Strategi Perdagangan Cawan Sedut Penunjuk RSI

Gambaran Keseluruhan

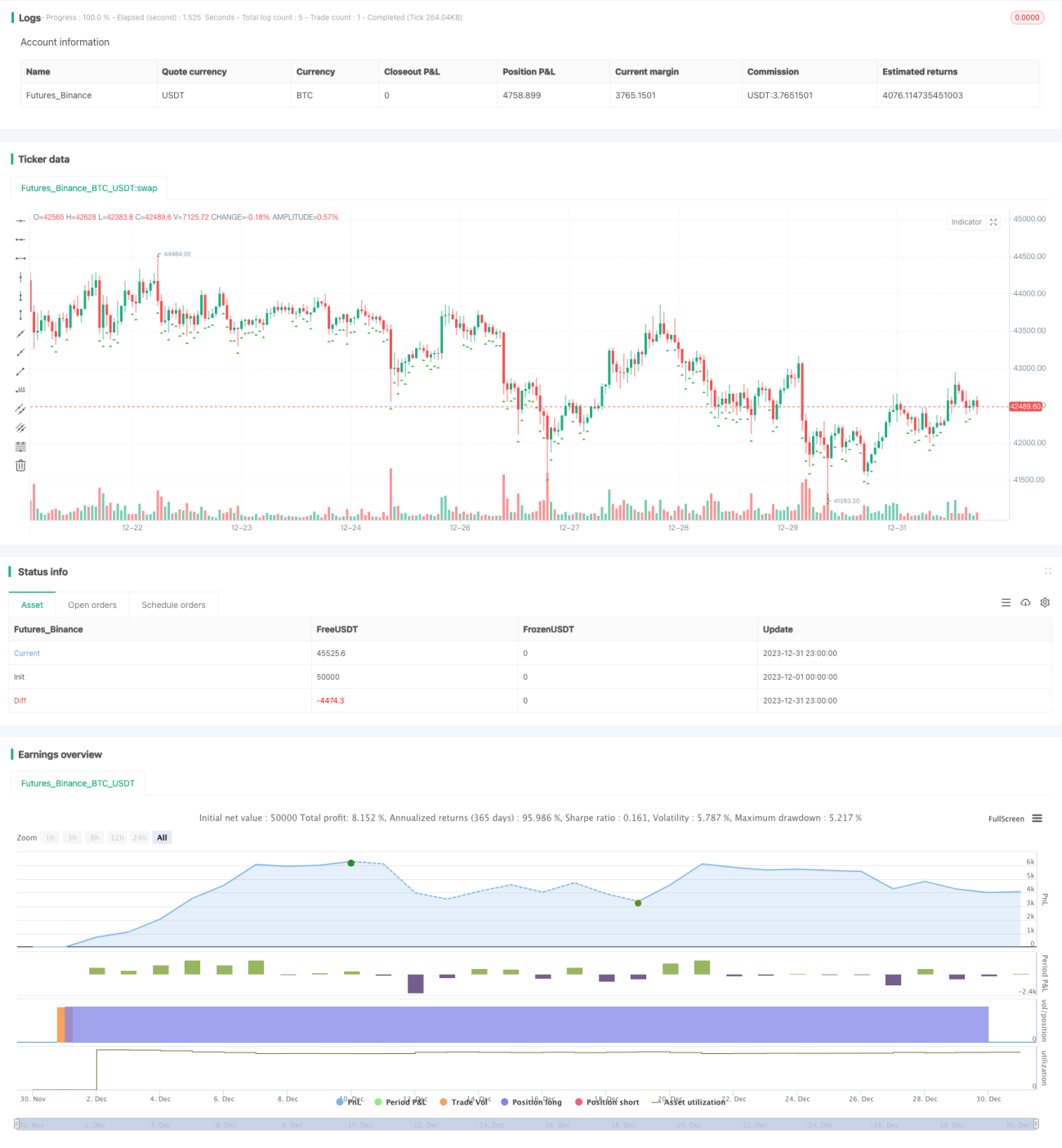

Strategi dagangan indikator RSI adalah kaedah dagangan grid tetap yang mengintegrasikan indikator RSI dan CCI. Strategi ini menentukan masa masuk berdasarkan nilai indikator RSI dan CCI, menggunakan nisbah keuntungan tetap dan bilangan grid tetap untuk menetapkan pesanan ambil untung dan pesanan tambah. Pada masa yang sama, strategi ini juga mengintegrasikan mekanisme lindung nilai terhadap perubahan harga yang menembus.

Prinsip Strategi

Syarat Masuk

Apabila indikator RSI 5 minit dan 30 minit kedua-duanya di bawah ambang yang ditetapkan, manakala indikator CCI 1 jam juga di bawah nilai yang ditetapkan, isyarat beli dihasilkan. Pada masa ini, harga close semasa direkodkan sebagai harga masuk, dan saiz lot pertama dikira berdasarkan ekuiti akaun dan bilangan grid.

Syarat Ambil Untung

Berdasarkan harga masuk, harga untung dikira mengikut nisbah keuntungan sasaran yang ditetapkan. Pesanan ambil untung diletakkan pada tahap harga tersebut.

Syarat Tambah Posisi

Selain lot pertama, pesanan tambah posisi untuk baki lot tetap akan dikeluarkan satu demi satu selepas isyarat masuk sehingga bilangan grid yang ditetapkan dicapai.

Mekanisme Lindung Nilai

Jika harga meningkat melebihi peratusan ambang lindung nilai yang ditetapkan berbanding harga masuk, semua posisi akan dilindung nilai dan ditutup.

Mekanisme Pembalikan

Jika harga menurun melebihi peratusan ambang pembalikan yang ditetapkan berbanding harga masuk, semua pesanan yang belum diisi akan dibatalkan, menunggu peluang masuk baharu.

Analisis Kelebihan

- Menggabungkan indikator RSI dan CCI untuk meningkatkan kebarangkalian keuntungan

- Menggunakan grid tetap untuk menetapkan sasaran keuntungan, meningkatkan kepastian keuntungan

- Mengintegrasikan mekanisme lindung nilai untuk mencegah risiko turun naik harga yang melampau secara berkesan

- Menambahkan mekanisme pembalikan untuk mengurangkan kerugian

Analisis Risiko

- Kebarangkalian isyarat palsu daripada indikator

- Turun naik harga melampau yang menembusi ambang lindung nilai

- Selepas pembalikan, harga mungkin tidak dapat masuk semula

Risiko ini boleh dikurangkan dengan melaraskan parameter indikator, memperluas julat lindung nilai, dan mengurangkan julat pembalikan.

Arah Pengoptimuman

- Boleh menguji lebih banyak kombinasi indikator

- Boleh mengkaji mekanisme ambil untung adaptif

- Boleh mengoptimumkan logik tambah posisi

Ringkasan

Strategi dagangan indikator RSI menentukan masa masuk melalui indikator, menggunakan grid tetap untuk ambil untung dan tambah posisi bagi mengunci keuntungan stabil. Pada masa yang sama, strategi ini mempunyai mekanisme lindung nilai terhadap turun naik besar dan mekanisme masuk semula selepas pembalikan. Strategi yang mengintegrasikan pelbagai mekanisme ini boleh digunakan untuk mengurangkan risiko dagangan dan meningkatkan kadar keuntungan. Dengan pengoptimuman lanjut terhadap indikator dan parameter, prestasi dagangan sebenar yang lebih baik boleh dicapai.

- 1