Strategi Gabungan Purata Pergerakan Trend Rekursif dengan Pembalikan Bentuk 123

Gambaran Keseluruhan

Strategi ini menggabungkan dua strategi iaitu Purata Pergerakan Trend Berulang dan Pembalikan Pola 123 untuk membentuk isyarat komprehensif, bertujuan meningkatkan kestabilan dan keuntungan strategi.

Prinsip

Pembalikan Pola 123

Bahagian ini mengambil inspirasi daripada buku Ulf Jensen "How I Tripled My Money in the Futures Market". Isyarat beli: harga penutupan dua hari terakhir meningkat dan nilai STO SLOWK kitaran 9 hari berada di bawah 50, maka posisi beli dibuka. Isyarat jual: harga penutupan dua hari terakhir menurun dan nilai STO FASTK kitaran 9 hari berada di atas 50, maka posisi jual dibuka.

Purata Pergerakan Trend Berulang

Bahagian ini menggunakan teknik yang dipanggil "Pelinieran Polinomial Berulang". Ideanya adalah menggunakan harga beberapa hari lalu dan harga hari semasa untuk meramalkan harga hari seterusnya. Apabila harga ramalan lebih tinggi daripada harga sebenar semalam, ia menandakan pandangan menurun, dan sebaliknya menaik.

Kelebihan

Gabungan strategi ini dapat memanfaatkan kelebihan kedua-dua strategi dan mengelakkan batasan strategi tunggal. Pembalikan Pola 123 dapat menangkap pergerakan besar ketika harga berbalik, manakala Purata Pergerakan Trend Berulang dapat menilai arah pergerakan harga dengan lebih tepat. Gabungan keduanya menghasilkan isyarat komprehensif yang kuat.

Risiko dan Penyelesaian

- Pembalikan Pola 123 mungkin menghasilkan isyarat palsu akibat turun naik harga jangka pendek. Parameter boleh disesuaikan untuk menapis hingar.

- Purata Pergerakan Trend Berulang mungkin lambat bertindak balas terhadap peristiwa mengejut. Boleh dipertimbangkan untuk menggabungkan dengan penunjuk lain untuk menilai trend tempatan.

- Isyarat kedua-dua strategi mungkin tidak selaras. Dalam kes ini, posisi hanya boleh dibuka apabila kedua-dua isyarat hadir, atau ikut hanya satu isyarat berdasarkan keadaan pasaran.

Hala Tuju Pengoptimuman

- Ujian pelbagai kombinasi parameter kitaran untuk mencari pasangan parameter terbaik.

- Memperkenalkan mekanisme henti rugi automatik.

- Menyesuaikan parameter berdasarkan instrumen dan keadaan pasaran yang berbeza.

- Boleh dipertimbangkan untuk digabungkan dengan strategi atau penunjuk lain bagi membentuk sistem komprehensif yang lebih kukuh.

Kesimpulan

Strategi ini menggabungkan dua jenis strategi yang berbeza untuk meningkatkan kestabilan melalui isyarat komprehensif. Dengan memanfaatkan kelebihan kedua-duanya, ia dapat menangkap titik pembalikan harga dan menilai arah pergerakan harga pada masa hadapan. Dengan pengoptimuman lanjut, ia berpotensi menunjukkan prestasi yang lebih cemerlang.

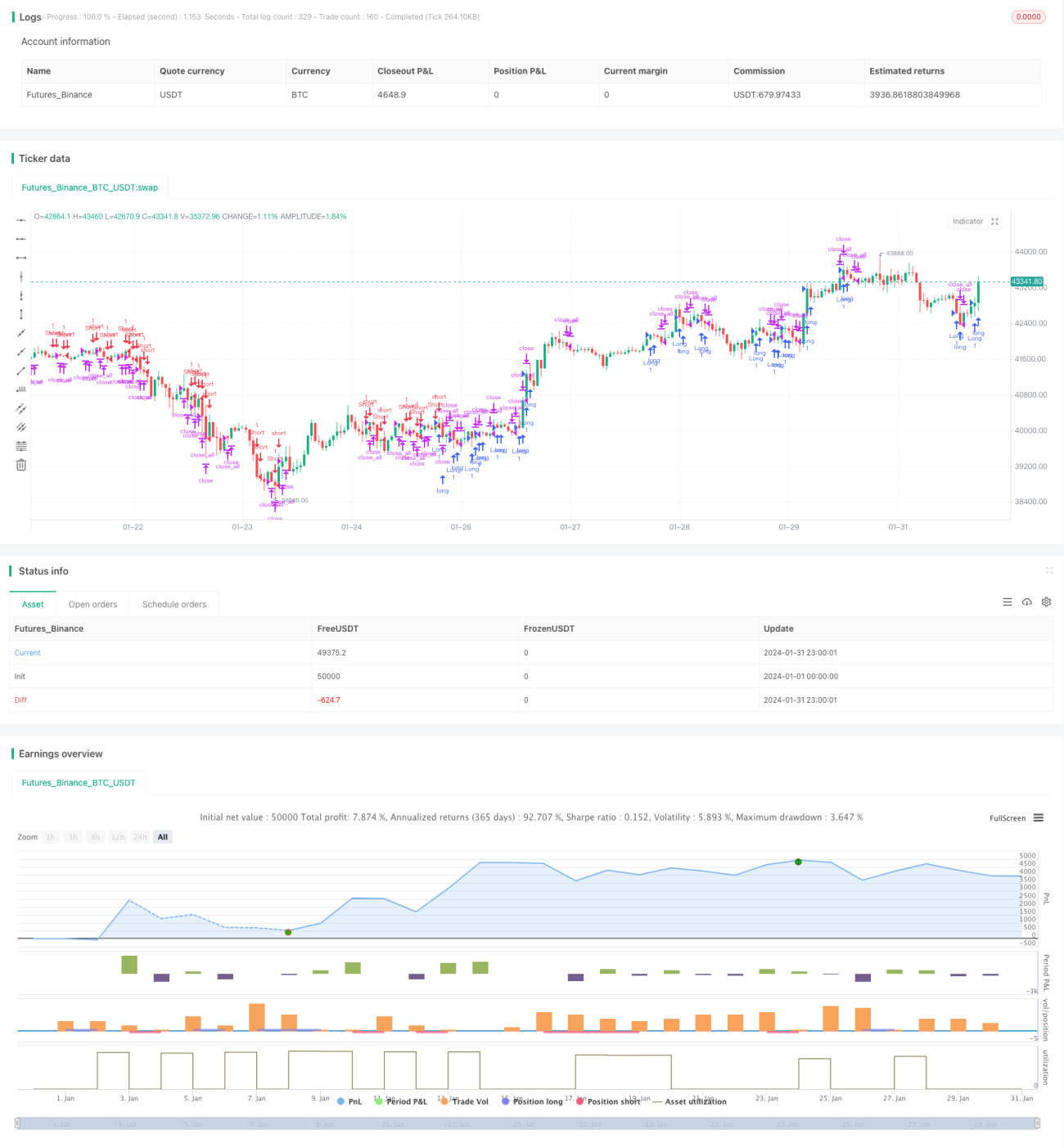

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 01/06/2021

// This is combo strategies for get a cumulative signal. - 1