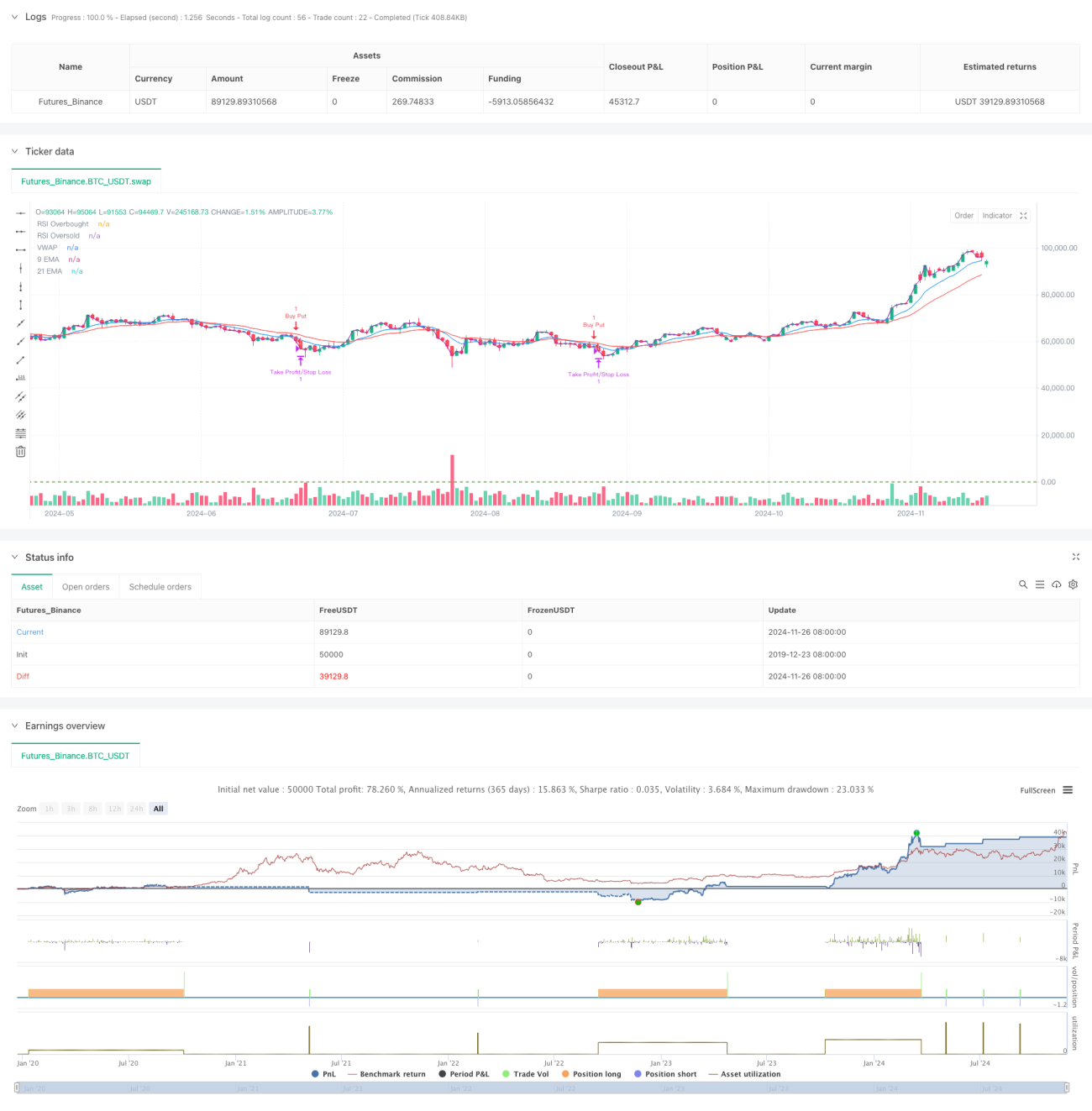

Gambaran Keseluruhan

Strategi ini adalah sistem perdagangan frekuensi tinggi berdasarkan pelbagai penunjuk teknikal, menggunakan jangka masa 5 minit, menggabungkan sistem purata bergerak, penunjuk momentum dan analisis volum. Strategi ini menyesuaikan secara dinamik untuk menyesuaikan dengan turun naik pasaran, menggunakan pengesahan isyarat berganda untuk meningkatkan ketepatan dan kebolehpercayaan perdagangan. Inti strategi terletak pada kombinasi penunjuk teknikal pelbagai dimensi untuk menangkap trend pasaran jangka pendek, sambil menggunakan henti rugi dinamik untuk mengawal risiko.

Prinsip Strategi

Strategi ini menggunakan sistem purata bergerak berganda (EMA 9 tempoh dan 21 tempoh) sebagai alat utama untuk menentukan arah aliran, digabungkan dengan penunjuk RSI untuk pengesahan momentum. Apabila harga berada di atas kedua-dua purata bergerak dan RSI berada dalam julat 40-65, sistem akan mencari peluang untuk membeli (long); apabila harga berada di bawah kedua-dua purata bergerak dan RSI berada dalam julat 35-60, sistem akan mencari peluang untuk menjual (short). Pada masa yang sama, strategi memperkenalkan mekanisme pengesahan volum yang memerlukan volum semasa melebihi 1.2 kali ganda purata volum bergerak 20 tempoh. Penggunaan VWAP seterusnya memastikan arah perdagangan konsisten dengan trend utama intra-hari.

Kelebihan Strategi

- Mekanisme pengesahan isyarat berganda meningkatkan kebolehpercayaan perdagangan dengan ketara

- Tetapan ambil untung dan henti rugi dinamik dapat menyesuaikan dengan persekitaran pasaran yang berbeza

- Menggunakan ambang RSI yang agak konservatif, mengelakkan perdagangan di kawasan ekstrem

- Mekanisme pengesahan volum berkesan menapis isyarat palsu

- Penggunaan VWAP membantu memastikan arah perdagangan selaras dengan modal utama

- Sistem purata bergerak yang responsif sesuai untuk menangkap peluang pasaran jangka pendek

Risiko Strategi

- Dalam pasaran yang bergerak mendatar (sideways) mungkin menghasilkan isyarat palsu yang kerap

- Had pelbagai syarat boleh menyebabkan terlepas beberapa peluang perdagangan

- Perdagangan frekuensi tinggi mungkin menghadapi kos perdagangan yang tinggi

- Mungkin bertindak balas perlahan apabila pasaran berubah dengan pantas

- Memerlukan data pasaran masa nyata yang tinggi

Arah Pengoptimuman Strategi

- Memperkenalkan mekanisme penyesuaian parameter secara automatik, membolehkan strategi melaraskan parameter penunjuk secara dinamik berdasarkan keadaan pasaran

- Menambah modul pengenalpastian persekitaran pasaran, menggunakan strategi perdagangan berbeza dalam keadaan pasaran yang berbeza

- Mengoptimumkan syarat penapisan volum, boleh mempertimbangkan penggunaan volum relatif atau analisis profil volum

- Menambah baik mekanisme henti rugi, boleh mempertimbangkan menambah fungsi henti rugi menjejak (trailing stop)

- Menambah penapisan masa perdagangan, mengelakkan tempoh pembukaan dan penutupan yang lebih tidak menentu

Kesimpulan

Strategi ini membina sistem perdagangan yang agak lengkap melalui penggunaan gabungan pelbagai penunjuk teknikal. Kelebihan strategi terletak pada mekanisme pengesahan isyarat pelbagai dimensi dan kaedah kawalan risiko dinamik. Walaupun terdapat beberapa potensi risiko, dengan pengoptimuman parameter yang sesuai dan pengurusan risiko, strategi ini masih mempunyai nilai aplikasi yang baik. Disarankan agar peniaga menjalankan ujian semula yang mencukupi sebelum menggunakan secara langsung, dan membuat pelarasan parameter yang sesuai berdasarkan keadaan pasaran tertentu.

- 1