Strategi Kawalan Keseimbangan Psikologi Perdagangan

Gambaran Keseluruhan

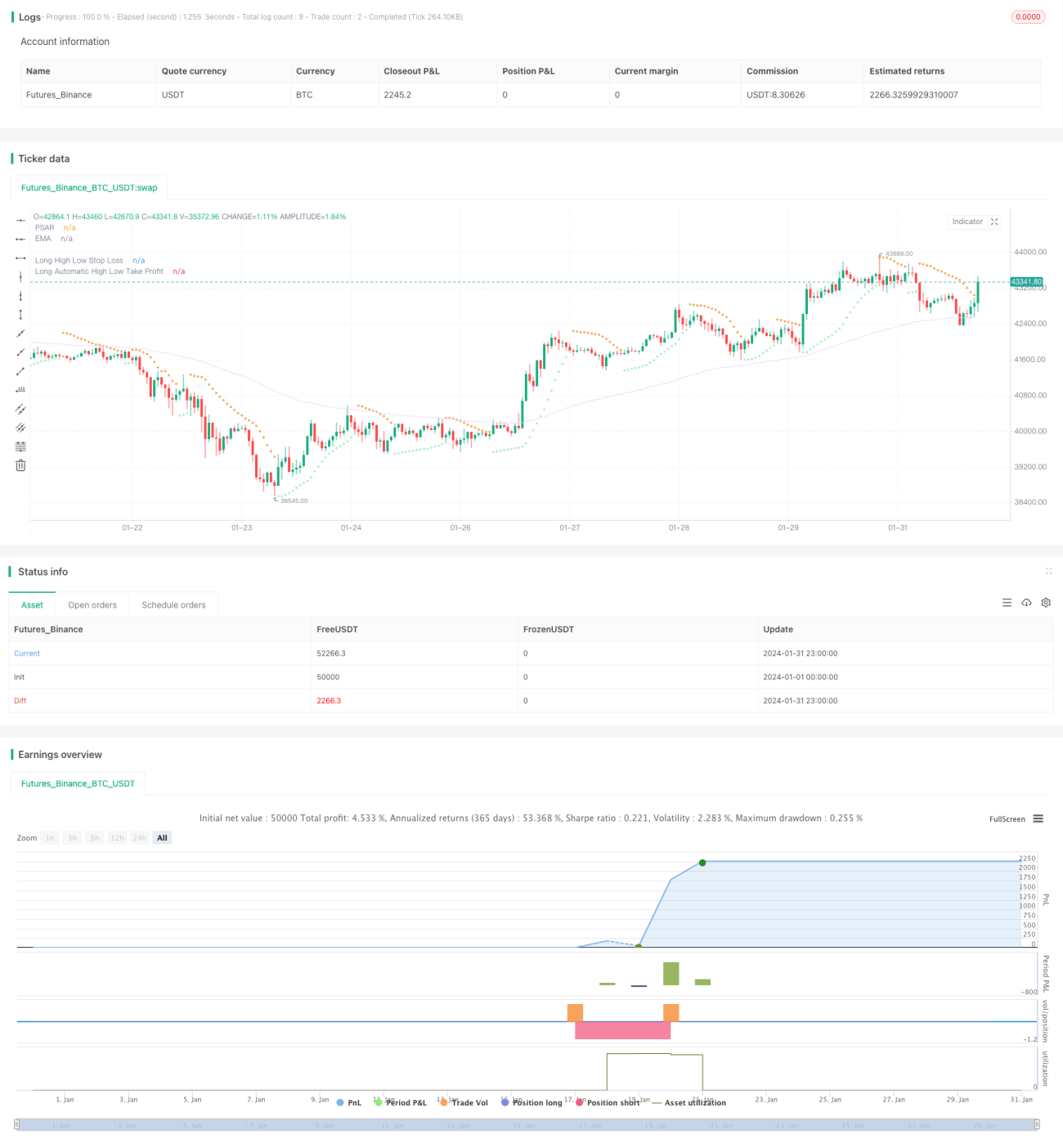

Strategi ini bertujuan untuk mengimbangi psikologi pedagang dan prestasi dagangan dengan menetapkan parameter yang berbeza bagi mendapatkan pulangan yang lebih stabil. Ia menggunakan penunjuk seperti purata bergerak, Bollinger Bands, Keltner Channels untuk menilai arah aliran pasaran dan turun naik, menggabungkan penunjuk PSAR untuk mengesan isyarat pembalikan, dan menggunakan penunjuk TTM Squeeze untuk menilai momentum. Isyarat dagangan dihasilkan daripada gabungan penunjuk ini. Pada masa yang sama, strategi ini menguruskan risiko dengan menggunakan stop loss pada paras tinggi/rendah dan take profit berdasarkan nisbah risiko-ganjaran.

Prinsip Strategi

Logik utama strategi ini adalah seperti berikut:

-

Menentukan arah aliran: Menggunakan EMA (Purata Bergerak Eksponen) untuk menilai arah harga. Harga di atas EMA menunjukkan arah menaik, di bawah EMA menunjukkan arah menurun.

-

Mengesan pembalikan: Menggunakan PSAR untuk mengesan titik pembalikan harga. Titik PSAR yang muncul di atas harga adalah isyarat kenaikan, manakala di bawah harga adalah isyarat penurunan.

-

Menilai momentum: Menggunakan penunjuk TTM Squeeze untuk mengukur turun naik dan momentum pasaran. Penunjuk TTM Squeeze membandingkan lebar Bollinger Bands dan Keltner Channels untuk mengukur turun naik. Squeeze (picitan) bermaksud turun naik yang sangat rendah. Pelepasan squeeze menandakan peningkatan turun naik dan pergerakan harga yang signifikan.

-

Menghasilkan isyarat dagangan: Apabila harga menembusi ke atas EMA dan titik PSAR, serta penunjuk TTM Squeeze melepaskan squeeze, isyarat beli (bullish) dihasilkan. Apabila harga menembusi ke bawah EMA dan titik PSAR, serta penunjuk TTM Squeeze memasuki squeeze, isyarat jual (bearish) dihasilkan.

-

Kaedah stop loss: Menggunakan stop loss pada paras tinggi/rendah. Titik stop loss ditentukan berdasarkan harga tertinggi atau terendah dalam tempoh tertentu yang didarab dengan gandaan yang ditetapkan.

-

Kaedah take profit: Menggunakan take profit automatik berdasarkan nisbah risiko-ganjaran. Titik take profit ditentukan berdasarkan jarak stop loss dari harga semasa didarab dengan parameter nisbah risiko-ganjaran yang ditetapkan.

Melalui penetapan parameter, kekerapan dagangan, pengurusan saiz posisi, titik stop loss dan take profit dapat dikawal bagi mengimbangi psikologi dagangan.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

-

Penilaian pelbagai penunjuk – meningkatkan ketepatan isyarat.

-

Mengutamakan pembalikan, disokong oleh arah aliran – menangkap titik pembalikan, mengurangkan kebarangkalian mengejar kenaikan dan menjual rendah.

-

Penunjuk TTM Squeeze – berkesan mengesan pelarasan dalam arah aliran, mengelakkan dagangan tidak berkesan semasa fasa pelarasan.

-

Stop loss paras tinggi/rendah – mudah dan praktikal, boleh dilaraskan mengikut pasaran.

-

Take profit berdasarkan nisbah risiko-ganjaran – mengkuantitikan hubungan untung/rugi, memudahkan pelarasan.

-

Parameter yang fleksibel – boleh ditala mengikut toleransi risiko individu.

Analisis Risiko

Strategi ini juga mempunyai risiko berikut:

-

Gabungan pelbagai penunjuk – walaupun meningkatkan ketepatan isyarat, ia juga meningkatkan kemungkinan terlepas titik masuk.

-

Strategi yang mengutamakan pembalikan – mungkin tidak berprestasi baik dalam pasaran yang sedang dalam arah aliran kuat.

-

Stop loss paras tinggi/rendah – kadangkala boleh ditembusi, tidak dapat mengelakkan risiko sepenuhnya.

-

Take profit berdasarkan nisbah risiko-ganjaran – mungkin gagal disebabkan lompatan harga atau pelarasan.

-

Parameter yang tidak sesuai – boleh menyebabkan kerugian atau henti rugi yang kerap.

Hala Tuju Pengoptimuman

Strategi ini boleh dioptimumkan dari aspek berikut:

-

Menambah atau melaraskan pemberat penunjuk – untuk isyarat yang lebih tepat.

-

Mengoptimumkan parameter penunjuk pembalikan dan arah aliran – meningkatkan kebarangkalian keuntungan.

-

Mengoptimumkan parameter stop loss paras tinggi/rendah – menjadikan stop loss lebih munasabah.

-

Menguji pelbagai nisbah risiko-ganjaran – untuk mendapatkan hasil yang optimum.

-

Melaraskan bilangan posisi – mengurangkan kesan kerugian tunggal.

Kesimpulan

Secara keseluruhan, strategi ini, melalui penilaian gabungan penunjuk dan pelarasan parameter, mampu mengimbangkan psikologi dagangan dan memperoleh pulangan positif yang stabil. Walaupun masih ada ruang untuk penambahbaikan, ia sudah bernilai untuk aplikasi dagangan sebenar. Dengan maklum balas pasaran dan penalaan parameter halus, strategi ini berpotensi menjadi alat yang berkesan untuk mengawal psikologi dagangan dan mencapai keuntungan stabil jangka panjang.

- 1