Strategi Keluar Candelier Diperkukuh ZLSMA dan Pengesanan Nadi Volume

Gambaran Keseluruhan

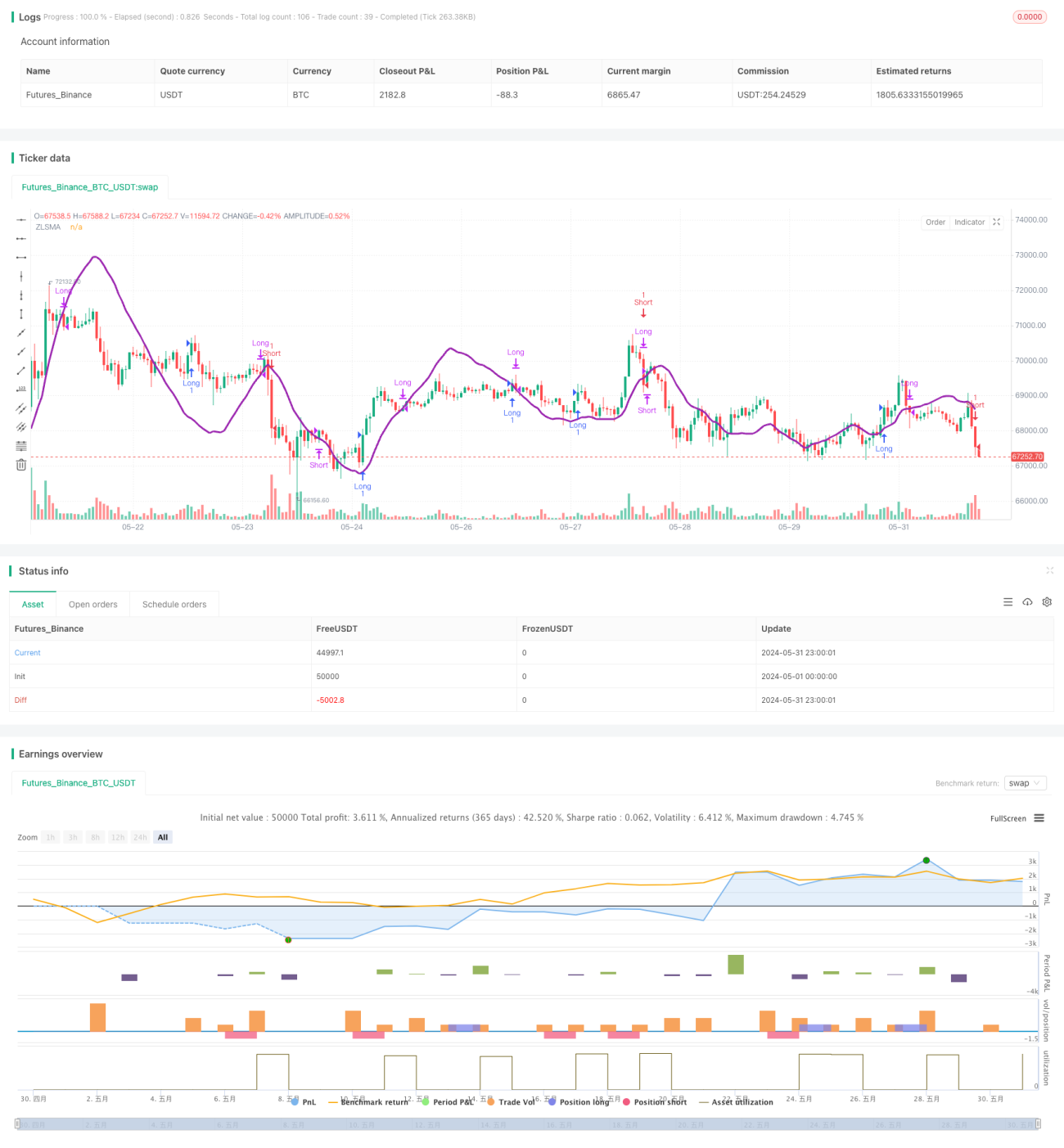

Strategi ini menggabungkan Peraturan Keluar Chandelier (Chandelier Exit), Purata Bergerak Sifar Ketinggalan (ZLSMA), dan pengesanan nadi Volume Relatif (RVOL) untuk membentuk sistem perdagangan yang lengkap. Peraturan Keluar Chandelier menyesuaikan kedudukan henti rugi secara dinamik melalui Purata Julat Sebenar (ATR), membolehkannya menyesuaikan diri dengan perubahan pasaran dengan lebih baik. ZLSMA dapat menangkap arah aliran harga dengan tepat, menyediakan panduan arah untuk perdagangan. Pengesanan nadi RVOL membantu strategi mengelakkan pasaran yang mendatar dengan turun naik yang rendah, meningkatkan kualiti perdagangan.

Prinsip Strategi

- Kira ATR, dan berdasarkan ATR serta harga tertinggi/terendah, kira kedudukan henti rugi untuk kedudukan panjang dan pendek.

- Kira ZLSMA sebagai asas untuk menentukan arah aliran.

- Kira RVOL, dan bandingkan RVOL dengan ambang yang ditetapkan untuk menentukan sama ada terdapat nadi volume.

- Masuk panjang: Harga penutup semasa melintasi ke atas ZLSMA, dan RVOL lebih besar daripada ambang, buka pesanan panjang, dengan henti rugi pada titik rendah terkini.

- Masuk pendek: Harga penutup semasa melintasi ke bawah ZLSMA, dan RVOL lebih besar daripada ambang, buka pesanan pendek, dengan henti rugi pada titik tinggi terkini.

- Keluar panjang: Harga penutup semasa melintasi ke bawah ZLSMA, tutup pesanan panjang.

- Keluar pendek: Harga penutup semasa melintasi ke atas ZLSMA, tutup pesanan pendek.

Kelebihan Strategi

- Peraturan Keluar Chandelier dapat menyesuaikan kedudukan henti rugi secara dinamik, mengurangkan risiko yang disebabkan oleh henti rugi tetap.

- ZLSMA dapat bertindak balas dengan cepat terhadap perubahan harga, memberikan penilaian arah aliran yang boleh dipercayai untuk perdagangan.

- Pengesanan nadi RVOL membantu strategi mengelakkan pasaran mendatar dengan turun naik rendah, meningkatkan kualiti perdagangan.

- Logik strategi jelas dan mudah difahami serta dilaksanakan.

Risiko Strategi

- Dalam pasaran yang tidak mempunyai arah aliran yang jelas atau sering berayun, strategi ini mungkin menghasilkan bilangan dagangan yang lebih tinggi, seterusnya meningkatkan kos yuran.

- Tetapan parameter strategi (seperti tempoh ATR, tempoh ZLSMA, ambang RVOL, dll.) mempunyai kesan yang besar terhadap prestasi strategi; parameter yang tidak sesuai boleh menyebabkan prestasi yang tidak memuaskan.

- Strategi ini tidak mengambil kira pengurusan kedudukan dan kawalan risiko; dalam aplikasi praktikal, prinsip pengurusan modal perlu digabungkan.

Arah Pengoptimuman Strategi

- Memperkenalkan penunjuk pengesahan arah aliran, seperti sistem purata bergerak atau penunjuk momentum, untuk meningkatkan lagi ketepatan penilaian arah aliran.

- Mengoptimumkan logik pengesanan nadi RVOL, misalnya dengan mempertimbangkan berlakunya beberapa nadi RVOL berturut-turut sebelum membuat dagangan, untuk meningkatkan lagi kualiti isyarat.

- Menambah logik ambil untung dalam syarat keluar; jika sasaran keuntungan tertentu dicapai, tutup kedudukan untuk mengunci keuntungan yang diperoleh.

- Mengoptimumkan parameter strategi berdasarkan ciri pasaran dan instrumen dagangan untuk mencari kombinasi parameter terbaik.

- Menggabungkan prinsip pengurusan kedudukan dan kawalan risiko untuk menyempurnakan strategi, meningkatkan kestabilan dan kebolehpercayaan strategi.

Ringkasan

Strategi ZLSMA – Peraturan Keluar Chandelier yang Dipertingkatkan dengan Pengesanan Nadi Volume merupakan strategi mengikut arah aliran yang, melalui henti rugi dinamik, penilaian arah aliran dan pengesanan nadi volume, mengawal risiko perdagangan sambil merebut peluang arah aliran. Logik strategi jelas dan mudah difahami serta dilaksanakan, namun dalam aplikasi praktikal, ia masih perlu dioptimumkan dan disempurnakan berdasarkan ciri pasaran dan instrumen dagangan tertentu. Dengan memperkenalkan lebih banyak penunjuk pengesahan isyarat, mengoptimumkan syarat keluar, menetapkan parameter secara wajar, serta pengurusan kedudukan dan kawalan risiko yang ketat, strategi ini berpotensi menjadi alat perdagangan yang stabil dan cekap.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Chandelier Exit Strategy with ZLSMA and Volume Spike Detection", shorttitle="CES with ZLSMA and Volume", overlay=true, process_orders_on_close=true, calc_on_every_tick=false)

// Chandelier Exit Inputs

lengthAtr = input.int(title='ATR Period', defval=1)- 1