RSI dan corak kenaikan harga strategi RSI yang lancar

Gambaran keseluruhan

Strategi ini mencari peluang untuk membeli pada titik rendah harga dengan menggabungkan RSI dengan RSI yang rata. Apabila RSI berinovasi rendah dan harga tidak berinovasi rendah, ia dianggap sebagai isyarat pemisahan multi-kepala.

Prinsip Strategi

- Hitung RSI dengan parameter 14 hari.

- Hitung RSI yang rata untuk mencapai kesan yang rata melalui purata WMA ganda.

- Jika RSI anda lebih rendah daripada 30, anda telah menjual lebih banyak daripada yang sepatutnya.

- Menentukan sama ada RSI lancar di bawah 35 atau lebih baik.

- Menentukan apakah RSI berada di bawah 25.

- Mengira RSI secara berspesifik, iaitu mencari RSI yang berinovasi rendah dan harga tidak berinovasi rendah.

- Untuk mengira kitaran penurunan RSI yang lancar, ia memerlukan 3 hari.

- Apabila syarat-syarat di atas dipenuhi, ia akan menghasilkan isyarat beli.

- Tetapkan keadaan berhenti dan hentikan.

Strategi ini bergantung kepada sifat pembalikan RSI, digabungkan dengan trend penghakiman RSI yang merata, membeli ketika harga berada di bawah tekanan dan RSI oversold.

Analisis kelebihan strategi

- Kombinasi RSI Ganda untuk Meningkatkan Kesan Strategi.

- Dengan menggunakan ciri-ciri pembalikan RSI, terdapat kelebihan kebarangkalian tertentu.

- RSI yang rata membantu mengelakkan pembalikan palsu.

- Logik stop-loss yang lengkap untuk mengurangkan risiko.

Analisis risiko

- Kemungkinan RSI berbalik gagal tidak dapat dielakkan sepenuhnya.

- Indeks RSI yang rata terlewat, mungkin terlepas peluang terbaik untuk membeli.

- Penetapan stop loss terlalu longgar, risiko peningkatan kerugian.

Anda boleh mengoptimumkan masa pembelian dengan menyesuaikan parameter RSI. Anda boleh mengurangkan jarak henti dengan sewajarnya dan mempercepatkan laju henti. Anda boleh menggunakan indikator lain untuk menilai risiko trend dan mengurangkan kemungkinan pembalikan palsu.

Arah pengoptimuman

- Anda boleh menguji kesan RSI dengan parameter yang berbeza.

- Mengoptimumkan kaedah pengiraan RSI yang halus, meningkatkan kualiti yang halus.

- Menyesuaikan titik hentian dan hentian untuk mencari nisbah ganjaran risiko yang optimum.

- Meningkatkan penilaian seperti penunjuk kapasiti, mengelakkan kekurangan kapasiti.

Dengan menyesuaikan parameter dan menggabungkan lebih banyak petunjuk, anda boleh meningkatkan lagi keberkesanan perdagangan strategi.

ringkaskan

Keseluruhan strategi ini adalah strategi yang memanfaatkan ciri-ciri RSI yang berbalik. Kombinasi kedua-dua indikator RSI memanfaatkan sepenuhnya kesan pembalikan RSI, tetapi juga meningkatkan ketidakpastian yang disebabkan oleh perbezaan indikator. Keseluruhan adalah strategi strategi indikator yang tipikal.

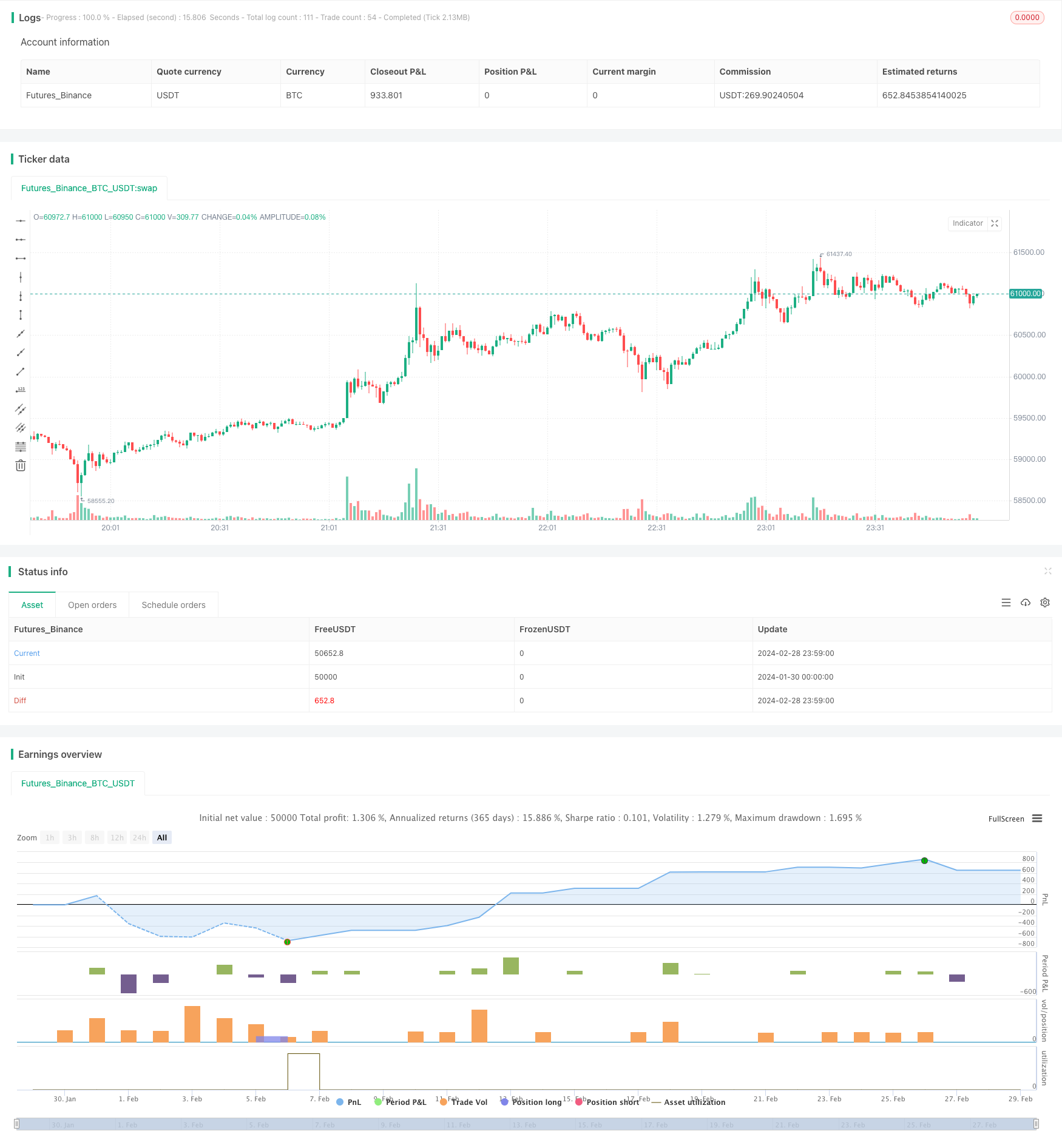

/*backtest

start: 2024-01-30 00:00:00

end: 2024-02-29 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © BigBitsIO

//@version=4

strategy(title="RSI and Smoothed RSI Bull Div Strategy [BigBitsIO]", shorttitle="RSI and Smoothed RSI Bull Div Strategy [BigBitsIO]", overlay=true, pyramiding=1, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_type=strategy.commission.percent, commission_value=.1, slippage=0)

TakeProfitPercent = input(3, title="Take Profit %", type=input.float, step=.25)

StopLossPercent = input(1.75, title="Stop Loss %", type=input.float, step=.25)

RSICurve = input(14, title="RSI Lookback Period", type=input.integer, step=1)

BuyBelowTargetPercent = input(0, title="Buy Below Lowest Low In RSI Divergence Lookback Target %", type=input.float, step=.05)

BuyBelowTargetSource = input(close, title="Source of Buy Below Target Price", type=input.source)

SRSICurve = input(10, title="Smoothed RSI Lookback Period", type=input.integer, step=1)

RSICurrentlyBelow = input(30, title="RSI Currently Below", type=input.integer, step=1)

RSIDivergenceLookback = input(25, title="RSI Divergence Lookback Period", type=input.integer, step=1)

RSILowestInDivergenceLookbackCurrentlyBelow = input(25, title="RSI Lowest In Divergence Lookback Currently Below", type=input.integer, step=1)

RSISellAbove = input(65, title="RSI Sell Above", type=input.integer, step=1)

MinimumSRSIDownTrend = input(3, title="Minimum SRSI Downtrend Length", type=input.integer, step=1)

SRSICurrentlyBelow = input(35, title="Smoothed RSI Currently Below", type=input.integer, step=1)

PlotTarget = input(false, title="Plot Target")

RSI = rsi(close, RSICurve)

SRSI = wma(2*wma(RSI, SRSICurve/2)-wma(RSI, SRSICurve), round(sqrt(SRSICurve))) // Hull moving average

SRSITrendDownLength = 0

if (SRSI < SRSI[1])

SRSITrendDownLength := SRSITrendDownLength[1] + 1

// Strategy Specific

ProfitTarget = (close * (TakeProfitPercent / 100)) / syminfo.mintick

LossTarget = (close * (StopLossPercent / 100)) / syminfo.mintick

BuyBelowTarget = BuyBelowTargetSource[(lowestbars(RSI, RSIDivergenceLookback)*-1)] - (BuyBelowTargetSource[(lowestbars(RSI, RSIDivergenceLookback)*-1)] * (BuyBelowTargetPercent / 100))

plot(PlotTarget ? BuyBelowTarget : na)

bool IsABuy = RSI < RSICurrentlyBelow and SRSI < SRSICurrentlyBelow and lowest(SRSI, RSIDivergenceLookback) < RSILowestInDivergenceLookbackCurrentlyBelow and BuyBelowTargetSource < BuyBelowTarget and SRSITrendDownLength >= MinimumSRSIDownTrend and RSI > lowest(RSI, RSIDivergenceLookback)

bool IsASell = RSI > RSISellAbove

if IsABuy

strategy.entry("Positive Trend", true) // buy by market

strategy.exit("Take Profit or Stop Loss", "Positive Trend", profit = ProfitTarget, loss = LossTarget)

if IsASell

strategy.close("Positive Trend")