Strategi Perdagangan Garis Trend Cerun Dinamik

Gambaran Keseluruhan

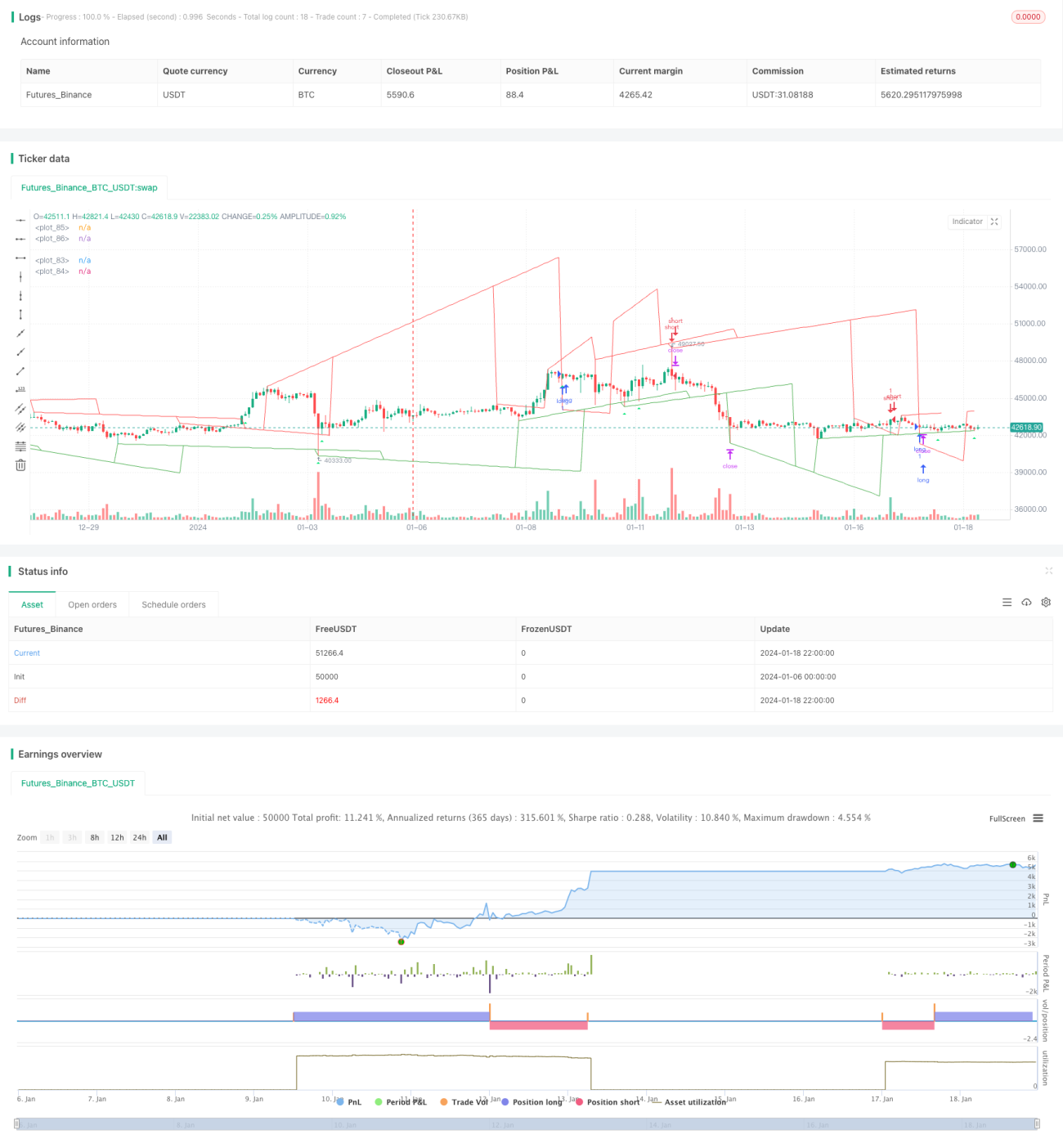

Idea utama strategi ini adalah menggunakan cerun dinamik untuk menilai arah aliran harga, digabungkan dengan penembusan untuk menghasilkan isyarat dagangan. Secara khususnya, ia akan menjejaki paras tertinggi dan terendah harga baharu secara masa nyata, mengira cerun dinamik berdasarkan perubahan harga dalam tempoh masa yang berbeza, dan kemudian menggabungkan penembusan harga terhadap garis arah aliran untuk menentukan isyarat beli atau jual.

Prinsip Strategi

Strategi ini terbahagi kepada beberapa langkah utama:

-

Menentukan harga tertinggi dan terendah: Menjejaki harga tertinggi dan terendah dalam tempoh tertentu (contohnya 20 batang lilin) untuk menentukan sama ada ia mencapai paras tertinggi atau terendah baharu.

-

Mengira cerun dinamik: Mencatat nombor lilin apabila harga mencapai tertinggi atau terendah baharu, dan mengira cerun dinamik dari titik tertinggi/terendah tersebut ke titik tertinggi/terendah selepas tempoh tertentu (contohnya 9 batang lilin).

-

Melukis garis arah aliran: Melukis garis arah aliran menaik dan menurun berdasarkan cerun dinamik.

-

Memanjangkan dan mengemas kini garis arah aliran: Apabila harga menembusi garis arah aliran, garis tersebut akan dipanjangkan dan dikemas kini.

-

Isyarat dagangan: Menggabungkan penembusan harga terhadap garis arah aliran untuk menentukan isyarat beli dan jual.

Kelebihan Strategi

Strategi ini mempunyai kelebihan berikut:

- Menilai arah aliran secara dinamik, responsif terhadap perubahan pasaran.

- Dapat mengawal stop loss dengan baik, mengurangkan pengeluaran.

- Isyarat dagangan penembusan yang jelas, mudah dilaksanakan.

- Parameter boleh disesuaikan, kebolehsuaian tinggi.

- Struktur kod yang jelas, mudah difahami dan dibangunkan semula.

Risiko dan Penyelesaian

Strategi ini juga mempunyai beberapa risiko:

- Apabila arah aliran berombak, isyarat mungkin palsu; cadangan menambah penapis.

- Isyarat penembusan palsu mungkin kerap; boleh laraskan parameter atau tambah penapis.

- Risiko stop loss semasa pergerakan harga yang mendadak; boleh tingkatkan lebar stop loss.

- Ruang pengoptimuman terhad, keuntungan mungkin terhad; sesuai untuk dagangan jangka pendek.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dalam aspek berikut:

- Menambah lebih banyak penunjuk teknikal untuk menapis isyarat.

- Mengoptimumkan kombinasi parameter untuk mencari parameter terbaik.

- Mencuba memperbaiki strategi stop loss untuk mengurangkan risiko.

- Menambah fungsi pelarasan automatik untuk lebar kemasukan.

- Mencuba menggabungkan dengan strategi lain untuk mencari lebih banyak peluang.

Kesimpulan

Secara keseluruhannya, strategi ini adalah strategi dagangan jangka pendek yang cekap berdasarkan cerun dinamik untuk menilai arah aliran dan berdagang pada penembusan. Ia mempunyai ketepatan penilaian yang baik, risiko terkawal, dan sesuai untuk merebut peluang jangka pendek dalam pasaran. Dengan mengoptimumkan parameter dan menambah penapis, kadar kemenangan dan tahap keuntungan strategi dapat ditingkatkan.

/*backtest

start: 2024-01-06 00:00:00

end: 2024-01-19 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © pune3tghai

//Originally posted by matsu_bitmex- 1