Strategi Penembusan Kenaikan Berdasarkan Bollinger Bands dan VWAP

Gambaran Keseluruhan

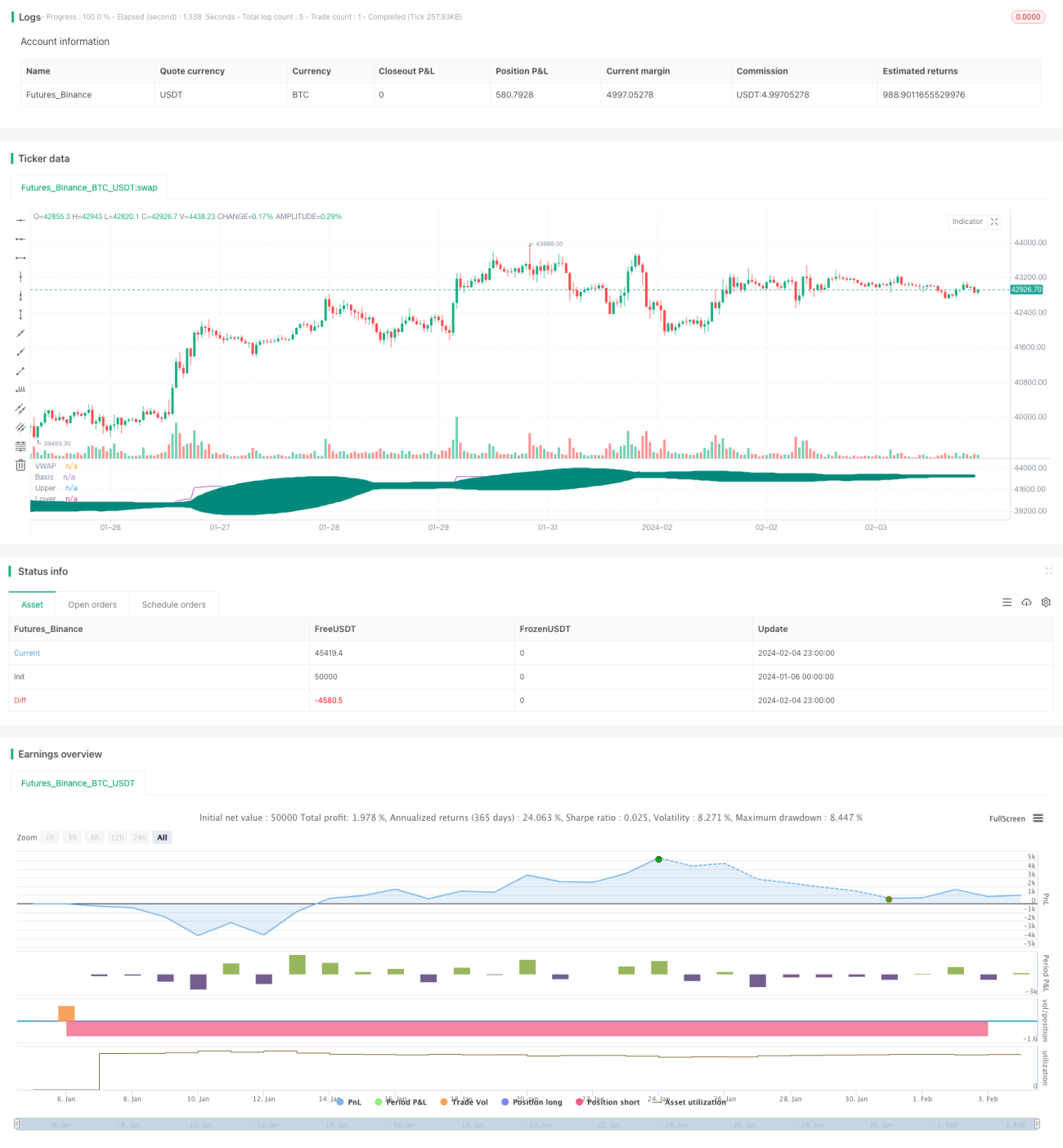

Strategi ini menggunakan penunjuk Bollinger Bands untuk menjejaki VWAP. Apabila VWAP menembusi ke atas garis tengah Bollinger Bands, ia dianggap sebagai penembusan kenaikan (bullish) dan strategi beli (long) diambil. Manakala apabila VWAP menembusi ke bawah garis bawah Bollinger Bands, ia dianggap sebagai pengesahan penurunan (bearish) dan posisi ditutup. Pada masa yang sama, strategi ini juga memperkenalkan tahap sokongan utama Pivot Point sebagai syarat bantuan untuk isyarat masuk, dengan itu dapat menapis beberapa penembusan palsu.

Prinsip Strategi

- Kira nilai VWAP.

- Kira Bollinger Bands untuk VWAP, termasuk garis atas, garis tengah, dan garis bawah.

- Tentukan sama ada VWAP menembusi ke atas garis tengah Bollinger Bands. Jika ya dan harga berada di atas tahap sokongan utama Pivot Point, maka posisi beli (long) diambil.

- Stop loss ditetapkan pada 5%.

- Jika VWAP menembusi ke bawah garis bawah Bollinger Bands, ia dianggap bahawa penurunan telah disahkan dan posisi ditutup. Jika stop loss tercetus, juga keluar.

Analisis Kelebihan

- VWAP mempunyai keupayaan mengikut arah aliran yang kuat; digabungkan dengan Bollinger Bands, ia dapat mengenal pasti permulaan arah aliran dengan tepat.

- Menambah Pivot Point sebagai syarat bantuan boleh menapis banyak penembusan palsu, mengelakkan kerugian yang tidak perlu.

- Menggunakan strategi keluar separa boleh mengunci sebahagian keuntungan dan mengawal risiko.

- Keputusan ujian semula menunjukkan bahawa strategi ini menunjukkan prestasi cemerlang dalam pasaran bull dan mempunyai kestabilan yang tinggi.

Analisis Risiko

- Dalam pasaran yang tidak menentu (sideways), mudah berlaku penembusan palsu yang menyebabkan kerugian.

- Pivot Point tidak dapat mengelakkan sepenuhnya penembusan palsu; perlu digabungkan dengan lebih banyak indikator untuk menapis isyarat.

- Keluar separa meningkatkan kekerapan dagangan dan juga meningkatkan kos transaksi.

- Dalam pasaran bear, prestasinya tidak ideal; perlu melakukan kawalan risiko yang baik.

Arah Pengoptimuman

- Boleh menggabungkan indikator lain seperti MACD, KDJ untuk membantu menapis isyarat masuk dan keluar.

- Boleh mencari kombinasi parameter optimum dengan mengoptimumkan panjang dan sisihan piawai Bollinger Bands.

- Boleh memperkenalkan algoritma pembelajaran mesin untuk mengoptimumkan parameter Bollinger Bands secara dinamik.

- Boleh menguji pelbagai tahap stop loss untuk mencari titik stop loss yang optimum.

- Boleh menambah mekanisme keluar adaptif yang menyesuaikan sasaran keuntungan mengikut tahap turun naik pasaran.

Kesimpulan

Secara keseluruhan, strategi ini adalah sistem penembusan yang stabil. Cara operasinya yang standard dan ruang pengoptimuman parameter yang luas menjadikannya sesuai untuk perdagangan kuantitatif. Walau bagaimanapun, perhatian juga perlu diberikan kepada kawalan risiko untuk mengelakkan kerugian akibat pasaran yang tidak normal. Secara keseluruhannya, ia adalah strategi penembusan yang layak untuk dikaji secara mendalam dan dioptimumkan secara berterusan.

- 1