Sistem Penjejakan Isyarat Perdagangan Kuantitatif dan Pengoptimuman Strategi Keluar yang Pelbagai

Gambaran Keseluruhan

Strategi ini adalah sistem perdagangan kuantitatif berdasarkan isyarat LuxAlgo® dan penunjuk tindanan. Ia terutamanya membuka kedudukan panjang dengan menangkap keadaan amaran tersuai, dan menggabungkan beberapa isyarat keluar untuk menguruskan pegangan. Sistem ini menggunakan reka bentuk modular, menyokong penggunaan gabungan pelbagai keadaan keluar, termasuk henti rugi menjejak pintar, pengesahan pembalikan arah aliran, dan henti rugi peratusan tradisional. Selain itu, sistem ini juga menyokong penambahan kedudukan atas pegangan sedia ada, memberikan fleksibiliti yang lebih besar dalam pengurusan modal.

Prinsip Strategi

Logik teras strategi merangkumi beberapa bahagian utama berikut:

- Sistem Isyarat Masuk: Mencetuskan isyarat masuk panjang melalui keadaan amaran tersuai LuxAlgo®.

- Pengurusan Penambahan Kedudukan: Secara pilihan boleh mengaktifkan fungsi penambahan kedudukan untuk meningkatkan saiz kedudukan atas pegangan sedia ada.

- Mekanisme Keluar Pelbagai Lapisan:

- Henti Rugi Menjejak Pintar: Memantau hubungan harga dengan garis penjejak pintar.

- Pengesahan Keluar Arah Aliran: Termasuk isyarat pengesahan pendek asas dan dipertingkatkan.

- Isyarat Keluar Terbina: Menggunakan pelbagai keadaan keluar yang disediakan oleh penunjuk itu sendiri.

- Henti Rugi Tradisional: Menyokong tetapan henti rugi tetap berasaskan peratusan.

- Pengurusan Tetingkap Masa: Menyediakan fungsi tetapan julat tarikh ujian semula yang fleksibel.

Kelebihan Strategi

- Pengurusan Risiko Sistematik: Melalui mekanisme keluar pelbagai lapisan, risiko penurunan dapat dikawal dengan berkesan.

- Pengurusan Pegangan Fleksibel: Menyokong pelbagai strategi penambahan dan pengurangan kedudukan, boleh disesuaikan secara dinamik mengikut keadaan pasaran.

- Kebolehsesuaian Tinggi: Pengguna bebas menggabungkan keadaan keluar yang berbeza untuk mencipta sistem perdagangan peribadi.

- Reka Bentuk Modular: Setiap modul fungsi agak bebas, memudahkan penyelenggaraan dan pengoptimuman.

- Sokongan Ujian Semula Lengkap: Menyediakan tetapan parameter ujian semula terperinci, menyokong pengesahan data sejarah.

Risiko Strategi

- Risiko Kebergantungan Isyarat: Strategi sangat bergantung kepada kualiti isyarat penunjuk LuxAlgo®.

- Risiko Kesesuaian Persekitaran Pasaran: Prestasi strategi mungkin berbeza dengan ketara dalam persekitaran pasaran yang berbeza.

- Risiko Kepekaan Parameter: Gabungan pelbagai keadaan keluar boleh menyebabkan keluar terlalu awal atau terlepas peluang.

- Risiko Kecairan: Apabila kecairan pasaran tidak mencukupi, ia mungkin menjejaskan pelaksanaan masuk dan keluar.

- Risiko Pelaksanaan Teknikal: Perlu memastikan operasi stabil penunjuk dan strategi untuk mengelakkan kegagalan teknikal.

Arah Pengoptimuman Strategi

- Pengoptimuman Sistem Isyarat:

- Memperkenalkan lebih banyak penunjuk teknikal untuk pengesahan isyarat.

- Membangunkan mekanisme pelarasan ambang isyarat adaptif.

- Peningkatan Kawalan Risiko:

- Menambah mekanisme henti rugi adaptif berdasarkan volatiliti.

- Membangunkan sistem pengurusan kedudukan dinamik.

- Pengoptimuman Prestasi:

- Mengoptimumkan kecekapan pengiraan, mengurangkan penggunaan sumber.

- Memperbaiki logik pemprosesan isyarat untuk mengurangkan kependaman.

- Peluasan Fungsi:

- Menambah lebih banyak alat analisis persekitaran pasaran.

- Membangunkan rangka kerja pengoptimuman parameter yang lebih fleksibel.

Kesimpulan

Strategi ini menyediakan penyelesaian lengkap untuk perdagangan kuantitatif dengan menggabungkan isyarat berkualiti tinggi LuxAlgo® dan sistem pengurusan risiko pelbagai lapisan. Reka bentuk modular dan pilihan konfigurasi yang fleksibel memberikan kebolehsuaian dan kebolehkembangan yang baik. Walaupun terdapat beberapa risiko yang wujud, melalui pengoptimuman dan penambahbaikan berterusan, prestasi keseluruhan strategi masih mempunyai ruang peningkatan yang besar. Cadangan kepada pengguna supaya memberi perhatian kepada perubahan persekitaran pasaran dalam aplikasi sebenar, melaraskan tetapan parameter pada masa yang sesuai, dan sentiasa memantau risiko.

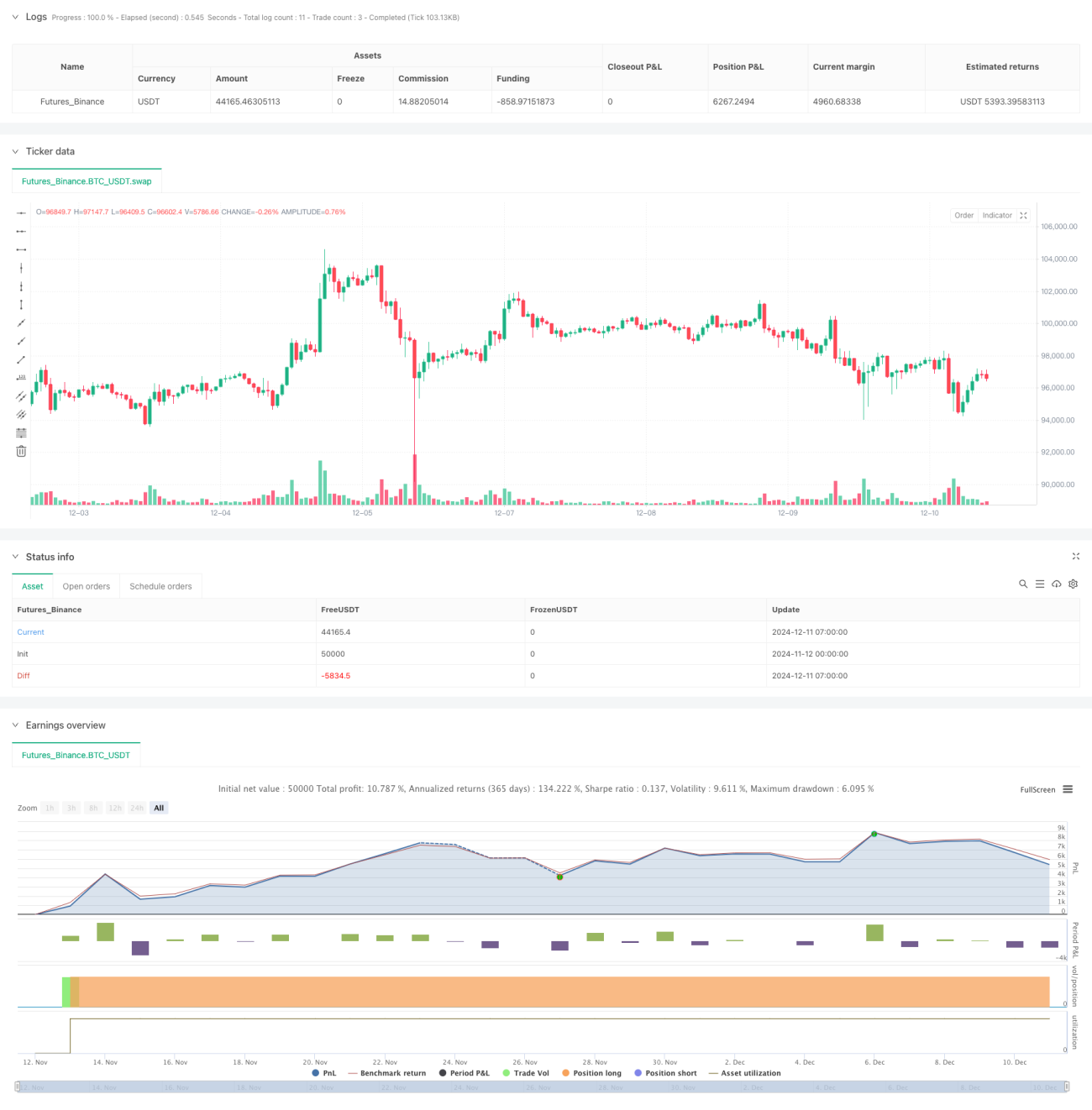

/*backtest

start: 2024-11-12 00:00:00

end: 2024-12-11 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Chart0bserver

// This strategy is NOT from the LuxAlgo® developers. We created this to compliment their hard work. No association with LuxAlgo® is intended nor implied.

- 1