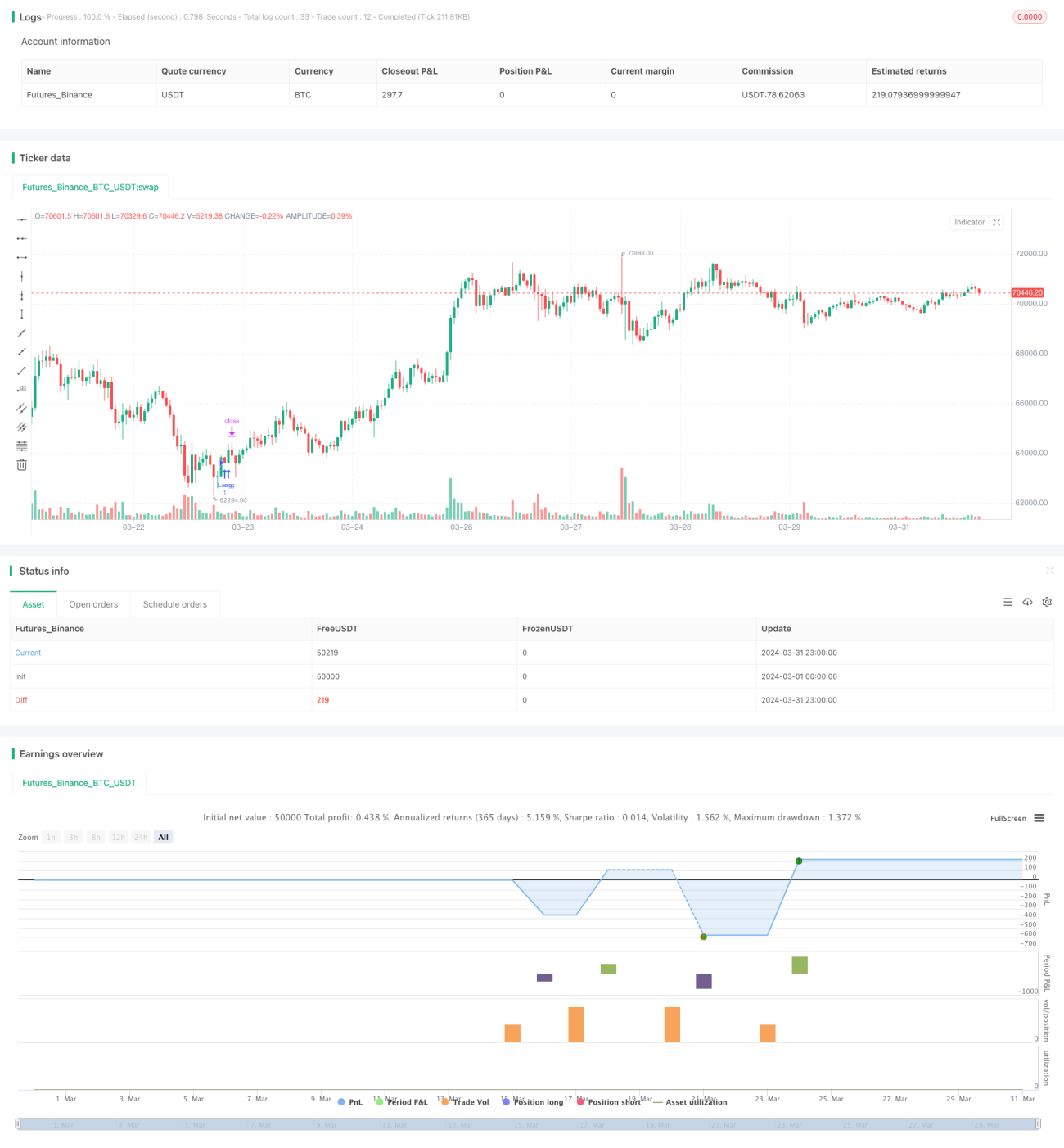

Strategi Dagangan BTC Berbilang Penunjuk

Gambaran Keseluruhan

Strategi ini menggabungkan beberapa penunjuk teknikal, termasuk Indeks Kekuatan Relatif (RSI), MACD (Moving Average Convergence Divergence), dan beberapa Purata Bergerak Mudah (SMA) dengan tempoh yang berbeza, bertujuan untuk menyediakan alat analisis yang komprehensif untuk perdagangan Bitcoin (BTC). Idea utama strategi ini adalah dengan mempertimbangkan isyarat daripada pelbagai penunjuk secara bersepadu, memasuki posisi beli apabila RSI berada dalam julat tertentu, MACD menunjukkan persilangan emas (golden cross), dan harga berada di bawah beberapa SMA, sambil menetapkan henti rugi (stop loss) dan ambil untung (take profit). Selain itu, kedudukan henti rugi akan dikemas kini apabila RSI mencapai 50.

Prinsip Strategi

- Kira RSI, MACD, dan SMA untuk tempoh yang berbeza.

- Nilai sama ada nilai RSI sebelumnya lebih rendah daripada had bawah atau lebih tinggi daripada had atas, sama ada nilai RSI semasa berada di antara had bawah dan had atas, sama ada MACD menunjukkan persilangan emas, dan sama ada harga penutup lebih rendah daripada semua SMA.

- Jika syarat di atas dipenuhi dan tiada kedudukan semasa, buka posisi beli (long).

- Tetapkan harga henti rugi dan ambil untung berdasarkan peratusan risiko.

- Jika memegang posisi beli dan RSI mencapai 50, kemas kini kedudukan henti rugi kepada harga tertinggi.

- Jika MACD menunjukkan persilangan mati (death cross), tutup posisi.

Kelebihan Strategi

- Menggabungkan pelbagai penunjuk teknikal untuk meningkatkan kebolehpercayaan isyarat.

- Membuka posisi hanya apabila RSI berada dalam julat tertentu, mengelakkan kemasukan dalam keadaan ekstrem.

- Menetapkan henti rugi dan ambil untung untuk mengawal risiko.

- Melaraskan kedudukan henti rugi secara dinamik untuk mengunci sebahagian keuntungan.

- Menutup posisi tepat pada masanya berdasarkan isyarat persilangan mati MACD, mengurangkan potensi kerugian.

Risiko Strategi

- Dalam pasaran yang berombak (sideways), isyarat dagangan yang kerap boleh menyebabkan terlalu banyak urus niaga dan kerugian komisen.

- Henti rugi dan ambil untung berdasarkan peratusan risiko tetap mungkin tidak sesuai untuk persekitaran pasaran yang berbeza.

- Hanya bergantung pada penunjuk teknikal tanpa mengambil kira faktor asas boleh menyebabkan keputusan dagangan yang salah.

Arah Pengoptimuman Strategi

- Memperkenalkan lebih banyak penunjuk teknikal atau penunjuk sentimen pasaran untuk meningkatkan ketepatan isyarat.

- Melaraskan tahap henti rugi dan ambil untung secara dinamik berdasarkan turun naik pasaran untuk menyesuaikan diri dengan persekitaran pasaran yang berbeza.

- Menggabungkan analisis asas, seperti peristiwa berita besar atau perubahan dasar kawal selia, untuk membantu keputusan dagangan.

- Pertimbangkan penunjuk pada jangka masa yang berbeza untuk menangkap peluang dagangan pada pelbagai skala masa.

Kesimpulan

Strategi ini menyediakan rangka kerja analisis yang komprehensif untuk perdagangan Bitcoin dengan menggunakan penunjuk teknikal seperti RSI, MACD, dan SMA. Ia menjana isyarat dagangan melalui pengesahan bersama daripada pelbagai penunjuk dan melaksanakan langkah kawalan risiko. Walau bagaimanapun, masih ada ruang untuk pengoptimuman, seperti memperkenalkan lebih banyak penunjuk, melaraskan parameter secara dinamik, dan menggabungkan analisis asas. Dalam aplikasi praktikal, peniaga harus menyesuaikan strategi mengikut toleransi risiko dan persekitaran pasaran masing-masing.

- 1