Gambaran Keseluruhan

Strategi ini adalah sistem perdagangan pintar yang menggabungkan MACD (Moving Average Convergence Divergence) dan kecerunan regresi linear (LRS). Strategi ini mengoptimumkan pengiraan penunjuk MACD melalui gabungan pelbagai kaedah purata bergerak, dan memperkenalkan analisis regresi linear untuk meningkatkan kebolehpercayaan isyarat perdagangan. Strategi ini membolehkan pedagang memilih secara fleksibel untuk menggunakan penunjuk tunggal atau gabungan dua penunjuk untuk menjana isyarat perdagangan, dan dilengkapi dengan mekanisme ambil untung dan henti rugi untuk mengawal risiko.

Prinsip Strategi

Teras strategi adalah untuk menangkap arah aliran pasaran melalui MACD yang dioptimumkan dan penunjuk regresi linear. Bahagian MACD menggunakan gabungan empat kaedah purata bergerak: SMA, EMA, WMA, dan TEMA untuk meningkatkan kepekaan terhadap arah aliran harga. Bahagian regresi linear menentukan arah dan kekuatan arah aliran dengan mengira kecerunan dan kedudukan garis regresi. Isyarat beli boleh berdasarkan persilangan emas MACD, arah aliran menaik regresi linear, atau gabungan kedua-duanya. Begitu juga, isyarat jual boleh dikonfigurasikan secara fleksibel. Strategi ini juga merangkumi tetapan ambil untung dan henti rugi berdasarkan peratusan untuk menguruskan nisbah risiko-ke-pulangan setiap perdagangan dengan berkesan.

Kelebihan Strategi

- Fleksibiliti gabungan penunjuk: Boleh memilih penunjuk tunggal atau gabungan dua penunjuk berdasarkan keadaan pasaran

- Pengiraan MACD yang diperbaiki: Meningkatkan ketepatan pengenalpastian arah aliran melalui pelbagai kaedah purata bergerak

- Pengesahan arah aliran yang objektif: Menggunakan regresi linear untuk menyediakan penilaian arah aliran yang disokong oleh statistik matematik

- Pengurusan risiko yang lengkap: Mengintegrasikan mekanisme ambil untung dan henti rugi

- Kebolehlarasan parameter yang tinggi: Parameter utama boleh dioptimumkan mengikut ciri pasaran yang berbeza

Risiko Strategi

- Kepekaan parameter: Mungkin memerlukan pelarasan parameter yang kerap dalam persekitaran pasaran yang berbeza

- Kelewatan isyarat: Penunjuk purata bergerak mempunyai ketinggalan tertentu

- Tidak sesuai untuk pasaran berayun: Mungkin menghasilkan isyarat palsu dalam pasaran yang tidak menentu dan mendatar

- Kos peluang daripada pengesahan berganda: Pengesahan berganda yang ketat mungkin menyebabkan kehilangan beberapa peluang perdagangan yang baik

Arah Pengoptimuman Strategi

- Menambah pengenalpastian persekitaran pasaran: Memperkenalkan penunjuk volatiliti untuk membezakan pasaran aliran dan pasaran berayun

- Pelarasan parameter dinamik: Melaraskan parameter MACD dan regresi linear secara automatik berdasarkan keadaan pasaran

- Mengoptimumkan ambil untung dan henti rugi: Memperkenalkan ambil untung dan henti rugi dinamik, melaraskan secara automatik berdasarkan turun naik pasaran

- Menambah analisis volum dagangan: Menggabungkan penunjuk volum untuk meningkatkan kebolehpercayaan isyarat

- Memperkenalkan analisis jangka masa: Mempertimbangkan pengesahan jangka masa berbilang untuk meningkatkan ketepatan perdagangan

Kesimpulan

Strategi ini mencipta sistem perdagangan yang menggabungkan fleksibiliti dan kebolehpercayaan dengan menggabungkan versi penunjuk klasik yang diperbaiki dan kaedah statistik. Reka bentuk modularnya membolehkan pedagang melaraskan parameter strategi dan mekanisme pengesahan isyarat secara fleksibel mengikut persekitaran pasaran yang berbeza. Melalui pengoptimuman dan penambahbaikan yang berterusan, strategi ini diharapkan dapat mengekalkan prestasi yang stabil dalam pelbagai keadaan pasaran.

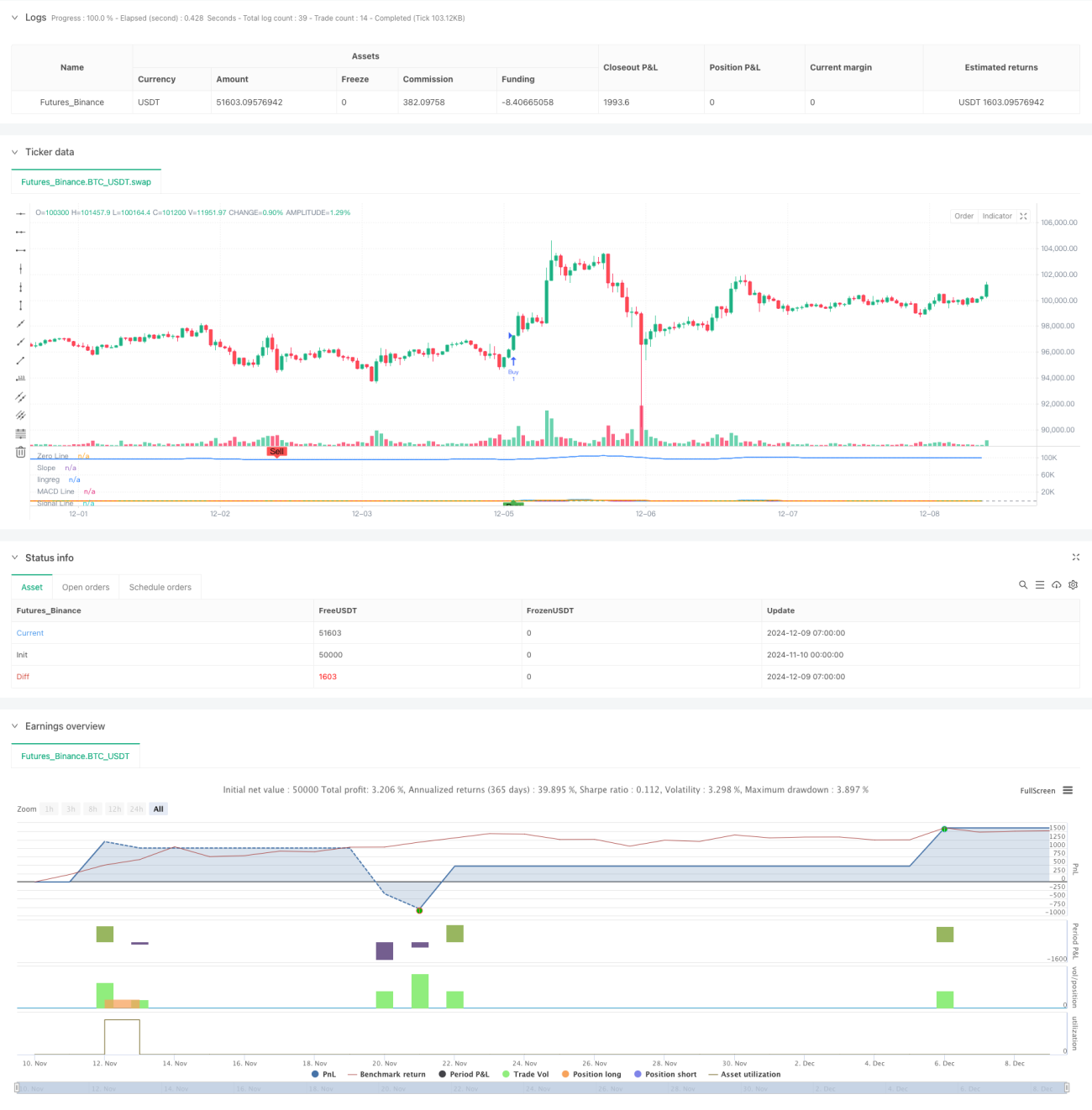

/*backtest

start: 2024-11-10 00:00:00

end: 2024-12-09 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy('SIMPLIFIED MACD & LRS Backtest by NHBProd', overlay=false)

// Function to calculate TEMA (Triple Exponential Moving Average)- 1