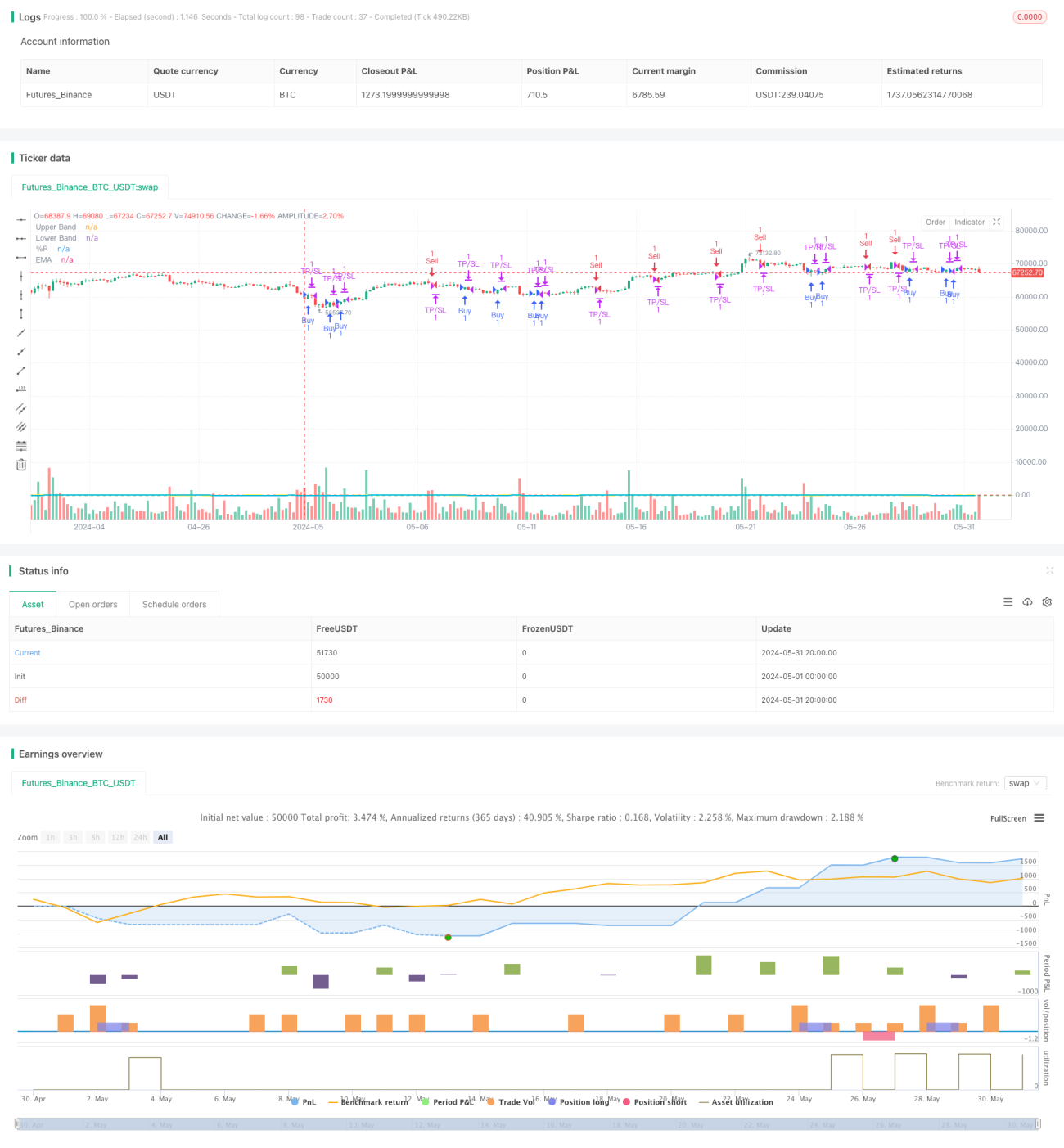

Strategi Pelarasan Dinamik Ambil Untung dan Henti Rugi Williams %R

Gambaran Keseluruhan

Strategi ini berdasarkan penunjuk Williams %R, yang mengoptimumkan prestasi dagangan dengan melaraskan tahap ambil untung/henti rugi secara dinamik. Isyarat beli dijana apabila Williams %R melintasi keluar dari kawasan terlebih jual (-80), dan isyarat jual dijana apabila ia melintasi keluar dari kawasan terlebih beli (-20). Nilai Williams %R kemudiannya dilicinkan menggunakan Purata Bergerak Eksponen (EMA) untuk mengurangkan bunyi. Strategi ini menyediakan tetapan parameter yang fleksibel, termasuk kitaran penunjuk, tahap ambil untung/henti rugi (TP/SL), waktu dagangan, dan arah dagangan, untuk menyesuaikan dengan pelbagai persekitaran pasaran dan pilihan pedagang.

Prinsip Strategi

- Kira nilai penunjuk Williams %R untuk tempoh yang diberikan.

- Kira Purata Bergerak Eksponen (EMA) bagi Williams %R.

- Apabila Williams %R melintasi dari bawah ke atas tahap -80, isyarat beli dicetuskan; apabila ia melintasi dari atas ke bawah tahap -20, isyarat jual dicetuskan.

- Selepas membeli, tetapkan tahap ambil untung dan henti rugi, dan tutup kedudukan hanya apabila tahap ambil untung/henti rugi tercapai atau Williams %R mencetuskan isyarat berlawanan.

- Selepas menjual, tetapkan tahap ambil untung dan henti rugi, dan tutup kedudukan hanya apabila tahap ambil untung/henti rugi tercapai atau Williams %R mencetuskan isyarat berlawanan.

- Pilihan untuk berdagang dalam julat waktu tertentu (contohnya 9:00-11:00) dan sama ada untuk berdagang berhampiran waktu tepat (dari X minit sebelum hingga Y minit selepas).

- Pilihan arah dagangan: hanya beli, hanya jual, atau dua arah.

Analisis Kelebihan

- Ambil Untung/Henti Rugi Dinamik: Melaraskan tahap ambil untung/henti rugi secara dinamik berdasarkan tetapan pengguna, membolehkan perlindungan keuntungan dan kawalan risiko yang lebih baik.

- Parameter Fleksibel: Pengguna boleh menetapkan pelbagai parameter mengikut keutamaan, seperti kitaran penunjuk, tahap ambil untung/henti rugi, waktu dagangan, dsb., untuk menyesuaikan dengan keadaan pasaran yang berbeza.

- Pelicinan Penunjuk: Pengenalan EMA untuk melicinkan nilai Williams %R berkesan mengurangkan bunyi penunjuk dan meningkatkan kebolehpercayaan isyarat.

- Had Masa Dagangan: Pilihan untuk berdagang dalam julat waktu tertentu, mengelakkan tempoh turun naik pasaran yang tinggi, mengurangkan risiko.

- Arah Dagangan Boleh Disesuaikan: Berdasarkan trend pasaran dan pertimbangan peribadi, pilih hanya beli, hanya jual, atau dua arah.

Analisis Risiko

- Tetapan Parameter Tidak Sesuai: Jika tetapan ambil untung/henti rugi terlalu longgar atau terlalu ketat, ia boleh menyebabkan kehilangan keuntungan atau henti rugi yang kerap.

- Kesalahan Pengenalpastian Trend: Penunjuk Williams %R berprestasi kurang baik dalam pasaran yang berayun, boleh menghasilkan isyarat palsu.

- Kesan Had Masa Terhad: Mengehadkan waktu dagangan mungkin menyebabkan strategi terlepas beberapa peluang dagangan yang baik.

- Pengoptimuman Berlebihan: Pengoptimuman parameter yang berlebihan boleh menyebabkan prestasi strategi yang lemah dalam dagangan sebenar pada masa hadapan.

Hala Tuju Pengoptimuman

- Gabungkan Penunjuk Lain: Seperti penunjuk trend, penunjuk turun naik, dsb., untuk meningkatkan ketepatan pengesahan isyarat.

- Pengoptimuman Parameter Dinamik: Laraskan parameter secara masa nyata mengikut keadaan pasaran, seperti menggunakan tetapan parameter berbeza dalam pasaran bertrend dan berayun.

- Penambahbaikan Kaedah Ambil Untung/Henti Rugi: Seperti menggunakan henti rugi menjejak, ambil untung separa, dsb., untuk melindungi keuntungan dan mengawal risiko dengan lebih baik.

- Masukkan Pengurusan Modal: Laraskan saiz kedudukan setiap dagangan secara dinamik berdasarkan baki akaun dan toleransi risiko.

Kesimpulan

Strategi Ambil Untung/Henti Rugi Dinamik Williams %R menangkap keadaan terlebih beli/terlebih jual harga dengan cara yang mudah dan berkesan, sambil menyediakan tetapan parameter yang fleksibel untuk menyesuaikan dengan pelbagai persekitaran pasaran dan gaya dagangan. Strategi ini melaraskan tahap ambil untung/henti rugi secara dinamik, membolehkan kawalan risiko dan perlindungan keuntungan yang lebih baik. Walau bagaimanapun, dalam aplikasi praktikal, faktor seperti tetapan parameter, pengesahan isyarat, dan pemilihan waktu dagangan masih perlu diberi perhatian untuk meningkatkan lagi keteguhan dan keuntungan strategi.

- 1