Strategi Pengesanan Trend Berbilang Penunjuk

Gambaran Keseluruhan

Strategi ini dinamakan "Jancok Strategycs v3", merupakan strategi penjejakan arah aliran pelbagai penunjuk yang berdasarkan Purata Pergerakan (MA), Perbezaan Penumpuan Purata Pergerakan (MACD), Indeks Kekuatan Relatif (RSI) dan Julat Benar Purata (ATR). Idea utama strategi ini adalah menggunakan gabungan pelbagai penunjuk untuk menilai arah aliran pasaran dan membuat perdagangan mengikut arah aliran tersebut. Pada masa yang sama, strategi ini juga menggunakan kaedah henti rugi dan ambil untung dinamik, serta pengurusan risiko berdasarkan ATR, untuk mengawal risiko dan mengoptimumkan pulangan.

Prinsip Strategi

Strategi ini menggunakan empat penunjuk berikut untuk menilai arah aliran pasaran:

- Purata Pergerakan (MA): Mengira purata pergerakan jangka pendek (9 tempoh) dan jangka panjang (21 tempoh). Apabila purata pergerakan jangka pendek melintasi ke atas purata pergerakan jangka panjang, ini menunjukkan arah aliran menaik; apabila purata pergerakan jangka pendek melintasi ke bawah purata pergerakan jangka panjang, ini menunjukkan arah aliran menurun.

- Perbezaan Penumpuan Purata Pergerakan (MACD): Mengira garis MACD dan garis isyarat. Apabila garis MACD melintasi ke atas garis isyarat, ini menunjukkan arah aliran menaik; apabila garis MACD melintasi ke bawah garis isyarat, ini menunjukkan arah aliran menurun.

- Indeks Kekuatan Relatif (RSI): Mengira RSI 14 tempoh. Apabila RSI melebihi 70, pasaran mungkin terlebih beli; apabila RSI di bawah 30, pasaran mungkin terlebih jual.

- Julat Benar Purata (ATR): Mengira ATR 14 tempoh, digunakan untuk mengukur kemeruapan pasaran dan menetapkan titik henti rugi dan ambil untung.

Logik perdagangan strategi ini adalah seperti berikut:

- Apabila purata pergerakan jangka pendek melintasi ke atas purata pergerakan jangka panjang, garis MACD melintasi ke atas garis isyarat, jumlah dagangan lebih besar daripada purata pergerakannya, dan kemeruapan di bawah ambang, buka posisi beli (long).

- Apabila purata pergerakan jangka pendek melintasi ke bawah purata pergerakan jangka panjang, garis MACD melintasi ke bawah garis isyarat, jumlah dagangan lebih besar daripada purata pergerakannya, dan kemeruapan di bawah ambang, buka posisi jual (short).

- Titik henti rugi dan ambil untung ditetapkan secara dinamik berdasarkan ATR: henti rugi pada 2 kali ganda ATR, ambil untung pada 4 kali ganda ATR.

- Boleh memilih menggunakan henti rugi menjejak berdasarkan ATR, dengan titik henti rugi menjejak pada 2.5 kali ganda ATR.

Kelebihan Strategi

- Gabungan pelbagai penunjuk untuk menilai arah aliran, meningkatkan ketepatan penilaian arah aliran.

- Henti rugi dan ambil untung dinamik, menyesuaikan diri secara adaptif dengan kemeruapan pasaran, mengawal risiko dan mengoptimumkan pulangan dengan lebih baik.

- Memasukkan penapis jumlah dagangan dan kemeruapan, mengelakkan dagangan semasa kecairan rendah dan kemeruapan tinggi, mengurangkan isyarat palsu.

- Pilihan henti rugi menjejak, mengekalkan lebih banyak keuntungan semasa arah aliran berterusan.

Risiko Strategi

- Semasa pasaran berayun atau perubahan arah aliran, isyarat palsu mungkin berlaku, menyebabkan kerugian.

- Penetapan parameter memberi kesan besar terhadap prestasi strategi, memerlukan pengoptimuman mengikut pasaran dan aset yang berbeza.

- Pengoptimuman parameter yang berlebihan boleh menyebabkan overfitting, prestasi buruk dalam dagangan sebenar.

- Apabila berlaku turun naik pasaran yang tidak normal atau peristiwa angsa hitam, strategi mungkin menanggung kerugian besar.

Hala Tuju Pengoptimuman Strategi

- Memperkenalkan lebih banyak penunjuk seperti Bollinger Bands, Stochastic, dll., untuk meningkatkan lagi ketepatan penilaian arah aliran.

- Mengoptimumkan pemilihan parameter, seperti menggunakan algoritma genetik, carian grid, dsb., untuk mencari kombinasi parameter optimum.

- Menetapkan parameter dan peraturan berbeza untuk pasaran dan aset berbeza, meningkatkan kebolehsuaian strategi.

- Menambah pengurusan saiz posisi, melaraskan saiz posisi secara dinamik berdasarkan kekuatan arah aliran pasaran dan risiko akaun.

- Menetapkan had pengeluaran maksimum, menghentikan dagangan atau mengurangkan saiz posisi apabila akaun mencapai pengeluaran maksimum, mengawal risiko.

Ringkasan

"Jancok Strategycs v3" adalah strategi penjejakan arah aliran berdasarkan gabungan pelbagai penunjuk, yang menggunakan penunjuk seperti Purata Pergerakan, MACD, RSI dan ATR untuk menilai arah aliran pasaran, serta menggunakan alat pengurusan risiko seperti henti rugi/ambil untung dinamik dan henti rugi menjejak untuk mengawal risiko dan mengoptimumkan pulangan. Kelebihan strategi ini termasuk ketepatan penilaian arah aliran yang tinggi, pengurusan risiko yang fleksibel, dan kebolehsuaian yang baik. Walau bagaimanapun, terdapat juga risiko tertentu seperti isyarat palsu, kepekaan terhadap penetapan parameter, dan peristiwa angsa hitam. Pada masa hadapan, prestasi dan kestabilan strategi boleh dipertingkatkan lagi dengan memperkenalkan lebih banyak penunjuk, mengoptimumkan pemilihan parameter, menambah pengurusan saiz posisi, dan menetapkan had pengeluaran maksimum.

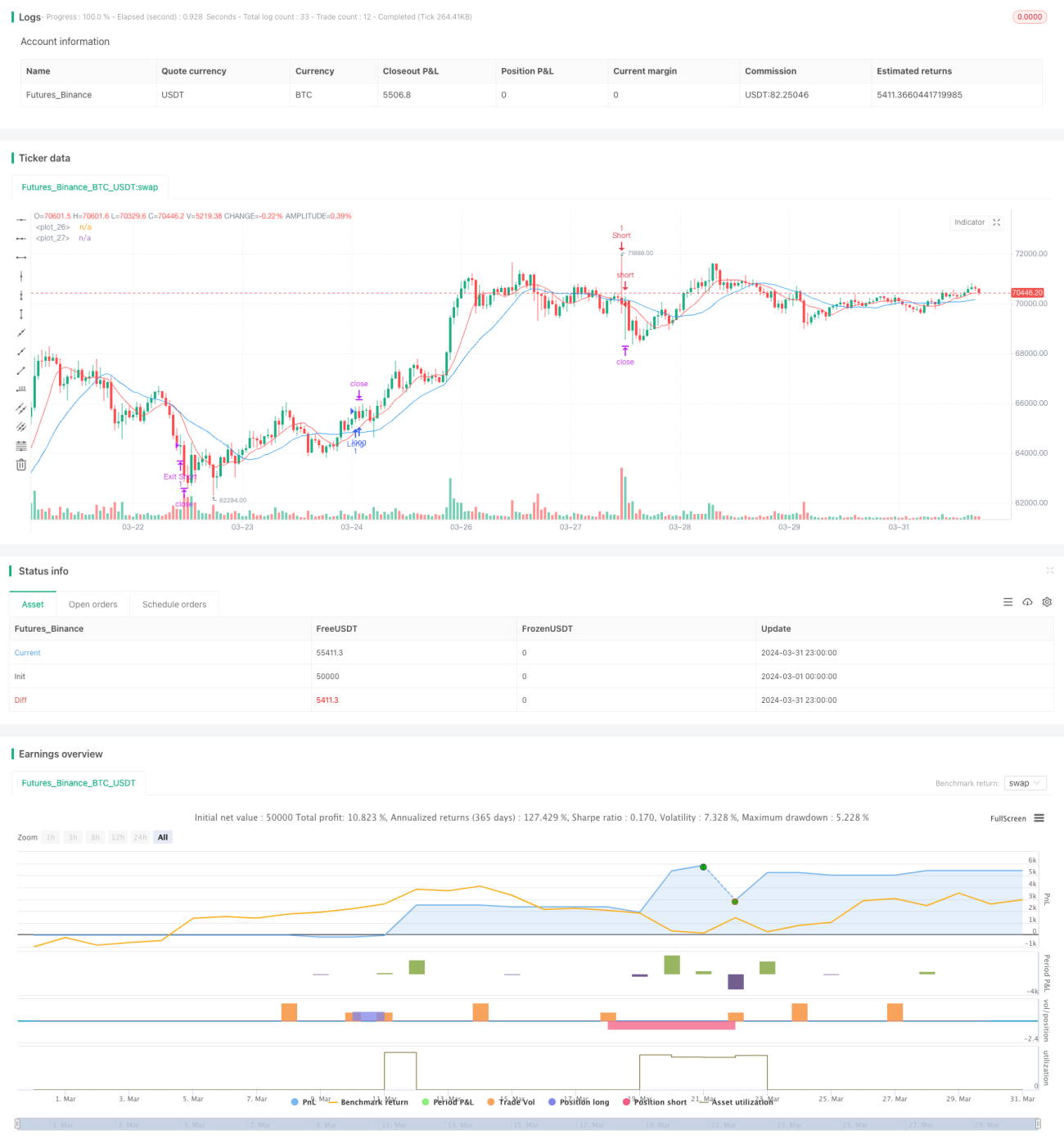

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © financialAccou42381

//@version=5- 1