Strategi Penyesuaian Portfolio Dinamik Adaptif Pelbagai Penunjuk Berdasarkan Kemeruapan ATR

Gambaran Keseluruhan

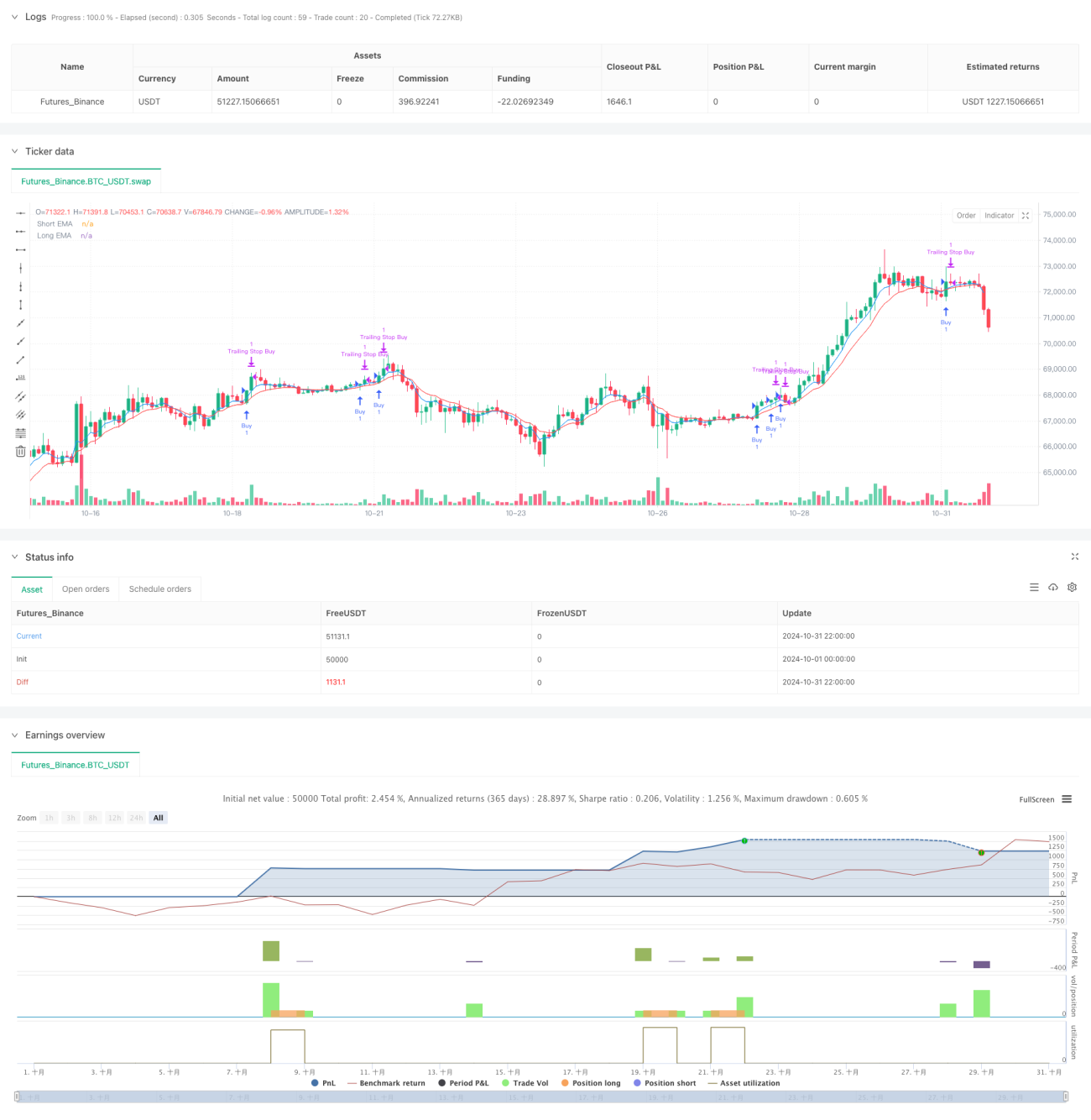

Strategi ini adalah strategi perdagangan kuantitatif berdasarkan pelbagai penunjuk teknikal dan pengurusan risiko dinamik. Ia menggabungkan pengesanan trend EMA, turun naik ATR, RSI terlebih beli/terlebih jual, dan pengiktirafan corak lilin (candlestick) melalui pelarasan kedudukan adaptif dan henti rugi dinamik untuk mencapai keseimbangan antara pulangan dan risiko. Strategi ini menggunakan kaedah ambil untung secara berperingkat dan henti rugi bergerak untuk melindungi keuntungan.

Prinsip Strategi

Strategi ini melaksanakan perdagangan melalui beberapa aspek utama:

- Menggunakan persilangan purata bergerak EMA 5 kitaran dan 10 kitaran untuk menentukan arah trend

- Melalui penunjuk RSI untuk mengenal pasti kawasan terlebih beli/terlebih jual, mengelakkan mengejar kenaikan atau menjual dalam kejatuhan

- Menggunakan penunjuk ATR untuk melaraskan kedudukan henti rugi dan saiz posisi secara dinamik

- Menggabungkan pengiktirafan corak lilin (menelan, tukul, bintang jatuh) sebagai isyarat masuk tambahan

- Menggunakan mekanisme pampasan gelinciran dinamik berdasarkan ATR

- Menggunakan pengesahan volum dagangan untuk menapis isyarat palsu

Kelebihan Strategi

- Pengesahan silang berbilang isyarat meningkatkan kebolehpercayaan perdagangan

- Pengurusan risiko dinamik, menyesuaikan secara adaptif mengikut turun naik pasaran

- Strategi ambil untung berperingkat, mengunci sebahagian keuntungan secara wajar

- Menggunakan henti rugi bergerak untuk melindungi keuntungan sedia ada

- Menetapkan had henti rugi harian untuk mengawal pendedahan risiko

- Pampasan gelinciran dinamik meningkatkan kadar pelaksanaan pesanan

Risiko Strategi

- Berbilang penunjuk boleh menyebabkan ketinggalan isyarat

- Perdagangan kerap boleh menjana kos yang tinggi

- Dalam pasaran yang bergelora, henti rugi mungkin kerap berlaku

- Pengiktirafan corak lilin mempunyai faktor subjektif

- Pengoptimuman parameter boleh menyebabkan overfitting

Arah Pengoptimuman Strategi

- Memperkenalkan pertimbangan kitaran turun naik pasaran, melaraskan parameter secara dinamik

- Menambah penapis kekuatan trend untuk mengurangkan isyarat palsu

- Mengoptimumkan algoritma pengurusan posisi untuk meningkatkan kecekapan penggunaan modal

- Menambah lebih banyak penunjuk sentimen pasaran

- Membangunkan sistem pengoptimuman parameter adaptif

Kesimpulan

Ini adalah sistem strategi matang yang menggabungkan pelbagai penunjuk teknikal, meningkatkan kestabilan perdagangan melalui pengurusan risiko dinamik dan pengesahan isyarat berbilang. Kelebihan teras strategi terletak pada kebolehsuaian dan sistem kawalan risiko yang komprehensif, namun masih memerlukan pengesahan dan pengoptimuman berterusan dalam dagangan sebenar.

- 1