Strategi Rujukan Aliran Menaik Jenis Pecahan

Gambaran Keseluruhan

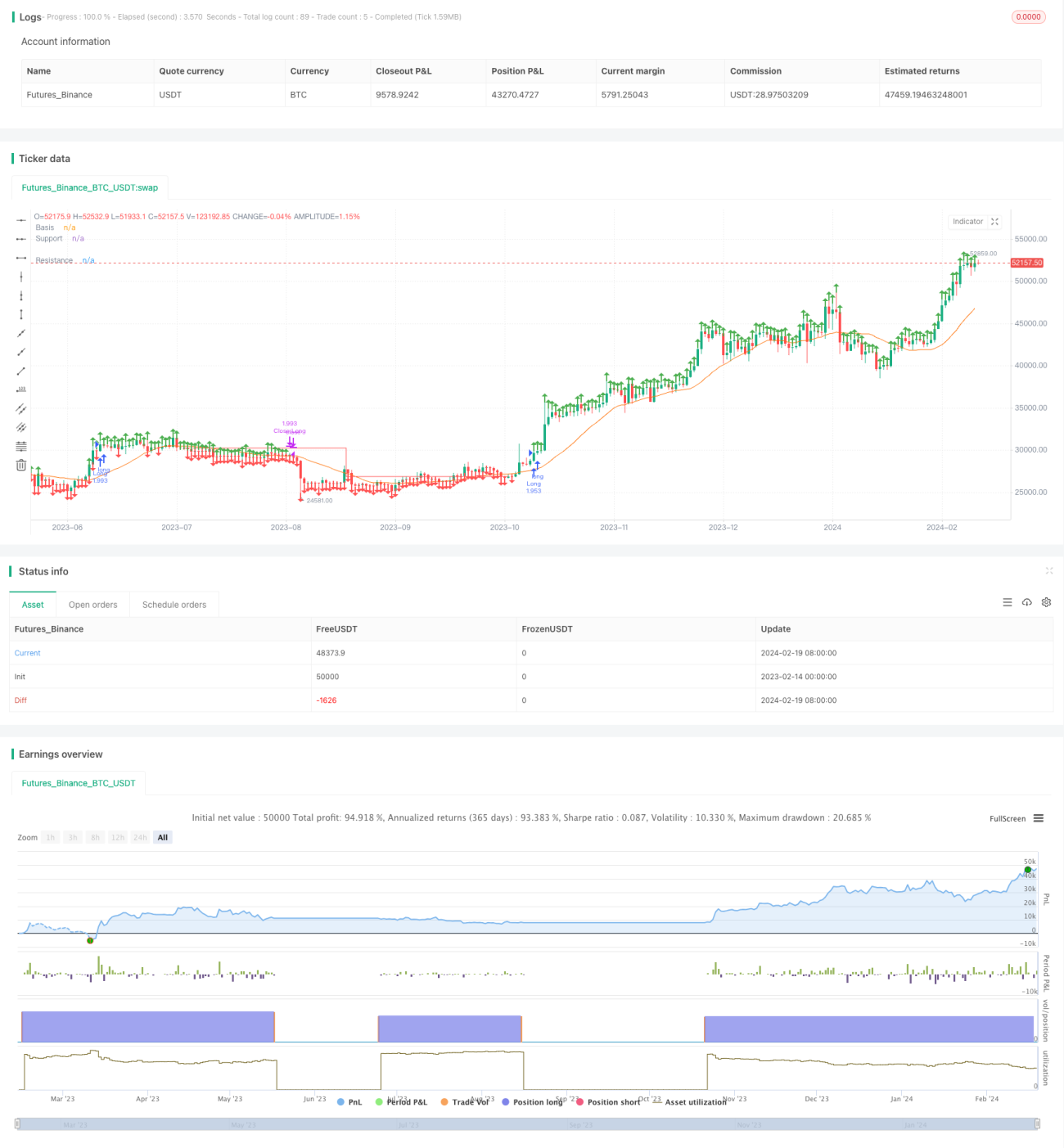

Strategi ini adalah strategi pegangan jangka panjang berdasarkan purata bergerak mudah untuk menentukan arah arah aliran, digabungkan dengan garis rintangan dan sokongan untuk membentuk isyarat penembusan. Dengan mengira titik pivot tinggi dan titik pivot rendah, garis rintangan dan garis sokongan diplot. Apabila harga menembusi garis rintangan, posisi beli dibuka; apabila harga menembusi garis sokongan, posisi ditutup. Strategi ini sesuai untuk saham yang mempunyai arah aliran yang jelas dan dapat memberikan nisbah risiko-pulangan yang baik.

Prinsip Strategi

- Kira purata bergerak mudah 20 hari sebagai garis asas untuk menentukan arah aliran.

- Kira titik pivot tinggi dan titik pivot rendah berdasarkan parameter input pengguna.

- Plot garis rintangan dan garis sokongan berdasarkan titik pivot tinggi dan titik pivot rendah.

- Apabila harga penutup lebih tinggi daripada garis rintangan, buka posisi beli.

- Apabila garis sokongan menembusi garis rintangan, tutup posisi.

Strategi ini menggunakan purata bergerak mudah untuk menentukan arah aliran keseluruhan, dan kemudian menggunakan penembusan titik utama untuk membentuk isyarat dagangan. Ia adalah strategi penembusan yang tipikal. Dengan penentuan titik utama dan arah aliran, ia dapat menapis penembusan palsu dengan berkesan.

Analisis Kelebihan

- Peluang strategi yang mencukupi, sesuai untuk saham yang berubah-ubah tinggi, mudah menangkap arah aliran.

- Kawalan risiko yang baik, nisbah risiko-pulangan yang tinggi.

- Menggunakan isyarat penembusan untuk mengelakkan risiko penembusan palsu.

- Parameter boleh disesuaikan, kebolehsuaian yang tinggi.

Analisis Risiko

- Bergantung pada pengoptimuman parameter; parameter yang tidak sesuai akan meningkatkan kebarangkalian penembusan palsu.

- Isyarat penembusan mengalami kelewatan, mungkin terlepas sebahagian peluang.

- Mudah terhenti rugi dalam pasaran yang tidak menentu.

- Pelarasan garis sokongan yang tidak tepat pada masanya boleh menyebabkan kerugian.

Risiko boleh dikurangkan melalui pengoptimuman parameter secara langsung dan menggabungkan strategi stop loss dan take profit.

Arah Pengoptimuman

- Optimumkan parameter kitaran purata bergerak.

- Optimumkan parameter garis sokongan dan rintangan.

- Tambah strategi stop loss dan take profit.

- Tambah mekanisme pengesahan penembusan.

- Gabungkan penunjuk seperti volum dagangan untuk menapis isyarat.

Ringkasan

Secara keseluruhan, strategi ini adalah strategi penembusan yang tipikal, bergantung pada pengoptimuman parameter dan kecairan, sesuai untuk pedagang yang menjejaki arah aliran. Ia boleh dijadikan rangka rujukan untuk pengembangan modul mengikut keperluan sebenar, dan risiko dapat dikurangkan serta kestabilan ditingkatkan melalui mekanisme seperti stop loss, take profit, dan penapisan isyarat.

- 1