Strategi Dagangan Dinamik Adaptif berdasarkan Log Pulangan Piawai

Gambaran Keseluruhan

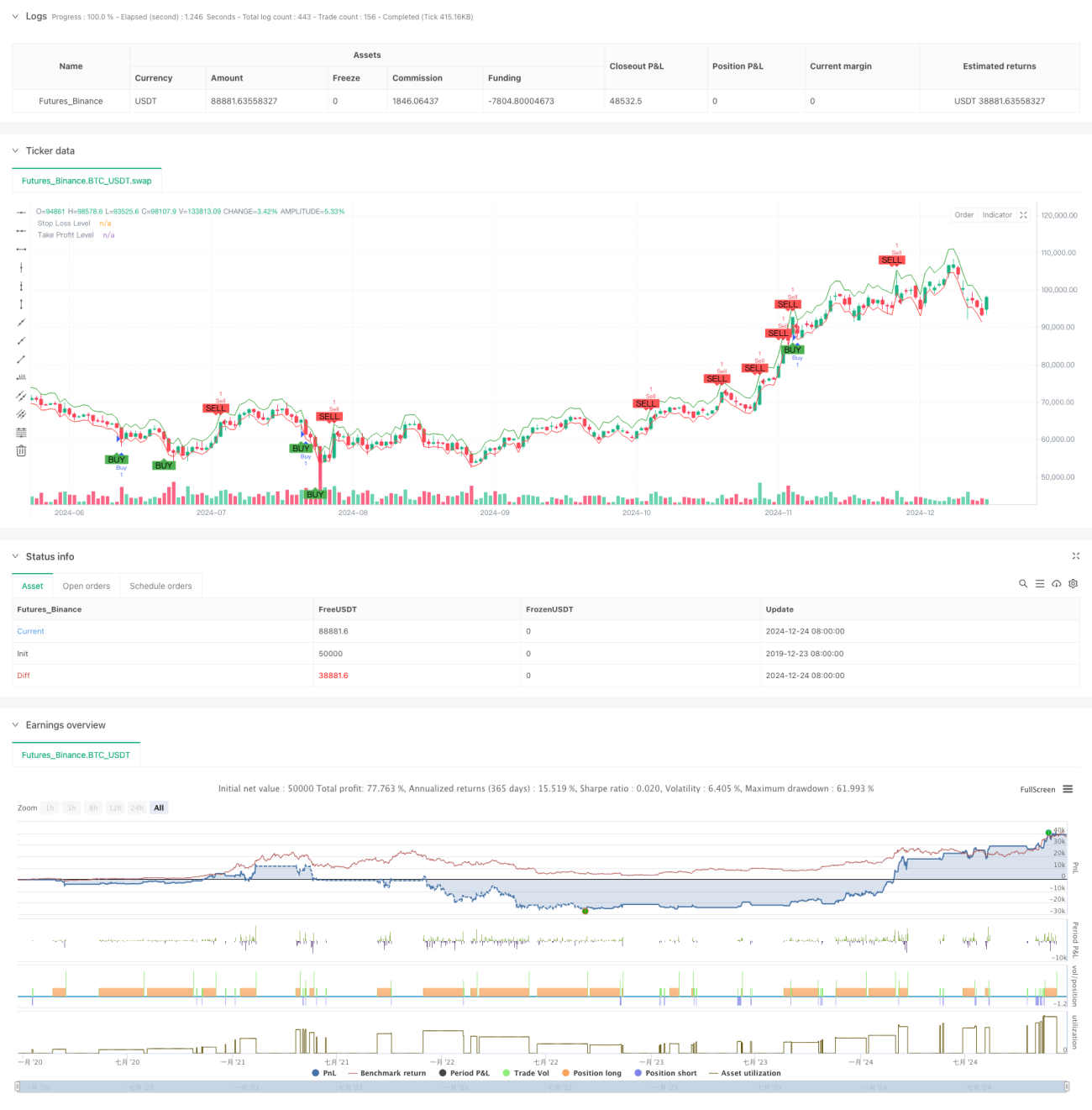

Strategi ini adalah sistem perdagangan adaptif berdasarkan Indeks Shiryaev-Zhou (SZI). Ia mengenal pasti keadaan terlebih beli dan terlebih jual pasaran dengan mengira skor piawai pulangan log, sekali gus meraih peluang revert min harga. Strategi ini menggabungkan stop loss dan sasaran untung dinamik untuk kawalan risiko yang tepat.

Prinsip Strategi

Teras strategi ini adalah membina penunjuk piawai melalui ciri statistik gelongsor pulangan log. Langkah-langkah khusus adalah seperti berikut:

- Kira pulangan log untuk menormalkan taburan pulangan.

- Gunakan tetingkap 50 tempoh untuk mengira min gelongsor dan sisihan piawai.

- Bina penunjuk SZI: (Pulangan log - Min gelongsor) / Sisihan piawai gelongsor.

- Apabila SZI di bawah -2.0, isyarat beli dijana; apabila melebihi 2.0, isyarat jual dijana.

- Tetapkan tahap stop loss sebanyak 2% dan take profit sebanyak 4% berdasarkan harga masuk.

Kelebihan Strategi

- Asas teori kukuh: Berdasarkan andaian taburan normal log, disokong oleh statistik yang baik.

- Kebolehsuaian tinggi: Melalui pengiraan tetingkap gelongsor, mampu menyesuaikan dengan perubahan ciri turun naik pasaran.

- Kawalan risiko lengkap: Menggunakan strategi stop loss peratusan, membolehkan kawalan tepat risiko setiap dagangan.

- Mesra visualisasi: Menandakan isyarat dagangan dan tahap kawalan risiko dengan jelas pada carta.

Risiko Strategi

- Kepekaan parameter: Panjang tetingkap gelongsor dan pilihan ambang mempengaruhi prestasi strategi secara signifikan.

- Kebergantungan pada persekitaran pasaran: Dalam pasaran bertrend, mungkin menghasilkan isyarat palsu yang kerap.

- Kesan gelinciran: Semasa tempoh turun naik melampau, harga pelaksanaan sebenar mungkin menyimpang ketara dari paras ideal.

- Kelewatan pengiraan: Pengiraan penunjuk statistik masa nyata mungkin menghasilkan sedikit kelewatan isyarat.

Arah Pengoptimuman Strategi

- Ambang dinamik: Boleh mempertimbangkan untuk melaraskan ambang isyarat secara dinamik berdasarkan turun naik pasaran.

- Pelbagai jangka masa: Memperkenalkan mekanisme pengesahan isyarat dari pelbagai jangka masa.

- Penapisan turun naik: Menghentikan dagangan atau menyesuaikan saiz kedudukan semasa turun naik melampau.

- Pengesahan isyarat: Menambah penunjuk bantuan seperti volum dagangan dan momentum untuk mengesahkan isyarat.

- Pengurusan kedudukan: Melaksanakan pengurusan kedudukan dinamik berdasarkan turun naik.

Kesimpulan

Ini adalah strategi perdagangan kuantitatif yang dibina atas asas statistik yang kukuh, menangkap peluang pergerakan harga melalui pulangan log piawai. Kelebihan utama strategi ini adalah kebolehsuaian dan kawalan risiko yang lengkap, namun masih ada ruang pengoptimuman dalam pemilihan parameter dan kebolehsuaian terhadap persekitaran pasaran. Dengan memperkenalkan ambang dinamik dan mekanisme pengesahan isyarat pelbagai dimensi, kestabilan dan kebolehpercayaan strategi dijangka dapat ditingkatkan lagi.

- 1