Strategi Perdagangan Ikut Arah Aliran Berasaskan Pengayun Volum

Gambaran Keseluruhan

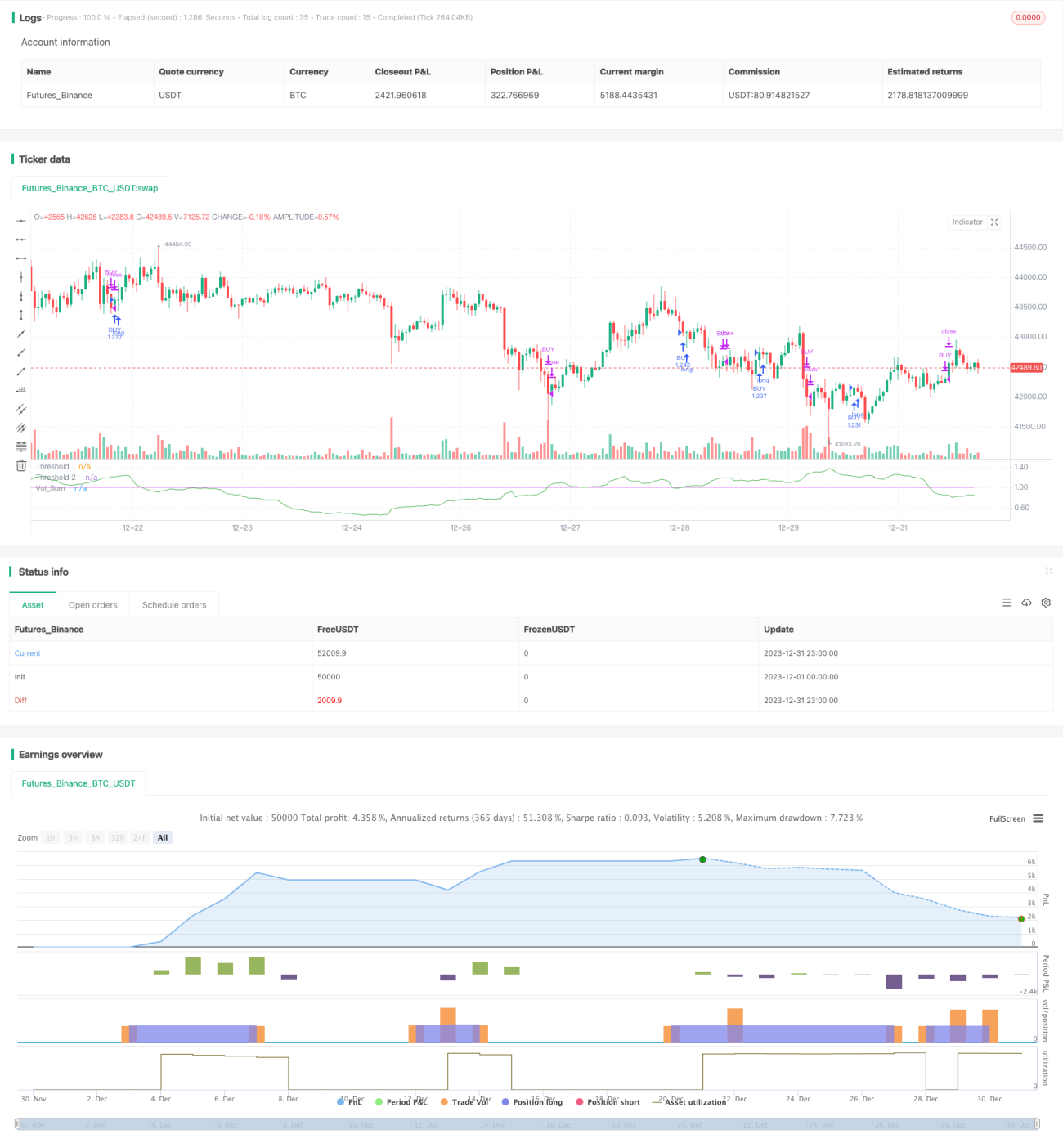

Strategi ini adalah strategi pengikut arah aliran yang berdagang berdasarkan penunjuk pengayun volum yang diubah suai. Ia menggunakan purata bergerak volum untuk mengenal pasti isyarat peningkatan volum, sekali gus menentukan masa untuk masuk atau keluar dari kedudukan. Ia juga menggabungkan penilaian arah aliran harga itu sendiri untuk mengelakkan isyarat palsu semasa pasaran tidak menentu.

Prinsip Strategi

- Kira purata bergerak volum vol_sum dengan panjang vol_length, dan lakukan pelicinan purata bergerak dengan panjang vol_smooth.

- Apabila vol_sum meningkat melebihi ambang threshold, ia menghasilkan isyarat beli; apabila ia menurun melebihi ambang, ia menghasilkan isyarat jual.

- Untuk menapis operasi yang salah, beli hanya apabila harga sedang dalam arah aliran menaik, berbanding dengan harga tutup dalam batang lilin yang lalu sebanyak direction batang lilin. Jual hanya apabila harga sedang dalam arah aliran menurun.

- Tetapkan dua ambang: threshold dan threshold2. threshold digunakan untuk menghasilkan isyarat perdagangan, manakala threshold2 digunakan untuk henti rugi.

- Uruskan logik buka dan tutup pesanan melalui mesin keadaan.

Analisis Kelebihan

- Menggunakan penunjuk volum membolehkan menangkap perubahan daya beli dan jual pasaran, seterusnya meningkatkan ketepatan isyarat.

- Menggabungkan penilaian arah aliran harga dapat mengelakkan isyarat palsu semasa harga tidak menentu.

- Menggunakan dua ambang untuk buka kedudukan dan henti rugi membolehkan kawalan risiko yang lebih baik.

Analisis Risiko

- Penunjuk volum itu sendiri mempunyai ketinggalan, yang mungkin menyebabkan terlepas titik perubahan harga.

- Tetapan parameter yang salah boleh menyebabkan kekerapan perdagangan terlalu tinggi atau isyarat menjadi lewat.

- Dalam senario di mana volum melonjak secara mendadak, titik henti rugi mungkin dilanggar.

Risiko-risiko ini boleh dikawal dengan melaraskan parameter, mengoptimumkan kaedah pengiraan penunjuk, dan menggabungkan penunjuk lain untuk pengesahan.

Arah Pengoptimuman

- Boleh mempertimbangkan untuk mengoptimumkan parameter penunjuk secara adaptif, melaraskan secara automatik mengikut keadaan pasaran.

- Boleh menggabungkan penunjuk lain, seperti indeks ayunan harga, untuk mengesahkan isyarat lagi dan meningkatkan ketepatan.

- Boleh mengkaji penggunaan model pembelajaran mesin dalam pertimbangan isyarat, menggunakan model untuk meningkatkan ketepatan.

Ringkasan

Strategi ini, melalui pengayun volum yang diperbaiki, dibantu oleh penilaian arah aliran harga, dan menetapkan dua ambang untuk buka kedudukan dan henti rugi, secara keseluruhannya adalah strategi pengikut arah aliran yang agak stabil. Ruang pengoptimuman terletak terutamanya pada pelarasan parameter, penapisan isyarat, dan strategi henti rugi. Secara keseluruhannya, strategi ini mempunyai nilai praktikal dan wajar dikaji serta dioptimumkan selanjutnya.

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy('Volume Advanced', default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=0.075, currency='USD')

startP = timestamp(input(2017, "Start Year"), input(12, "Start Month"), input(17, "Start Day"), 0, 0)

end = timestamp(input(9999, "End Year"), input(1, "End Month"), input(1, "End Day"), 0, 0)- 1