Strategi Penjejakan Amplitud Dinamik Trend Berbilang Kitaran

Gambaran Keseluruhan

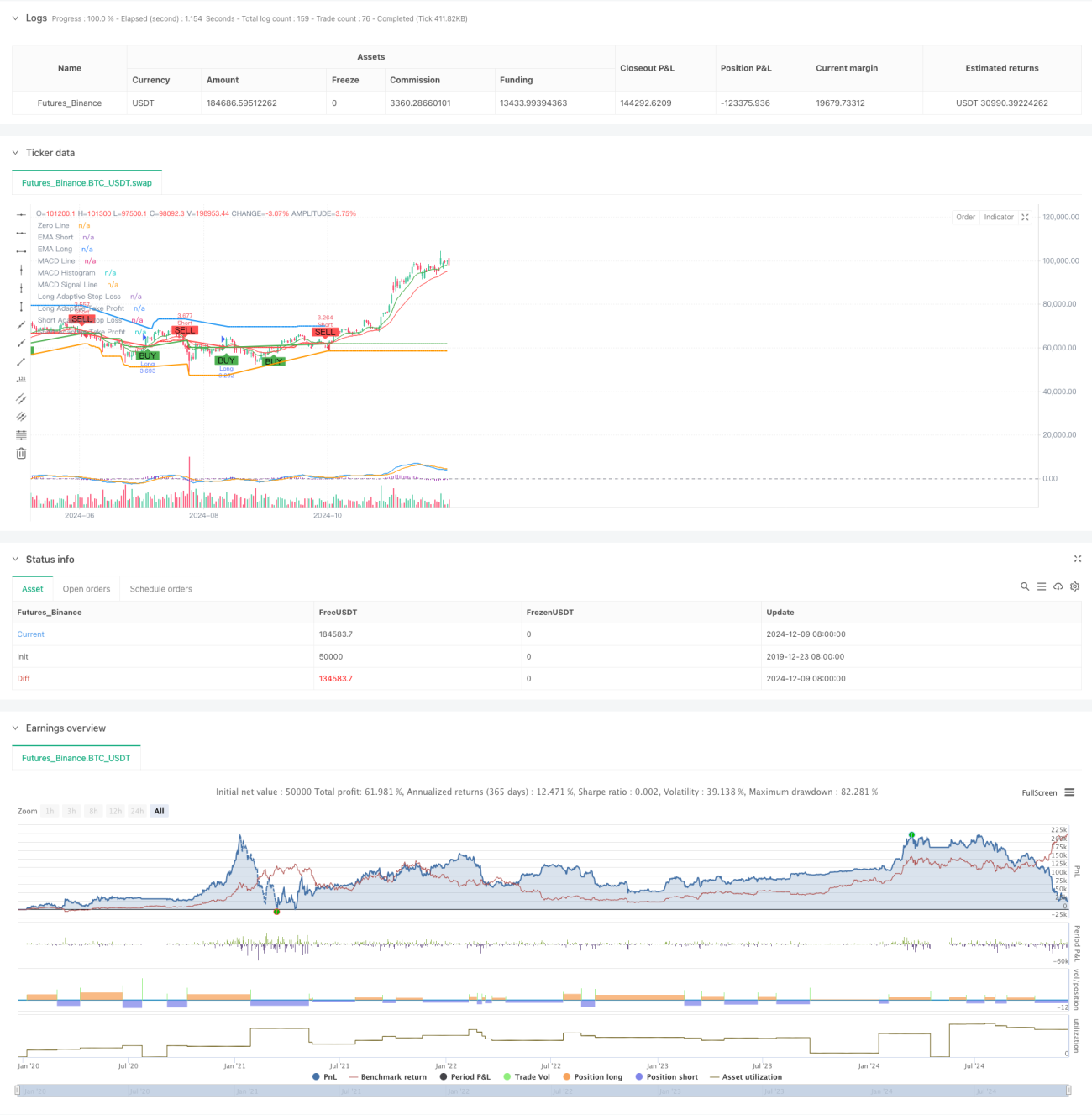

Strategi ini adalah sistem penjejakan trend adaptif yang menggabungkan pelbagai indikator teknikal. Ia mengoptimumkan prestasi perdagangan melalui analisis pelbagai kitaran dan pelarasan dinamik tahap stop loss dan take profit. Teras strategi adalah menggunakan sistem purata bergerak untuk mengenal pasti trend, mengesahkan kekuatan trend dengan RSI dan MACD, serta melaraskan parameter pengurusan risiko secara dinamik berdasarkan ATR.

Prinsip Strategi

Strategi ini menggunakan mekanisme pengesahan tiga kali ganda untuk membuat perdagangan: 1) Menentukan arah trend melalui persilangan EMA cepat dan perlahan; 2) Menapis isyarat perdagangan dengan menggunakan tahap overbought/oversold RSI dan pengesahan trend MACD; 3) Memperkenalkan EMA tempoh masa yang lebih tinggi untuk pengesahan trend. Dari segi kawalan risiko, strategi melaraskan stop loss dan sasaran keuntungan secara dinamik berdasarkan ATR, mencapai pengurusan posisi adaptif. Apabila turun naik pasaran meningkat, sistem akan secara automatik meluaskan ruang stop loss dan ambil untung; apabila pasaran menjadi tenang, ia akan mengetatkan parameter ini untuk meningkatkan kadar kemenangan.

Kelebihan Strategi

- Mekanisme pengesahan isyarat pelbagai dimensi meningkatkan ketepatan perdagangan dengan ketara.

- Tetapan stop loss dan take profit adaptif dapat menyesuaikan diri dengan lebih baik dengan persekitaran pasaran yang berbeza.

- Pengesahan trend dari tempoh masa yang lebih tinggi mengurangkan risiko pemecahan palsu dengan berkesan.

- Sistem peringatan yang lengkap membantu merebut peluang perdagangan dan mengawal risiko tepat pada masanya.

- Arah perdagangan yang fleksibel membolehkan strategi menyesuaikan diri dengan pelbagai keutamaan perdagangan.

Risiko Strategi

- Mekanisme pengesahan berganda boleh menyebabkan terlepas peluang dalam pergerakan pasaran pantas.

- Dalam pasaran yang sangat tidak menentu, stop loss dinamik boleh dicetuskan terlalu awal.

- Dalam pasaran sideways, mungkin menghasilkan isyarat palsu yang kerap.

- Terdapat risiko overfitting dalam proses pengoptimuman parameter.

- Analisis pelbagai kitaran boleh menghasilkan isyarat yang bercanggah pada tempoh masa yang berbeza.

Arah Pengoptimuman Strategi

- Memperkenalkan indikator volum sebagai pengesahan tambahan untuk meningkatkan kebolehpercayaan isyarat.

- Menambah sistem skor kuantitatif untuk kekuatan trend, mengoptimumkan masa masuk.

- Membangunkan mekanisme pengoptimuman parameter adaptif untuk meningkatkan kestabilan strategi.

- Menambah sistem klasifikasi persekitaran pasaran, menggunakan parameter berbeza untuk pasaran yang berbeza.

- Membangunkan sistem pengurusan posisi dinamik, melaraskan saiz posisi berdasarkan kekuatan isyarat.

Kesimpulan

Ini adalah sistem penjejakan trend yang direka dengan teliti, menyediakan penyelesaian perdagangan yang komprehensif melalui mekanisme pengesahan berlapis dan pengurusan risiko dinamik. Kelebihan teras strategi terletak pada kebolehsuaian dan keupayaan kawalan risikonya, namun perlu memberi perhatian kepada isu padanan antara pengoptimuman parameter dan persekitaran pasaran semasa penggunaan. Melalui pengoptimuman dan penambahbaikan berterusan, strategi ini berpotensi mengekalkan prestasi stabil dalam pelbagai keadaan pasaran.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-10 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("TrenGuard Adaptive ATR Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100)

// Parameters- 1