Strategi Pengoptimuman Momentum Aliran Dinamik Digabungkan dengan Indikator Saluran G

Gambaran Keseluruhan

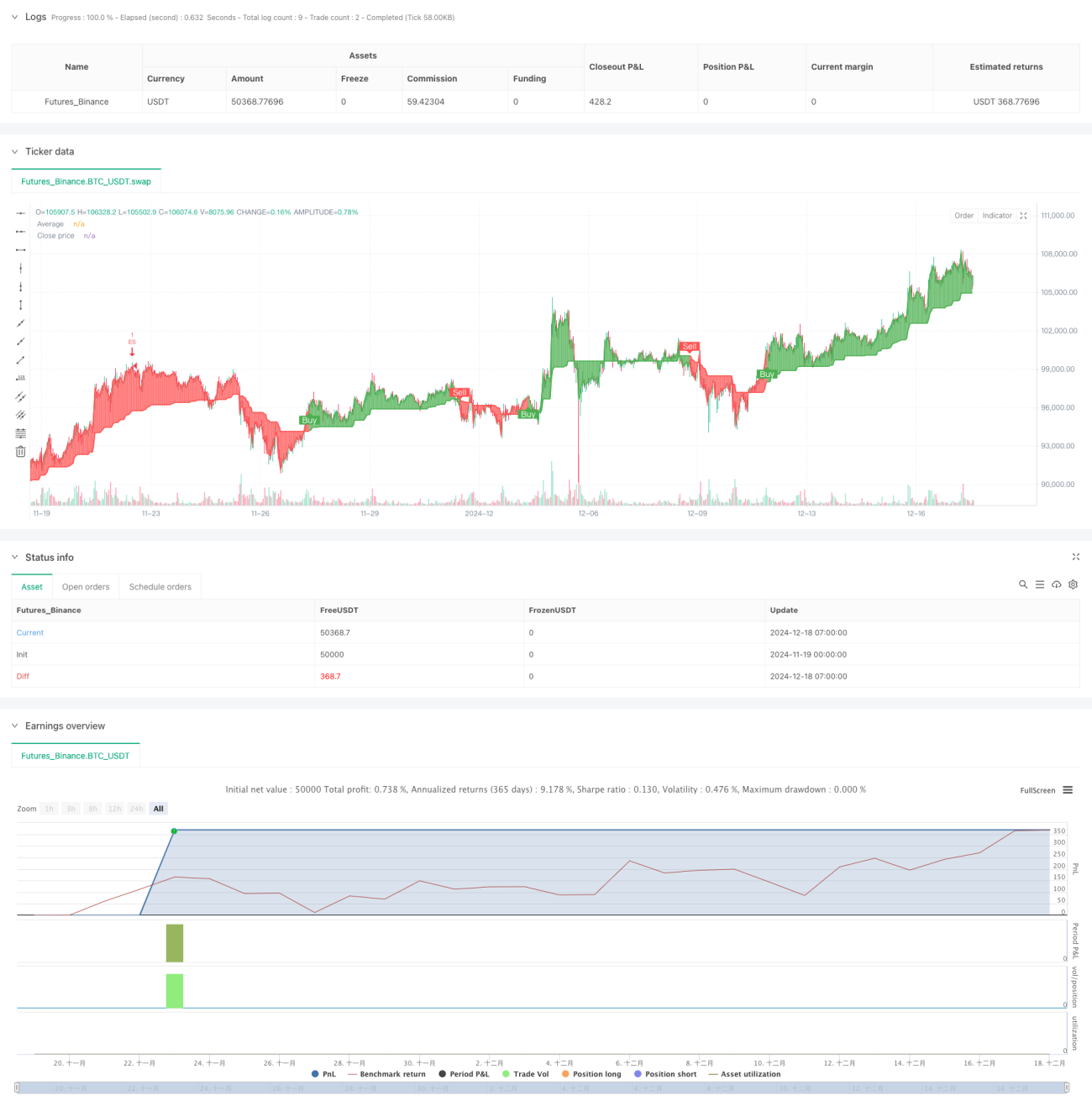

Strategi ini ialah sistem perdagangan tren lanjutan yang menggabungkan indikator G-Channel, RSI dan MACD. Ia mengira zon sokongan dan rintangan secara dinamik, digabungkan dengan indikator momentum untuk mengenal pasti peluang perdagangan berkebarangkalian tinggi. Inti strategi adalah menggunakan indikator G-Channel tersuai untuk menentukan arah aliran pasaran, sementara menggunakan RSI dan MACD untuk mengesahkan perubahan momentum, menjana isyarat perdagangan yang lebih tepat.

Prinsip Strategi

Strategi menggunakan mekanisme penapisan tiga lapis untuk memastikan kebolehpercayaan isyarat perdagangan. Pertama, G-Channel membina zon sokongan dan rintangan secara dinamik dengan mengira harga tertinggi dan terendah dalam tempoh tertentu. Apabila harga menembusi saluran, sistem mengenal pasti titik perubahan arah aliran yang berpotensi. Kedua, indikator RSI digunakan untuk mengesahkan sama ada pasaran berada dalam keadaan terlebih beli atau terlebih jual, membantu menyaring peluang perdagangan yang lebih bernilai. Akhir sekali, indikator MACD mengesahkan arah dan kekuatan momentum melalui nilai positif dan negatif histogram. Hanya apabila ketiga-tiga syarat ini dipenuhi, sistem akan mengeluarkan isyarat perdagangan.

Kelebihan Strategi

- Mekanisme pengesahan isyarat pelbagai dimensi meningkatkan ketepatan perdagangan dengan ketara

- Penetapan henti rugi dan ambil untung secara dinamik, mengawal risiko dengan berkesan

- Sifat penyesuaian G-Channel membolehkan strategi menyesuaikan diri dengan pelbagai keadaan pasaran

- Sistem pengurusan risiko yang lengkap, termasuk pengurusan kedudukan dan pengurusan modal

- Sistem label visual memaparkan isyarat perdagangan secara intuitif, memudahkan analisis dan pengoptimuman

Risiko Strategi

- Dalam pasaran yang bergerak tidak menentu, mungkin menghasilkan isyarat palsu, memerlukan pengenalpastian keadaan pasaran

- Pengoptimuman parameter yang berlebihan boleh menyebabkan risiko overfitting

- Pelbagai indikator mungkin menghasilkan kesan ketinggalan semasa tempoh turun naik tinggi

- Penetapan henti rugi yang tidak betul boleh menyebabkan penarikan balik yang besar

Arah Pengoptimuman Strategi

- Memperkenalkan modul pengenalpastian keadaan pasaran, menggunakan tetapan parameter yang berbeza dalam keadaan pasaran yang berbeza

- Membangunkan mekanisme henti rugi adaptif, melaraskan tahap henti rugi secara dinamik berdasarkan turun naik pasaran

- Menambah indikator analisis volum dagangan untuk meningkatkan kebolehpercayaan isyarat

- Mengoptimumkan kaedah pengiraan G-Channel untuk mengurangkan kesan ketinggalan

Kesimpulan

Strategi ini membina sistem perdagangan yang lengkap dengan menggunakan pelbagai indikator teknikal secara menyeluruh. Kelebihan utamanya terletak pada mekanisme pengesahan isyarat pelbagai dimensi dan sistem pengurusan risiko yang mantap. Dengan pengoptimuman dan penambahbaikan berterusan, strategi ini dijangka dapat mengekalkan prestasi yang stabil dalam pelbagai keadaan pasaran. Adalah disarankan agar pedagang menguji pelbagai kombinasi parameter sepenuhnya sebelum dagangan sebenar, dan membuat pelarasan yang sesuai berdasarkan ciri pasaran khusus.

/*backtest

start: 2024-11-19 00:00:00

end: 2024-12-18 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("VinSpace Optimized Strategy", shorttitle="VinSpace Magic", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// Input Parameters- 1