purata bergerak, purata bergerak mudah, kecerunan purata bergerak, henti rugi menjejak, kemasukan semula

Ringkasan

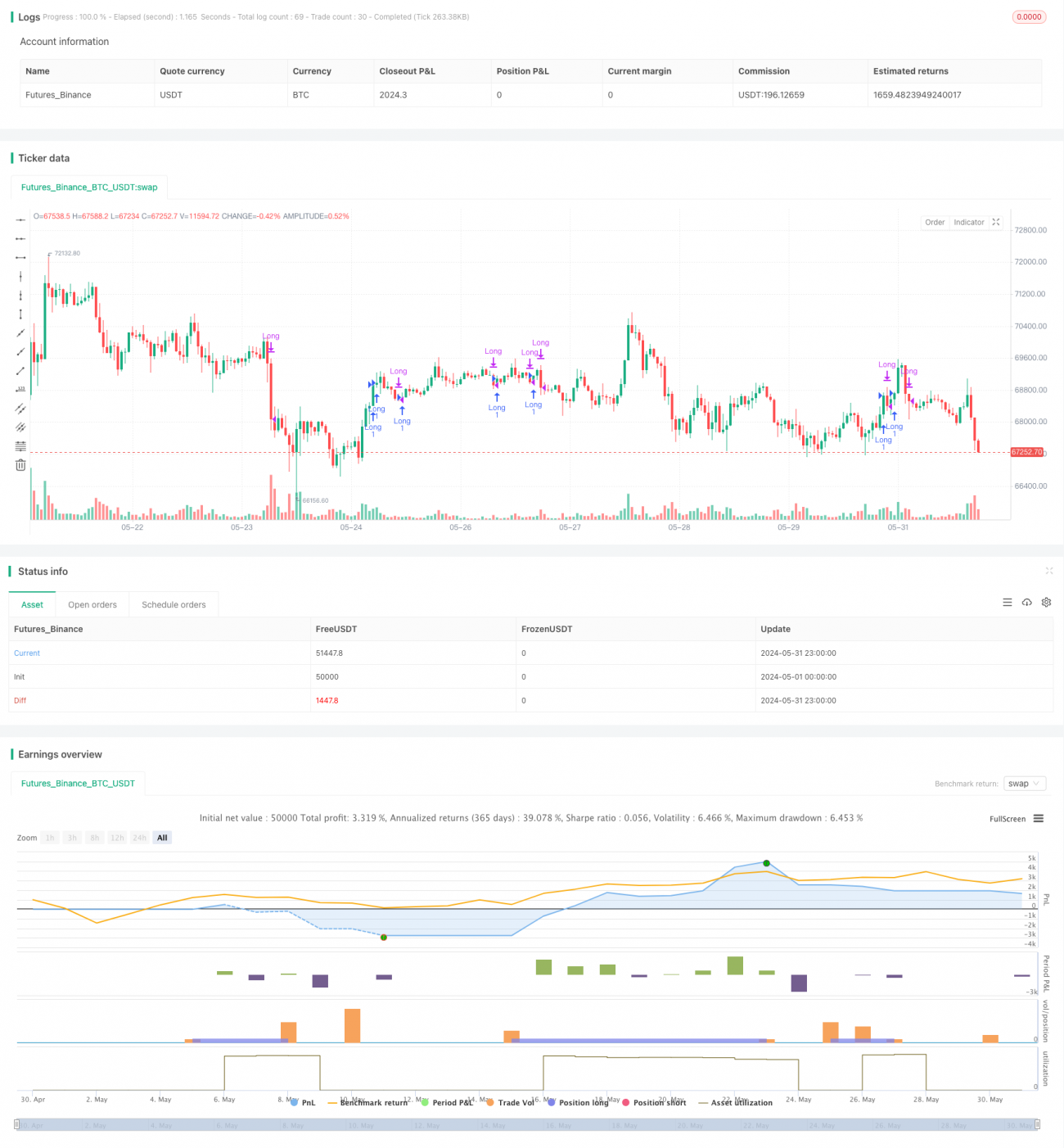

Strategi ini membuat keputusan perdagangan berdasarkan kecerunan Purata Bergerak (MA) dan kedudukan relatif harga berbanding MA. Apabila kecerunan MA melebihi ambang kecerunan minimum dan harga berada di atas MA, strategi akan membeli. Pada masa yang sama, strategi menggunakan Henti Rugi Berikutan (Trailing Stop Loss) untuk menguruskan risiko, dan masuk semula (Re-Entry) di bawah syarat tertentu. Strategi ini bertujuan untuk menangkap peluang dalam aliran menaik, sambil mengoptimumkan keuntungan dan risiko melalui henti rugi dinamik dan mekanisme masuk semula.

Prinsip Strategi

- Kira Purata Bergerak Mudah (SMA) dalam tempoh tertentu sebagai penunjuk aliran utama.

- Kira kecerunan SMA dalam tetingkap masa yang ditentukan untuk menilai kekuatan aliran semasa.

- Apabila kecerunan SMA lebih besar daripada ambang kecerunan minimum dan harga berada di atas SMA, pasaran dianggap dalam aliran menaik, dan strategi akan membeli.

- Setelah masuk, strategi menggunakan mekanisme henti rugi berikutan, melaraskan tahap henti rugi secara dinamik berdasarkan harga semasa dan peratusan yang ditetapkan.

- Jika harga mencapai tahap henti rugi berikutan, strategi akan menutup kedudukan dan menandakan berlakunya henti rugi.

- Selepas henti rugi berlaku, jika harga berundur ke peratusan tertentu di bawah SMA, strategi akan masuk semula.

- Jika harga jatuh di bawah SMA, strategi akan menutup kedudukan secara langsung.

Analisis Kelebihan

- Pengikut Aliran: Dengan menilai aliran melalui kecerunan SMA dan kedudukan relatif harga berbanding SMA, strategi membantu meraih keuntungan dalam aliran menaik.

- Henti Rugi Dinamik: Menggunakan mekanisme henti rugi berikutan, melaraskan kedudukan henti rugi berdasarkan perubahan harga, dapat melindungi keuntungan dan mengehadkan kerugian dengan lebih baik.

- Masuk Semula: Selepas henti rugi berlaku, strategi akan masuk semula apabila harga berundur ke peratusan tertentu di bawah SMA, untuk menangkap peluang pemulihan yang berpotensi.

- Parameter Fleksibel: Strategi menyediakan pelbagai parameter boleh laras seperti tempoh SMA, ambang kecerunan minimum, peratusan henti rugi berikutan, dan lain-lain, yang boleh dioptimumkan mengikut keadaan pasaran yang berbeza.

Analisis Risiko

- Kepekaan Parameter: Prestasi strategi mungkin sangat sensitif terhadap tetapan parameter; pemilihan parameter yang tidak sesuai boleh menyebabkan prestasi strategi yang lemah.

- Pengenalpastian Aliran: Strategi bergantung terutamanya pada kecerunan SMA dan kedudukan relatif harga berbanding SMA untuk menilai aliran, yang mungkin menghasilkan isyarat salah dalam keadaan pasaran tertentu.

- Kekerapan Henti Rugi: Mekanisme henti rugi berikutan boleh menyebabkan henti rugi yang kerap, terutamanya dalam pasaran yang tidak menentu, sekali gus menjejaskan prestasi keseluruhan strategi.

- Risiko Masuk Semula: Mekanisme masuk semula boleh menyebabkan strategi masuk semula dan mengalami penurunan selanjutnya dalam beberapa situasi, membesarkan kerugian.

Arah Pengoptimuman

- Pengesahan Aliran: Dalam menilai aliran, boleh menggabungkan penunjuk teknikal lain atau corak tindakan harga untuk meningkatkan ketepatan pengenalpastian aliran.

- Pengoptimuman Henti Rugi: Boleh meneroka kaedah henti rugi lain, seperti berdasarkan turun naik atau kedudukan sokongan/rintangan, untuk menyesuaikan diri dengan keadaan pasaran yang berbeza.

- Syarat Masuk Semula: Boleh mengoptimumkan syarat masuk semula, seperti mempertimbangkan magnitud pengunduran harga, tempoh masa, dan faktor lain, untuk menapis isyarat masuk semula yang tidak menguntungkan.

- Pengurusan Saiz Kedudukan: Memperkenalkan mekanisme pengurusan saiz kedudukan, melaraskan saiz kedudukan setiap dagangan berdasarkan turun naik pasaran atau penunjuk risiko lain, untuk mengawal pendedahan risiko keseluruhan.

Kesimpulan

Strategi ini menilai aliran melalui kecerunan Purata Bergerak dan kedudukan relatif harga berbanding Purata Bergerak, serta menggunakan mekanisme henti rugi berikutan dan masuk semula bersyarat untuk menguruskan dagangan. Kelebihan strategi termasuk keupayaan mengikut aliran, perlindungan henti rugi dinamik, dan penangkapan peluang masuk semula. Walau bagaimanapun, strategi juga mempunyai potensi masalah seperti kepekaan parameter, ralat pengenalpastian aliran, kekerapan henti rugi, dan risiko masuk semula. Kelemahan strategi boleh diperbaiki mengikut arah pengoptimuman seperti pengoptimuman pengenalpastian aliran, kaedah henti rugi, syarat masuk semula, dan pengurusan saiz kedudukan. Dalam aplikasi praktikal, perlu dinilai dan diselaraskan dengan berhati-hati berdasarkan ciri pasaran spesifik dan gaya perdagangan.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("MA Incline Strategy with Trailing Stop-Loss and Conditional Re-Entry", overlay=true, calc_on_every_tick=true)

// Input parameters- 1