Mampatan Ujian Balik Transformer v2.0

Gambaran Umum

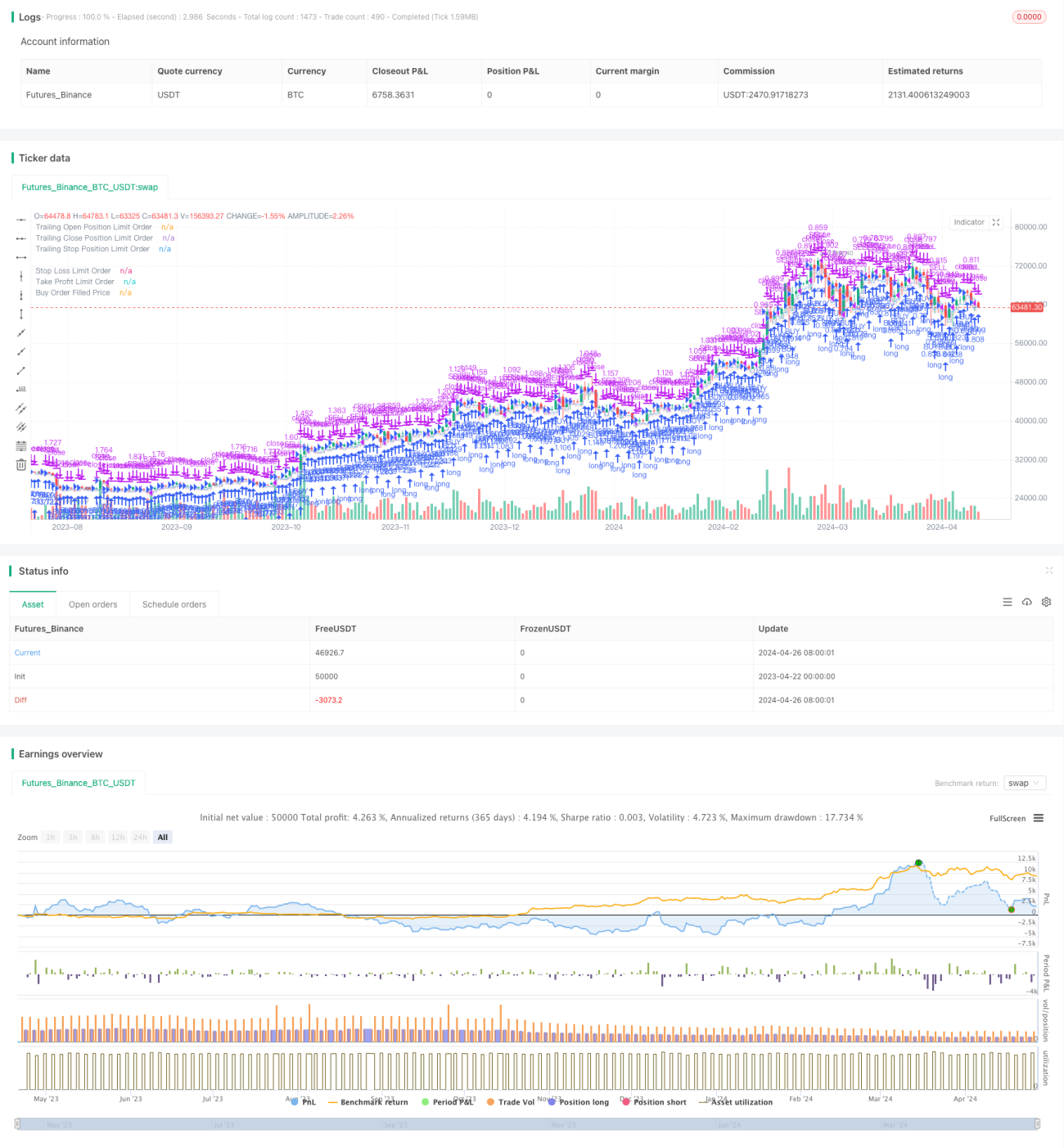

Squeeze Backtest Transformer v2.0 ialah sistem perdagangan kuantitatif berdasarkan strategi jenis squeeze. Ia menjalankan ujian belakang ke atas strategi dalam jangka masa tertentu dengan menetapkan parameter seperti peratusan masuk, henti rugi dan ambil untung, serta tempoh pegangan maksimum. Strategi ini menyokong perdagangan pelbagai arah, dan boleh menetapkan arah perdagangan secara fleksibel sama ada beli panjang atau jual pendek. Pada masa yang sama, strategi ini juga menyediakan pilihan tempoh ujian belakang yang pelbagai, memudahkan pemilihan jangka masa tetap atau masa ujian belakang maksimum.

Prinsip Strategi

- Pertama, berdasarkan parameter tempoh ujian belakang yang ditetapkan oleh pengguna, tentukan masa mula dan masa tamat ujian belakang.

- Dalam tempoh ujian belakang, jika tiada pegangan semasa dan harga menyentuh harga masuk (dikira berdasarkan peratusan buka posisi), maka buka posisi dan pada masa yang sama tetapkan harga henti rugi dan ambil untung (dikira berdasarkan peratusan henti rugi dan ambil untung).

- Jika sudah mempunyai pegangan, batalkan pesanan henti rugi/ambil untung sebelumnya dan tetapkan semula harga henti rugi/ambil untung baharu (dikira berdasarkan harga purata pegangan semasa).

- Jika tempoh pegangan maksimum ditetapkan, apabila tempoh pegangan mencapai nilai maksimum, posisi akan ditutup secara paksa.

- Strategi menyokong perdagangan dalam dua arah: beli panjang dan jual pendek.

Kelebihan Strategi

- Tetapan parameter yang fleksibel, boleh disesuaikan mengikut keadaan pasaran dan keperluan perdagangan yang berbeza.

- Menyokong perdagangan pelbagai arah, boleh menjana keuntungan dalam pelbagai keadaan pasaran.

- Menyediakan pilihan tempoh ujian belakang yang pelbagai, memudahkan ujian belakang dan analisis data sejarah.

- Tetapan henti rugi dan ambil untung dapat mengawal risiko dengan berkesan dan meningkatkan kecekapan penggunaan modal.

- Tetapan tempoh pegangan maksimum dapat mengelakkan risiko pasaran akibat pegangan yang terlalu lama.

Risiko Strategi

- Tetapan harga masuk, harga henti rugi dan harga ambil untung memberi kesan besar kepada pulangan strategi; tetapan parameter yang tidak sesuai boleh menyebabkan kerugian.

- Apabila pasaran turun naik dengan kuat, kemungkinan berlakunya situasi di mana posisi baru dibuka serta-merta mencetuskan henti rugi, mengakibatkan kerugian.

- Jika tempoh pegangan maksimum dicetuskan semasa pegangan, mungkin terlepas peluang keuntungan seterusnya.

- Prestasi strategi mungkin tidak baik dalam keadaan pasaran tertentu (seperti pasaran sideway).

Arah Pengoptimuman Strategi

- Boleh mempertimbangkan untuk memperkenalkan lebih banyak penunjuk teknikal atau penunjuk sentimen pasaran, mengoptimumkan syarat masuk, henti rugi dan ambil untung, meningkatkan kestabilan dan keuntungan strategi.

- Bagi tetapan tempoh pegangan maksimum, boleh melaraskan secara dinamik berdasarkan turun naik pasaran dan untung/rugi pegangan, mengelakkan kos peluang yang mungkin timbul daripada penutupan posisi pada masa tetap.

- Sebagai tindak balas kepada ciri pasaran sideway, boleh menambah logik seperti penembusan julat sideway atau pengesahan perubahan arah aliran, mengurangkan kos akibat perdagangan yang kerap.

- Pertimbangkan untuk menambah strategi pengurusan posisi dan pengurusan modal, mengawal pendedahan risiko setiap perdagangan, meningkatkan kecekapan penggunaan modal dan kestabilan.

Ringkasan

Squeeze Backtest Transformer v2.0 ialah sistem perdagangan kuantitatif berdasarkan strategi jenis squeeze. Melalui tetapan parameter yang fleksibel dan sokongan perdagangan pelbagai arah, ia boleh berdagang dalam pelbagai persekitaran pasaran. Pada masa yang sama, pilihan tempoh ujian belakang yang pelbagai dan tetapan henti rugi/ambil untung dapat membantu pengguna dalam analisis data sejarah dan kawalan risiko. Walau bagaimanapun, prestasi strategi sangat dipengaruhi oleh tetapan parameter, dan perlu dioptimumkan serta diperbaiki berdasarkan ciri pasaran dan keperluan perdagangan untuk meningkatkan keteguhan dan keuntungan strategi. Pada masa hadapan, boleh mempertimbangkan untuk memperkenalkan lebih banyak penunjuk teknikal, melaraskan tempoh pegangan maksimum secara dinamik, mengoptimumkan strategi pasaran sideway, serta memperkukuh pengurusan posisi dan modal untuk pengoptimuman.

/*backtest

start: 2023-04-22 00:00:00

end: 2024-04-27 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="Squeeze Backtest by Shaqi v2.0", overlay=true, pyramiding=0, currency="USD", process_orders_on_close=true, commission_type=strategy.commission.percent, commission_value=0.075, default_qty_type=strategy.percent_of_equity, default_qty_value=100, initial_capital=100, backtest_fill_limits_assumption=0)

R0 = "6 Hours"- 1