Strategi Kedudukan Kompaun Pecah Keluar Isipadu Tinggi

Gambaran Keseluruhan

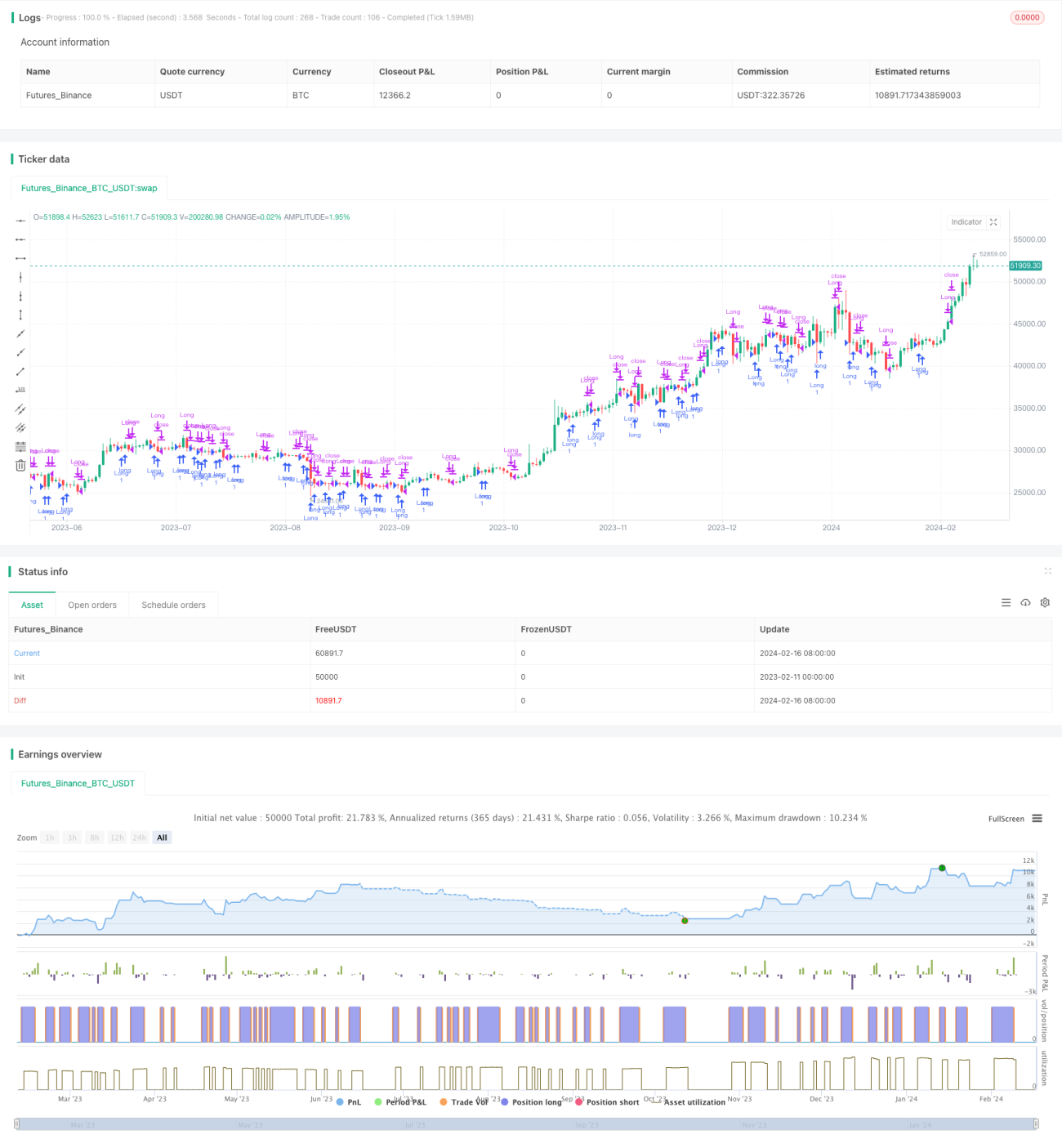

Strategi ini berteraskan kepada pengesanan penembusan dalam keadaan volum dagangan yang tinggi, dengan menetapkan peratusan belanjawan risiko dan leveraj simulasi 250x untuk mencapai kedudukan faedah kompaun. Ia bertujuan untuk merebut peluang pembalikan yang berpotensi selepas tekanan jualan yang tinggi.

Prinsip Strategi

Kemasukan posisi beli (long) berlaku apabila syarat berikut dipenuhi:

- Volum melebihi ambang yang ditentukan pengguna (volThreshold)

- Harga terendah lilin semasa lebih rendah daripada harga terendah lilin sebelumnya (lowLowerThanPrevBar)

- Lilin semasa ditutup pada harga negatif, tetapi lebih tinggi daripada harga tutup lilin sebelumnya (negativeCloseWithHighVolume)

- Tiada posisi beli terbuka (strategy.position_size == 0)

Saiz kedudukan dikira seperti berikut:

- Jumlah risiko dikira berdasarkan peratusan risiko (riskPercentage) daripada ekuiti (equity) akaun

- Jumlah risiko didarabkan dengan gandaan leveraj simulasi (leverage, lalai 250x) untuk mendapatkan kuantiti kontrak

Prinsip keluar:

Apabila peratus untung/rugi posisi beli (posProfitPct) menyentuh garisan henti rugi (-0.14%) atau garisan ambil untung (4.55%), kedudukan ditutup.

Analisis Kelebihan

Kelebihan strategi ini termasuk:

- Merebut peluang pembalikan arah aliran yang didorong oleh volum tinggi

- Menggunakan pengurusan kedudukan faedah kompaun, pertumbuhan keuntungan yang pesat

- Penetapan henti rugi dan ambil untung yang munasabah, membantu dalam kawalan risiko

Analisis Risiko

Strategi ini juga mempunyai beberapa risiko:

- Leveraj 250x boleh membesarkan kerugian

- Tidak mengambil kira faktor dagangan sebenar seperti gelinciran, yuran transaksi dan margin

- Memerlukan ujian semula (backtest) berulang untuk mengoptimumkan parameter, dan pengesahan secara dagangan sebenar

Langkah-langkah untuk mengurangkan risiko:

- Mengurangkan gandaan leveraj secara sesuai

- Menambah amplitud henti rugi

- Mempertimbangkan kos dagangan sebenar

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari aspek berikut:

- Melaraskan saiz leveraj secara dinamik

- Mengoptimumkan syarat henti rugi dan ambil untung

- Menambahkan penapis arah aliran

- Melaraskan parameter berdasarkan ciri-ciri saham tertentu

Kesimpulan

Secara keseluruhan, strategi ini agak mudah dan terus terang, bertujuan untuk memperoleh pulangan lebihan dengan merebut peluang pembalikan. Walau bagaimanapun, ia juga membawa risiko tertentu dan memerlukan pengesahan dagangan sebenar yang berhati-hati. Melalui pengoptimuman parameter dan struktur strategi, ia boleh menjadi lebih stabil dan lebih praktikal untuk dagangan sebenar.

/*backtest

start: 2023-02-11 00:00:00

end: 2024-02-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("High Volume Low Breakout (Compounded Position Size)", overlay=true, initial_capital=1000)

// Define input for volume threshold- 1