Gambaran Keseluruhan

Strategi ini menggunakan beberapa purata bergerak (VWMA), Indeks Arah Purata (ADX) dan Indeks Pergerakan Arah (DMI) untuk menangkap peluang beli dalam pasaran Bitcoin. Dengan menggabungkan momentum harga, arah aliran, dan jumlah dagangan, strategi ini bertujuan mencari titik masuk yang mempunyai arah menaik yang kukuh dan momentum mencukupi, sambil mengawal risiko dengan ketat.

Prinsip Strategi

- Menggunakan VWMA 9 hari dan 14 hari untuk menilai arah menaik – isyarat beli dijana apabila purata bergerak jangka pendek melintasi ke atas purata bergerak jangka panjang.

- Memperkenalkan purata bergerak suai yang dibina daripada VWMA harga tertinggi dan terendah 89 hari sebagai penapis arah aliran – posisi hanya dipertimbangkan apabila harga tutup atau harga buka berada di atas purata tersebut.

- Menggunakan indikator ADX dan DMI untuk mengesahkan kekuatan arah aliran – hanya apabila ADX >18 dan perbezaan antara +DI dan -DI >15, arah aliran dianggap cukup kuat.

- Menggunakan fungsi persentil jumlah dagangan untuk menapis palang yang jumlah dagangannya berada dalam julat 60%–95%, mengelakkan tempoh jumlah dagangan yang terlalu rendah.

- Menetapkan henti rugi pada 0.96–0.99 kali ganda harga tertinggi palang sebelumnya, dan semakin berkurang dengan peningkatan jangka masa, bagi mengawal risiko.

- Tutup posisi apabila tempoh pegangan yang ditetapkan tercapai atau harga jatuh di bawah purata bergerak suai.

Analisis Kelebihan

- Menggabungkan beberapa indikator teknikal untuk menilai keadaan pasaran dari pelbagai dimensi seperti arah aliran, momentum, dan jumlah dagangan, menjadikan isyarat lebih boleh dipercayai.

- Purata bergerak suai dan mekanisme penapisan jumlah dagangan berkesan menapis isyarat palsu, mengurangkan dagangan tidak berkesan.

- Tetapan henti rugi yang ketat dan had tempoh pegangan mengurangkan dedahan risiko strategi dengan ketara.

- Reka bentuk modular kod memudahkan pembacaan dan penyelenggaraan, serta memudahkan pengoptimuman dan pengembangan selanjutnya.

Analisis Risiko

- Apabila pasaran berada dalam fasa sideways atau arah aliran yang tidak jelas, strategi ini mungkin menjana banyak isyarat palsu.

- Tahap henti rugi agak dekat, yang boleh menyebabkan henti rugi tercetus terlalu awal semasa pergerakan pasaran yang besar, menyebabkan kerugian lebih besar.

- Kurang pertimbangan terhadap keadaan ekonomi makro dan peristiwa besar, menjadikannya mungkin gagal apabila berdepan peristiwa 'angsa hitam'.

- Tetapan parameter agak tetap dan kurang kebolehsuaian, prestasi mungkin tidak stabil dalam persekitaran pasaran yang berbeza.

Hala Tuju Pengoptimuman

- Memperkenalkan lebih banyak indikator yang boleh menggambarkan keadaan pasaran, seperti Indeks Kekuatan Relatif (RSI), Bollinger Bands, dan lain-lain, untuk meningkatkan kebolehpercayaan isyarat.

- Mengoptimumkan tahap henti rugi secara dinamik, contohnya menggunakan ATR atau henti rugi peratusan, untuk menyesuaikan dengan keadaan turun naik pasaran yang berbeza.

- Menggabungkan data ekonomi makro dan analisis sentimen untuk memperkukuh modul kawalan risiko strategi.

- Menggunakan algoritma pembelajaran mesin untuk mengoptimumkan parameter secara automatik, meningkatkan kebolehsuaian dan kestabilan strategi.

Kesimpulan

Strategi beli Bitcoin VWMA-ADX menggabungkan beberapa indikator teknikal seperti arah aliran harga, momentum dan jumlah dagangan, membolehkannya menangkap peluang kenaikan dalam pasaran Bitcoin dengan agak berkesan. Pada masa yang sama, langkah kawalan risiko yang ketat dan syarat tutup posisi yang jelas membolehkan risiko strategi dikawal dengan baik. Walau bagaimanapun, strategi ini juga mempunyai beberapa kelemahan, seperti kurang kebolehsuaian terhadap perubahan persekitaran pasaran, serta strategi henti rugi yang perlu dioptimumkan lagi. Pada masa hadapan, peningkatan boleh dibuat dari segi kebolehpercayaan isyarat, kawalan risiko, dan pengoptimuman parameter untuk meningkatkan lagi kestabilan dan keuntungan strategi. Secara keseluruhannya, strategi beli Bitcoin VWMA-ADX menyediakan pendekatan dagangan sistematik berasaskan momentum dan arah aliran kepada pelabur, yang wajar diterokai dan diperbaiki lagi.

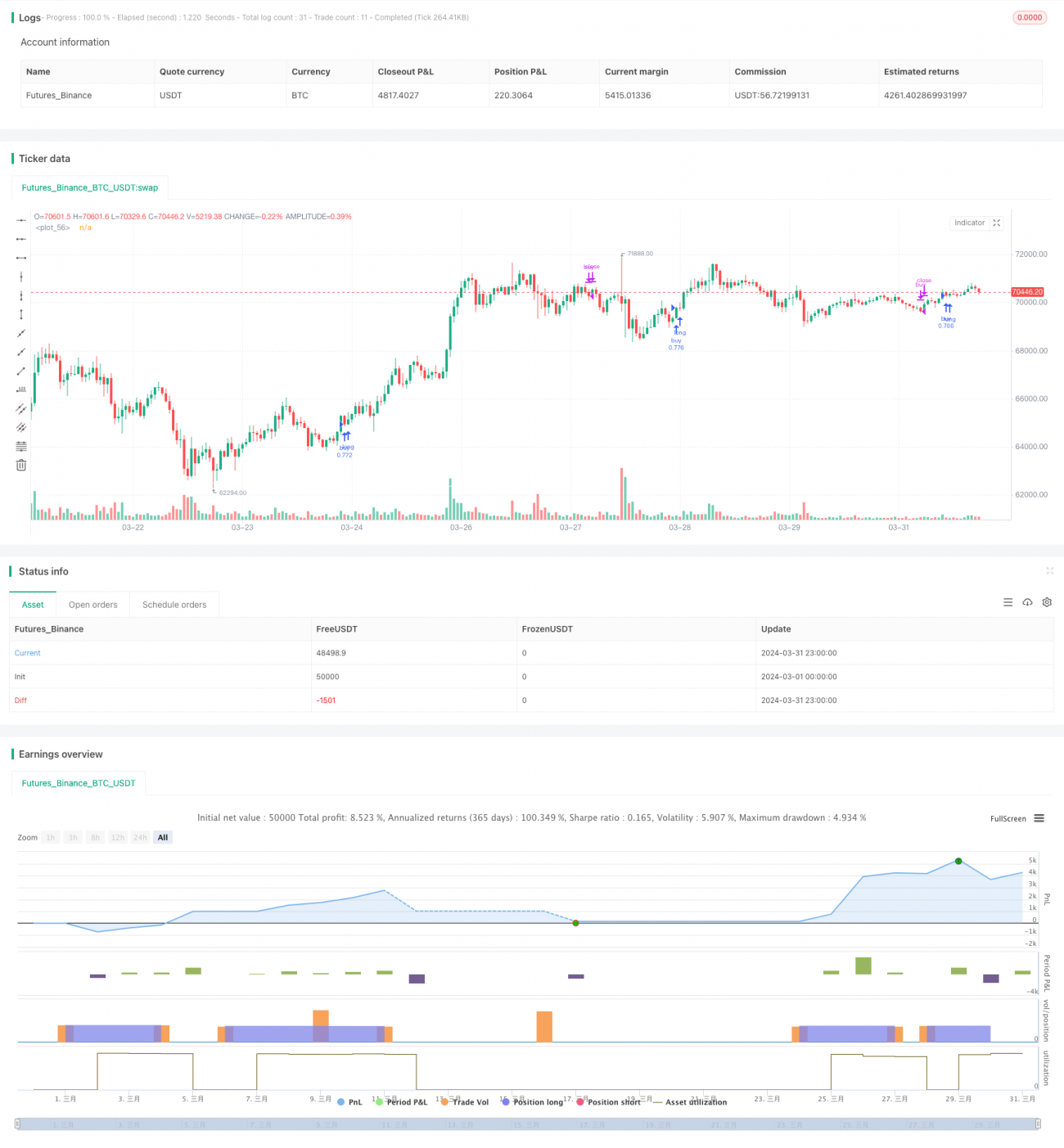

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Q_D_Nam_N_96

//@version=5

- 1