Strategi Crossover VWAP dan RSI

Gambaran keseluruhan

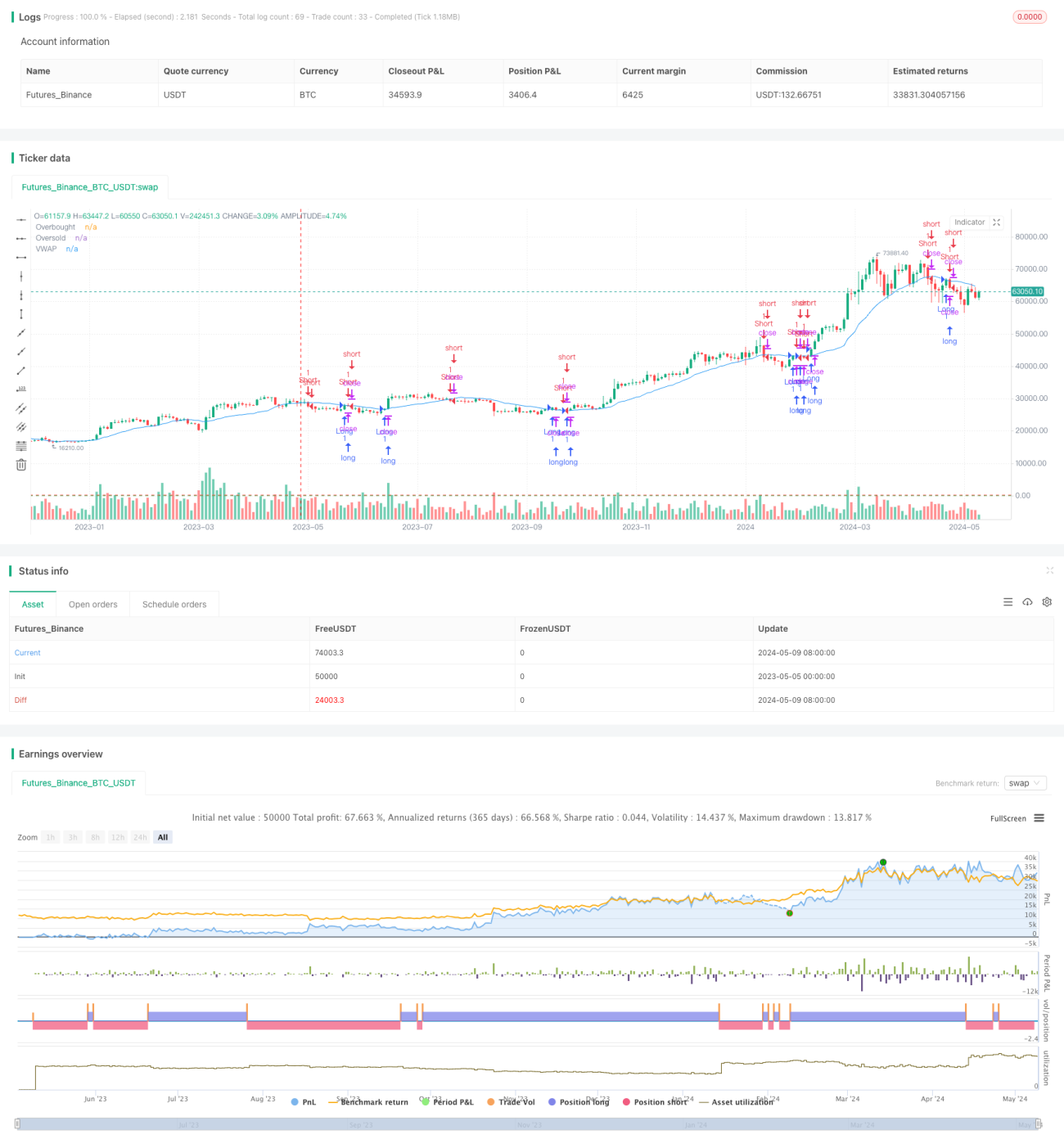

Strategi ini didasarkan pada persilangan garis VWAP dari dua kitaran yang berbeza, dan digabungkan dengan RSI untuk mengesahkan isyarat perdagangan. Sinyal multisignal dihasilkan apabila harga melangkaui garis VWAP ke atas dan RSI lebih tinggi daripada paras oversell; isyarat kosong dihasilkan apabila harga melangkaui garis VWAP ke bawah dan RSI lebih rendah daripada paras oversell.

Prinsip Strategi

- Nilai VWAP yang dikira dalam tempoh yang diberikan. VWAP adalah purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata purata

- Pengiraan RSI. RSI mengukur kekuatan relatif harga dalam jangka masa yang digunakan untuk menentukan sama ada pasaran terlalu banyak membeli atau terlalu banyak menjual.

- Apabila harga penutupan melepasi garis VWAP ke atas dan RSI lebih tinggi daripada paras oversold (default 30), ia menghasilkan isyarat melakukan lebih banyak.

- Isyarat shorting dihasilkan apabila harga penutupan melepasi garis VWAP ke bawah dan RSI berada di bawah tahap overbought (default 70)

- Apabila memegang kedudukan berbilang kepala, jika harga penutupan menembusi ke bawah garis VWAP atau RSI lebih tinggi daripada tahap overbought, ia akan ditutup.

- Apabila memegang kedudukan kosong, jika harga penutupan melangkaui garis VWAP ke atas atau RSI berada di bawah paras oversold, ia akan ditutup.

Kelebihan Strategik

- Menggabungkan maklumat mengenai harga dan jumlah transaksi. VWAP menyusun harga dan jumlah transaksi untuk mencerminkan pergerakan pasaran secara lebih menyeluruh.

- Menggunakan RSI untuk mengesahkan trend dan menyaring isyarat palsu. RSI membantu menilai kebolehpercayaan penembusan, mengurangkan kesalahan penilaian.

- Strategi terobosan mudah difahami dan dilaksanakan. Strategi ini logiknya jelas dan sesuai untuk dipelajari dan digunakan oleh pemula.

- Strategi ini boleh digunakan untuk gaya perdagangan dan pasaran yang berbeza dengan menyesuaikan VWAP dan kitaran pengiraan RSI.

Risiko Strategik

- Pilihan parameter VWAP dan RSI mempengaruhi prestasi strategi. Tetapan parameter yang tidak sesuai boleh menyebabkan perdagangan yang kerap atau kehilangan peluang yang baik.

- Strategi ini mungkin menghasilkan lebih banyak isyarat palsu di pasaran yang tidak menentu atau kurang turun naik.

- Strategi ini tidak mempertimbangkan pengurusan risiko, seperti hentikan kerugian dan kawalan kedudukan. Dalam aplikasi sebenar, langkah-langkah pengurusan risiko perlu digabungkan.

- Strategi penembusan mudah menyebabkan kerugian di pasaran yang bergolak. Strategi ini mungkin menyebabkan kerugian kerana sering berdagang ketika harga bergolak di sekitar VWAP.

Arah pengoptimuman strategi

- Pengenalan VWAP dan RSI yang mempunyai banyak tempoh masa. Meningkatkan kebolehpercayaan dan kestabilan isyarat dengan menggabungkan indikator dari pelbagai tempoh masa.

- Menambah indikator pengesahan trend, seperti purata bergerak atau ADX. Hanya berdagang di arah yang jelas trend, anda boleh meningkatkan peluang kemenangan dan keuntungan strategi.

- Mengoptimumkan peraturan masuk dan keluar. Contohnya, meminta harga melebihi peratusan VWAP semasa penembusan, atau menggunakan ATR sebagai syarat penapisan.

- Gabungan dengan petunjuk teknikal lain, seperti pita Brin atau petunjuk momentum. Untuk meningkatkan kualiti isyarat melalui pengesahan bersama beberapa petunjuk.

- Menambah pengurusan risiko, seperti kawalan stop loss dan kedudukan dinamik. Tetapan stop loss yang munasabah dapat mengurangkan risiko perdagangan tunggal, dan penyesuaian kedudukan dinamik dapat meningkatkan kecekapan penggunaan dana.

ringkaskan

Strategi penyambungan purata purata dan indeks relatif kuat adalah strategi perdagangan yang mudah dan mudah digunakan untuk mendapatkan keuntungan yang berpotensi dengan menangkap pergerakan harga berbanding VWAP. Tetapi strategi ini juga mempunyai masalah seperti pengoptimuman parameter, prestasi pasaran yang tidak stabil, kurangnya pengurusan risiko. Dengan memperkenalkan analisis jangka masa yang banyak, menggabungkan dengan petunjuk teknikal lain, mengoptimumkan peraturan masuk, dan menambahkan kaedah kawalan risiko, anda dapat meningkatkan lagi kestabilan dan kepraktisan strategi.

- 1