Strategi ini adalah sistem perdagangan kuantitatif berdasarkan pengayun RSI dinamik. Ia mengira kadar perubahan RSI untuk menangkap momentum pasaran melalui pelarasan polinomial dan analisis siri masa pada penunjuk RSI. Strategi ini menggunakan kaedah matematik lanjutan seperti penguraian QR untuk pemprosesan isyarat, dan menggabungkan sistem purata bergerak untuk membuat keputusan perdagangan.

Prinsip Strategi

Teras strategi ini adalah pengayun Delta-RSI, yang dilaksanakan melalui langkah-langkah berikut:

- Mula-mula mengira RSI tradisional sebagai data asas

- Menggunakan pelarasan polinomial untuk melicinkan RSI, mengurangkan hingar

- Mengira terbitan masa RSI untuk mendapatkan Delta-RSI, mencerminkan kadar perubahan RSI

- Membandingkan Delta-RSI dengan purata bergeraknya untuk menjana isyarat perdagangan

- Menggunakan punca min kuasa dua ralat (RMSE) untuk menilai dan menapis kualiti pelarasan

Isyarat perdagangan boleh dihasilkan melalui tiga cara:

- Persilangan garis sifar: Beli apabila Delta-RSI bertukar dari negatif ke positif, jual apabila bertukar dari positif ke negatif

- Persilangan garis isyarat: Beli/jual apabila Delta-RSI menembusi ke atas/ke bawah purata bergeraknya

- Perubahan arah: Beli apabila Delta-RSI mula meningkat di kawasan negatif, jual apabila mula menurun di kawasan positif

Kelebihan Strategi

- Asas matematik yang kukuh: menggunakan kaedah matematik lanjutan seperti penguraian QR untuk pemprosesan isyarat, teori yang boleh dipercayai

- Isyarat licin: pelarasan polinomial dapat menapis hingar pasaran dengan berkesan, meningkatkan kualiti isyarat

- Fleksibiliti tinggi: menyediakan pelbagai kaedah penjanaan isyarat dan pilihan parameter, menyesuaikan dengan persekitaran pasaran yang berbeza

- Risiko terkawal: termasuk mekanisme penapisan RMSE, dapat memilih isyarat yang lebih dipercayai

- Pengiraan cekap: operasi matriks menggunakan algoritma yang dioptimumkan, kecekapan pengiraan yang tinggi

Risiko Strategi

- Kepekaan parameter: beberapa parameter utama perlu dilaraskan dengan teliti, pemilihan parameter yang tidak sesuai akan menjejaskan prestasi strategi dengan serius

- Ketinggalan: pemprosesan isyarat yang licin akan menyebabkan sedikit ketinggalan, mungkin terlepas pergerakan pasaran yang pantas

- Penembusan palsu: dalam pasaran berayun mungkin menghasilkan isyarat palsu, meningkatkan kos perdagangan

- Kerumitan pengiraan: melibatkan banyak operasi matriks, mungkin terdapat masalah prestasi dalam perdagangan frekuensi tinggi

- Terlebih pelarasan: semasa mengoptimumkan parameter perlu berhati-hati untuk mengelakkan terlalu menyesuaikan dengan data sejarah

Arah Pengoptimuman Strategi

- Parameter adaptif: boleh melaraskan tempoh RSI dan darjah pelarasan secara dinamik berdasarkan turun naik pasaran

- Pelbagai jangka masa: menggabungkan isyarat dari lebih banyak jangka masa untuk pengesahan silang

- Penapisan turun naik: menambah penunjuk turun naik seperti ATR untuk penapisan isyarat

- Klasifikasi pasaran: menggunakan peraturan penjanaan isyarat yang berbeza untuk keadaan pasaran yang berbeza (trend/berayun)

- Pengoptimuman henti rugi: menambah mekanisme henti rugi yang lebih pintar, seperti henti rugi dinamik berdasarkan tahap sokongan dan rintangan

Kesimpulan

Ini adalah strategi perdagangan kuantitatif yang berstruktur lengkap dan asas teori yang kukuh. Melalui analisis ciri dinamik RSI, digabungkan dengan kaedah matematik moden untuk pemprosesan isyarat, ia mampu menangkap trend pasaran dengan baik. Walaupun terdapat beberapa isu kepekaan parameter dan kerumitan pengiraan, dengan pemilihan parameter yang munasabah dan penambahbaikan pengoptimuman, strategi ini mempunyai nilai aplikasi yang baik. Adalah disyorkan untuk memberi perhatian kepada kawalan risiko semasa penggunaan sebenar, menetapkan saiz kedudukan dengan munasabah, dan memantau prestasi strategi secara berterusan.

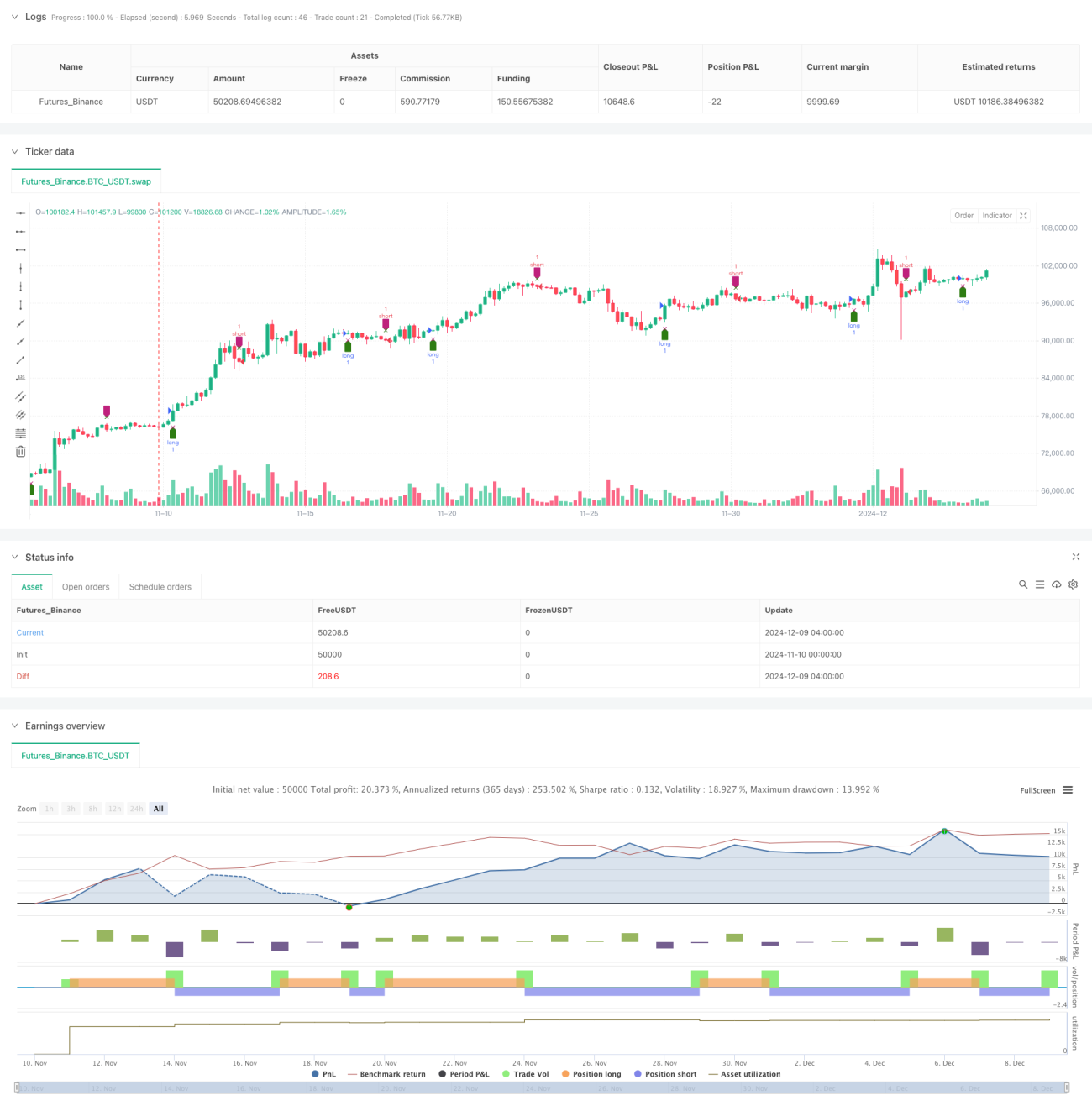

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tbiktag

//

// Delta-RSI Oscillator Strategy- 1