Sistem Perdagangan Trend Persilangan Pelbagai Purata Bergerak dengan Sokongan Rintangan Camarilla

Gambaran Keseluruhan

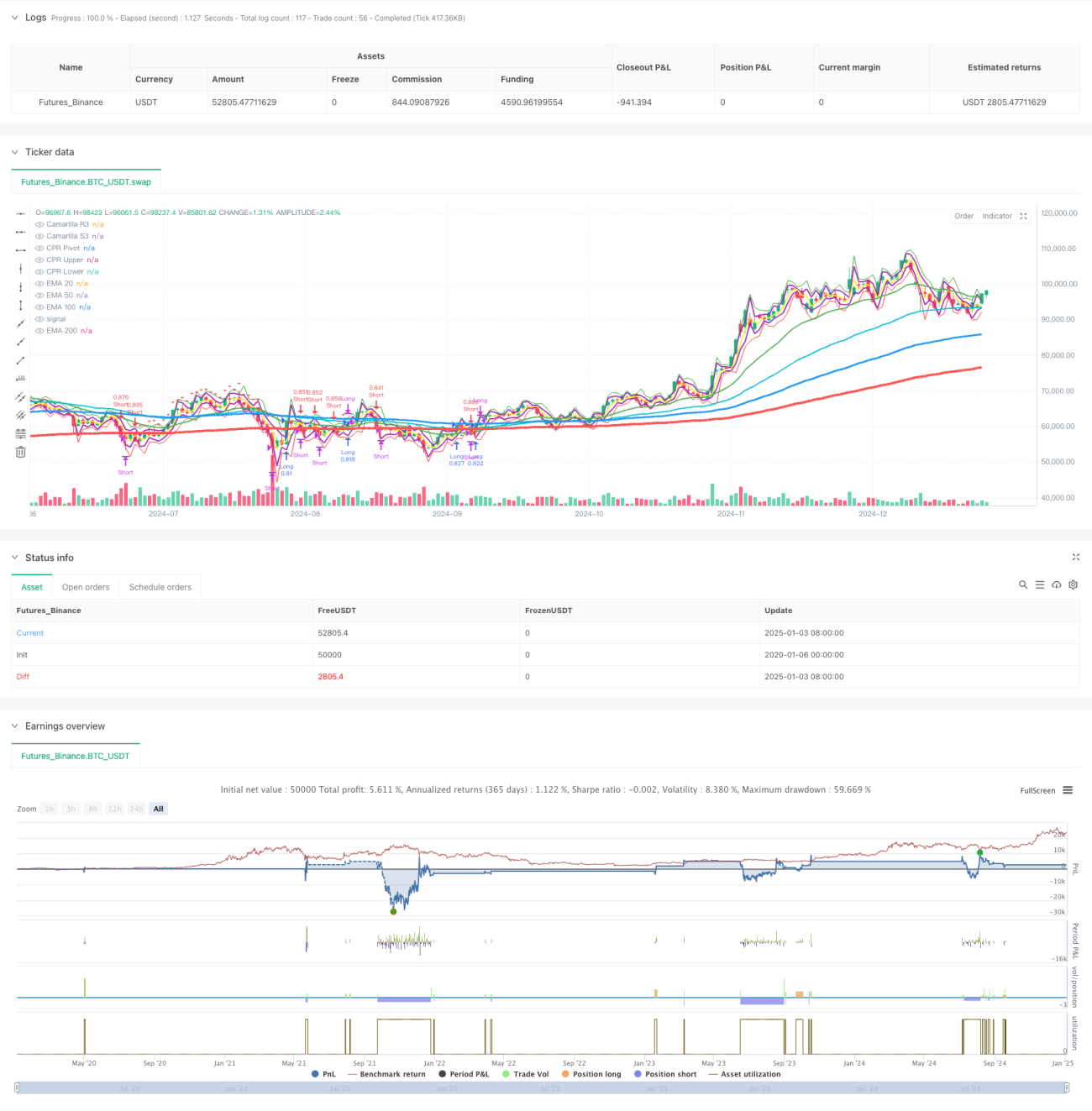

Strategi ini merupakan sistem perdagangan yang menggabungkan pelbagai purata pergerakan eksponen (EMA), tahap sokongan dan rintangan Camarilla, serta julat pangsi (CPR). Strategi ini mengenal pasti arah aliran pasaran dan peluang perdagangan yang berpotensi dengan menganalisis hubungan harga dengan beberapa purata pergerakan serta julat harga penting. Sistem ini menggunakan langkah pengurusan risiko dan kawalan modal yang ketat, termasuk saiz kedudukan berdasarkan peratusan dan mekanisme keluar yang pelbagai.

Prinsip Strategi

Strategi ini berasaskan beberapa komponen teras berikut:

- Sistem purata pergerakan berganda (EMA20/50/100/200) untuk mengesahkan arah dan kekuatan trend.

- Tahap sokongan dan rintangan Camarilla (R3/S3) untuk mengenal pasti tahap harga kritikal.

- Julat pangsi (CPR) untuk menentukan julat dagangan intrahari.

- Isyarat masuk berdasarkan persilangan harga dengan EMA200 dan pengesahan EMA20.

- Strategi keluar merangkumi dua mod: titik tetap dan pergerakan peratusan.

- Sistem pengurusan modal menyesuaikan saiz kedudukan secara dinamik berdasarkan saiz akaun.

Kelebihan Strategi

- Gabungan penunjuk teknikal pelbagai dimensi menyediakan isyarat dagangan yang lebih boleh dipercayai.

- Mekanisme keluar yang fleksibel menyesuaikan diri dengan pelbagai keadaan pasaran.

- Sistem pengurusan modal yang lengkap mengawal risiko dengan berkesan.

- Ciri pengesanan arah aliran membantu menangkap pergerakan pasaran yang besar.

- Komponen visual memudahkan pedagang memahami struktur pasaran.

Risiko Strategi

- Mungkin menjana isyarat palsu dalam pasaran yang tidak menentu.

- Pelbagai penunjuk boleh menyebabkan kelewatan isyarat perdagangan.

- Titik keluar tetap mungkin menunjukkan prestasi yang kurang baik dalam pasaran yang sangat tidak menentu.

- Memerlukan modal yang besar untuk menanggung pengeluaran.

- Kos dagangan boleh menjejaskan keuntungan keseluruhan strategi.

Arah Pengoptimuman Strategi

- Memperkenalkan penunjuk turun naik untuk melaraskan parameter masuk dan keluar secara dinamik.

- Menambah modul pengenalpastian keadaan pasaran untuk menyesuaikan diri dengan pelbagai persekitaran pasaran.

- Mengoptimumkan sistem pengurusan modal dengan menambah pengurusan kedudukan dinamik.

- Menambah penapis masa dagangan untuk meningkatkan kualiti isyarat.

- Mempertimbangkan untuk menambah analisis volum bagi meningkatkan kebolehpercayaan isyarat.

Ringkasan

Strategi ini membina sistem perdagangan yang lengkap dengan mengintegrasikan beberapa alat analisis teknikal klasik. Kelebihan sistem ini terletak pada analisis pasaran pelbagai dimensi dan pengurusan risiko yang ketat, tetapi perlu juga memberi perhatian kepada kebolehsuaian dalam pelbagai persekitaran pasaran. Melalui pengoptimuman dan penambahbaikan yang berterusan, strategi ini dijangka dapat meningkatkan keuntungan sambil mengekalkan kestabilan.

- 1