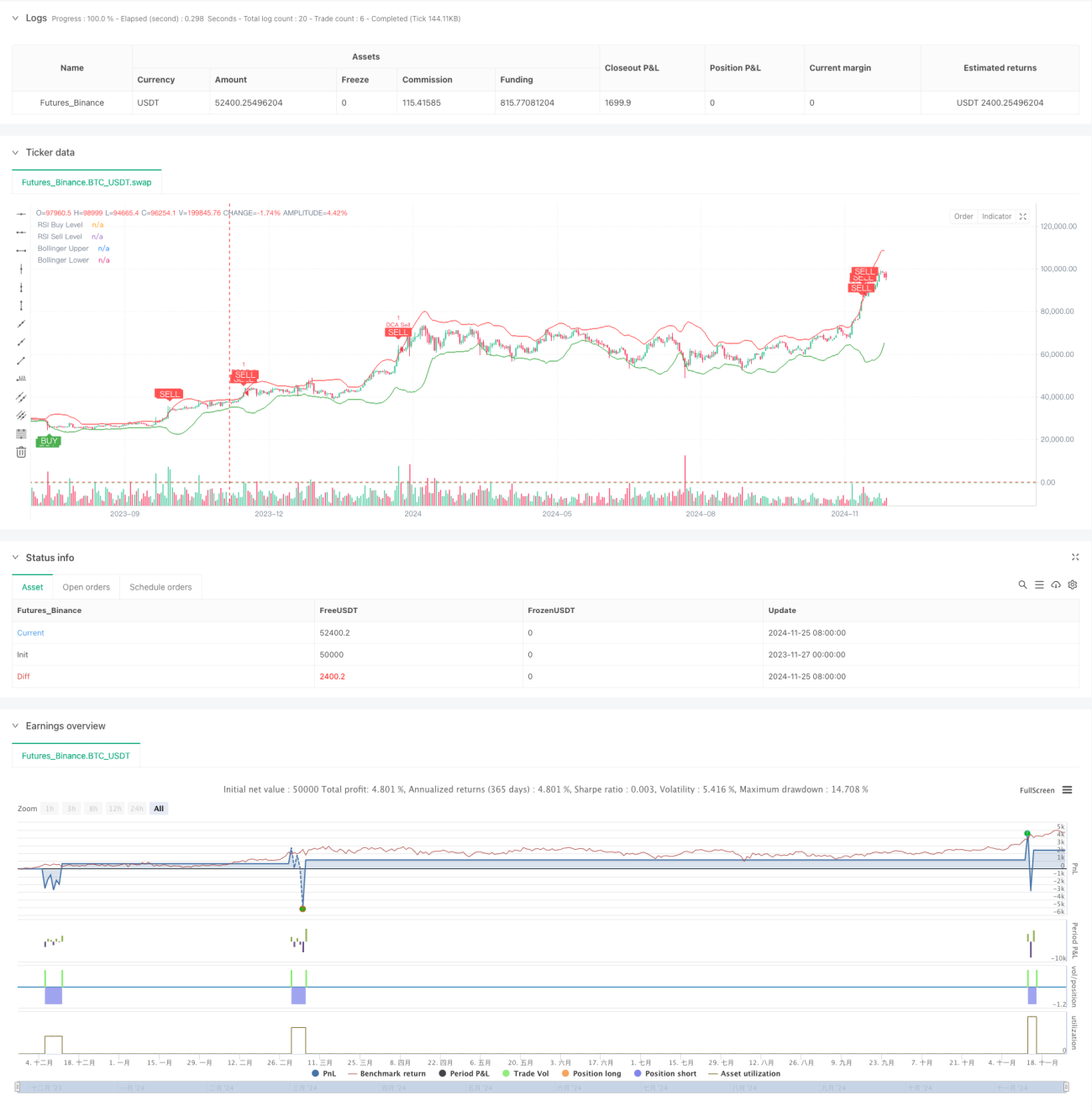

Ringkasan

Strategi ini adalah sistem dagangan kuantitatif yang menggabungkan Bollinger Bands, Indeks Kekuatan Relatif (RSI) dan Purata Kos Dinamik (DCA). Strategi ini menetapkan peraturan pengurusan modal, secara automatik melaksanakan pembinaan kedudukan berperingkat dalam turun naik pasaran, sambil menggabungkan penunjuk teknikal untuk menentukan isyarat beli dan jual, mencapai pelaksanaan dagangan dengan risiko terkawal. Sistem ini juga merangkumi fungsi ambil untung dan penjejakan keuntungan terkumpul untuk memantau dan mengurus prestasi dagangan dengan berkesan.

Prinsip Strategi

Strategi beroperasi berdasarkan beberapa komponen teras berikut:

- Bollinger Bands digunakan untuk menentukan julat pergerakan harga. Apabila harga menyentuh jalur bawah, pertimbangkan untuk membeli; apabila menyentuh jalur atas, pertimbangkan untuk menjual.

- Indeks RSI mengesahkan keadaan terlebih beli atau terlebih jual pasaran. RSI di bawah 25 mengesahkan terlebih jual, di atas 75 mengesahkan terlebih beli.

- Modul DCA mengira jumlah pesanan setiap kali secara dinamik berdasarkan ekuiti akaun untuk mencapai pengurusan modal adaptif.

- Modul ambil untung menetapkan sasaran keuntungan 5%. Apabila sasaran tercapai, kedudukan ditutup secara automatik untuk melindungi keuntungan.

- Modul pemantauan keadaan pasaran mengira magnitud perubahan pasaran dalam tempoh 90 hari untuk membantu menilai arah aliran keseluruhan.

- Modul penjejakan keuntungan terkumpul merekod untung rugi setiap dagangan untuk memudahkan penilaian prestasi strategi.

Kelebihan Strategi

- Menggabungkan pengesahan silang pelbagai penunjuk teknikal untuk meningkatkan kebolehpercayaan isyarat.

- Mengguna pakai pengurusan kedudukan dinamik untuk mengelakkan risiko kedudukan tetap.

- Menetapkan syarat ambil untung yang munasabah untuk mengunci keuntungan tepat pada masanya.

- Mempunyai fungsi pemantauan arah aliran pasaran untuk memudahkan pemahaman gambaran besar.

- Sistem penjejakan keuntungan yang lengkap untuk memudahkan analisis prestasi strategi.

- Konfigurasi fungsi amaran yang baik untuk mengingatkan peluang dagangan secara masa nyata.

Risiko Strategi

- Pasaran julat mungkin mencetuskan isyarat dengan kerap, menyebabkan peningkatan kos dagangan.

- Indikator RSI mungkin mengalami ketinggalan dalam pasaran berarah.

- Ambil untung peratusan tetap mungkin menyebabkan keluar terlalu awal dalam pasaran berarah kukuh.

- Strategi DCA mungkin menyebabkan pengeluaran yang besar dalam pasaran menurun satu arah.

Cadangan untuk mengurus risiko termasuk:

- Menetapkan had pegangan maksimum.

- Melaraskan parameter secara dinamik berdasarkan turun naik pasaran.

- Menambah penapis arah aliran.

- Melaksanakan strategi ambil untung berperingkat.

Arah Pengoptimuman Strategi

- Pengoptimuman parameter dinamik:

- Parameter Bollinger Bands boleh dilaras secara adaptif berdasarkan turun naik.

- Ambang RSI boleh berubah mengikut kitaran pasaran.

- Nisbah modal DCA boleh dilaras mengikut saiz akaun.

- Peningkatan sistem isyarat:

- Menambah pengesahan volum dagangan.

- Menambah analisis garis arah aliran.

- Menggabungkan lebih banyak penunjuk teknikal untuk pengesahan silang.

- Penambahbaikan kawalan risiko:

- Melaksanakan henti rugi dinamik.

- Menambah kawalan pengeluaran maksimum.

- Menetapkan had kerugian harian.

Kesimpulan

Strategi ini membina satu sistem dagangan yang agak lengkap dengan menggabungkan secara menyeluruh analisis teknikal dan kaedah pengurusan modal. Kelebihan strategi terletak pada pengesahan isyarat berganda dan pengurusan risiko yang sempurna, namun masih memerlukan ujian dan pengoptimuman secukupnya dalam dagangan sebenar. Dengan penambahbaikan berterusan pada tetapan parameter dan penambahan penunjuk bantuan, strategi ini berpotensi mencapai prestasi yang stabil dalam dagangan sebenar.

/*backtest

start: 2023-11-27 00:00:00

end: 2024-11-26 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Combined BB RSI with Cumulative Profit, Market Change, and Futures Strategy (DCA)", shorttitle="BB RSI Combined DCA Strategy", overlay=true)

// Input Parameters- 1