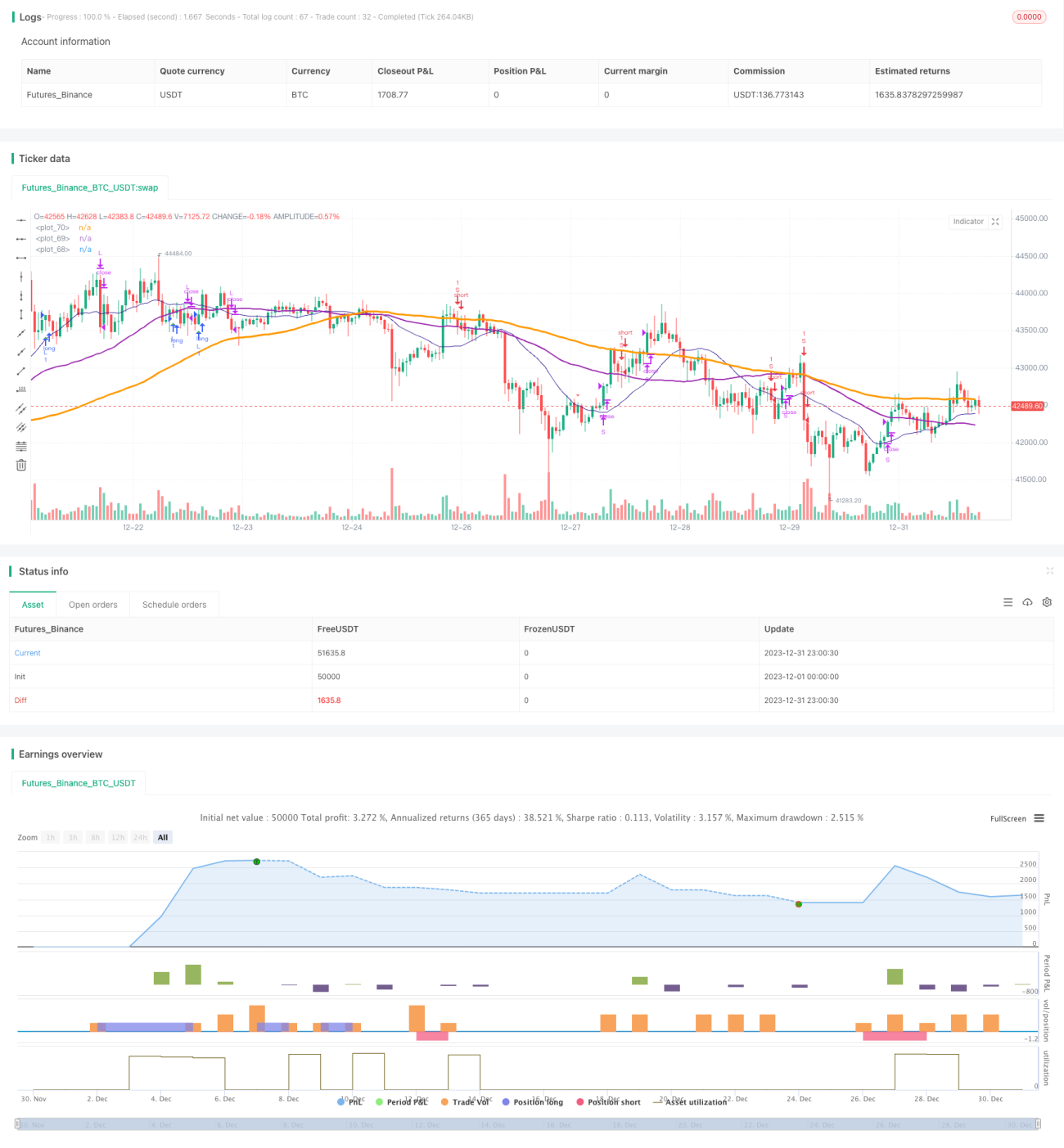

Strategi ini menggabungkan strategi persilangan RSI dan Stokastik dengan strategi pengoptimuman gelinciran penutupan posisi, untuk mencapai kawalan tepat logik dagangan dan henti rugi/ambil untung yang tepat. Pada masa yang sama, melalui pengenalan pengoptimuman isyarat, ia dapat mengawal arah aliran dengan lebih baik dan mencapai pengurusan modal yang rasional.

Prinsip Strategi

- Penunjuk RSI menentukan zon terlebih beli/terlebih jual, digabungkan dengan persilangan emas dan persilangan maut nilai K dan D penunjuk Stokastik untuk membentuk isyarat dagangan.

- Pengenalan pola pecahan pada lilin (candlestick fractal) digunakan untuk membantu menentukan isyarat arah aliran dan mengelakkan dagangan yang salah.

- Purata bergerak SMA membantu dalam menentukan arah aliran. Apabila purata bergerak jangka pendek menembusi purata bergerak jangka panjang dari bawah ke atas, ia adalah isyarat kenaikan harga.

- Strategi gelinciran penutupan posisi: menetapkan harga henti rugi dan ambil untung berdasarkan julat pergerakan harga tertinggi dan terendah.

Analisis Kelebihan

- Pengoptimuman parameter RSI yang baik dalam menentukan zon terlebih beli/terlebih jual, mengelakkan dagangan yang salah.

- Pengoptimuman parameter STO (Stokastik): pelarasan parameter kelicinan dapat menapis hingar dan meningkatkan kualiti isyarat.

- Pengenalan analisis teknikal Heikin-Ashi untuk mengenal pasti perubahan arah badan lilin, memastikan ketepatan isyarat dagangan.

- Purata bergerak SMA membantu menentukan arah aliran utama, mengelakkan dagangan menentang arah aliran.

- Menggabungkan strategi gelinciran henti rugi/ambil untung dapat memaksimumkan penguncian keuntungan setiap dagangan.

Analisis Risiko

- Apabila pasaran terus menurun, modal berdepan risiko yang besar.

- Kekerapan dagangan mungkin terlalu tinggi, meningkatkan kos dagangan dan kos gelinciran.

- Penunjuk RSI mudah menghasilkan isyarat palsu, perlu digabungkan dengan penunjuk lain untuk penapisan.

Pengoptimuman Strategi

- Laraskan parameter RSI untuk mengoptimumkan penentuan terlebih beli/terlebih jual.

- Laraskan parameter penunjuk STO (Stokastik) – kelicinan dan tempoh – untuk meningkatkan kualiti isyarat.

- Laraskan tempoh purata bergerak untuk mengoptimumkan penentuan arah aliran.

- Perkenalkan lebih banyak penunjuk teknikal untuk meningkatkan ketepatan penentuan isyarat.

- Optimumkan nisbah henti rugi/ambil untung untuk mengurangkan risiko setiap dagangan.

Ringkasan

Strategi ini mengintegrasikan kelebihan pelbagai penunjuk teknikal utama, melalui pengoptimuman parameter dan penambahbaikan peraturan, mencapai keseimbangan antara kualiti isyarat dagangan dan henti rugi/ambil untung. Ia mempunyai kebolehgunaan umum dan keupayaan keuntungan yang stabil. Melalui pengoptimuman berterusan, kadar kemenangan dan kadar keuntungan dapat ditingkatkan lagi.

Source

Pine

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//study(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true)

strategy(title="@sentenzal strategy", shorttitle="@sentenzal strategy", overlay=true )

smoothK = input(3, minval=1)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1