Ini adalah strategi perdagangan momentum komprehensif berdasarkan isyarat persilangan purata bergerak berbilang dan indikator harga volum. Strategi ini menjana isyarat perdagangan melalui gabungan beberapa indikator seperti persilangan purata pergerakan eksponen (EMA) pantas dan perlahan, harga purata wajaran volum (VWAP) dan SuperTrend, serta menggabungkan syarat seperti tetingkap masa perdagangan dalam hari dan julat perubahan harga untuk mengawal kemasukan dan keluar.

Prinsip Strategi

Strategi menggunakan EMA 5 hari dan 13 hari sebagai indikator utama penentuan arah aliran. Apabila EMA pantas menembusi ke atas EMA perlahan dan harga penutup berada di atas VWAP, isyarat beli (long) dijana; apabila EMA pantas menembusi ke bawah EMA perlahan dan harga penutup berada di bawah VWAP, isyarat jual (short) dijana. Pada masa yang sama, strategi juga memperkenalkan indikator SuperTrend sebagai pengesahan arah aliran dan asas untuk henti rugi. Strategi menetapkan syarat kemasukan yang berbeza untuk hari perdagangan yang berbeza, termasuk perubahan harga berbanding harga penutup hari sebelumnya, julat turun naik antara harga tertinggi dan terendah hari semasa, dan lain-lain.

Kelebihan Strategi

- Penggunaan gabungan pelbagai indikator teknikal meningkatkan kebolehpercayaan isyarat perdagangan.

- Syarat kemasukan yang berbeza untuk hari perdagangan yang berbeza membolehkan penyesuaian yang lebih baik dengan ciri pasaran.

- Mekanisme ambil untung dan henti rugi dinamik dapat mengawal risiko dengan berkesan.

- Gabungan had tetingkap masa perdagangan dalam hari mengurangkan risiko semasa tempoh turun naik tinggi.

- Sekatan melalui paras tinggi/rendah sebelumnya dan julat turun naik harga mengurangkan risiko membeli pada paras tertinggi dan menjual pada paras terendah.

Risiko Strategi

- Dalam keadaan pasaran yang bergerak pantas, isyarat palsu mungkin timbul.

- Pada awal pembalikan arah aliran, mungkin berlaku kelewatan.

- Pengoptimuman parameter mungkin menghadapi risiko overfitting.

- Kos perdagangan boleh menjejaskan keuntungan strategi.

- Semasa tempoh turun naik pasaran yang tinggi, mungkin menghadapi pengeluaran yang besar.

Arah Pengoptimuman Strategi

- Boleh mempertimbangkan untuk memperkenalkan indikator analisis volum untuk mengesahkan kekuatan arah aliran dengan lebih lanjut.

- Mengoptimumkan tetapan parameter untuk hari perdagangan yang berbeza bagi meningkatkan kebolehsuaian strategi.

- Menambah lebih banyak indikator sentimen pasaran untuk meningkatkan ketepatan ramalan.

- Menyempurnakan mekanisme ambil untung dan henti rugi untuk meningkatkan kecekapan penggunaan modal.

- Mempertimbangkan untuk menambah indikator turun naik untuk mengoptimumkan pengurusan saiz kedudukan.

Kesimpulan

Strategi ini mencapai gabungan penjejakan arah aliran dan perdagangan momentum melalui penggunaan menyeluruh pelbagai indikator teknikal. Reka bentuk strategi mengambil kira kepelbagaian pasaran dan menggunakan peraturan perdagangan yang berbeza untuk hari perdagangan yang berbeza. Melalui kawalan risiko yang ketat dan mekanisme ambil untung dan henti rugi yang fleksibel, strategi ini menunjukkan nilai aplikasi praktikal yang baik. Pada masa hadapan, kestabilan dan keuntungan strategi boleh ditingkatkan dengan memperkenalkan lebih banyak indikator teknikal dan mengoptimumkan tetapan parameter.

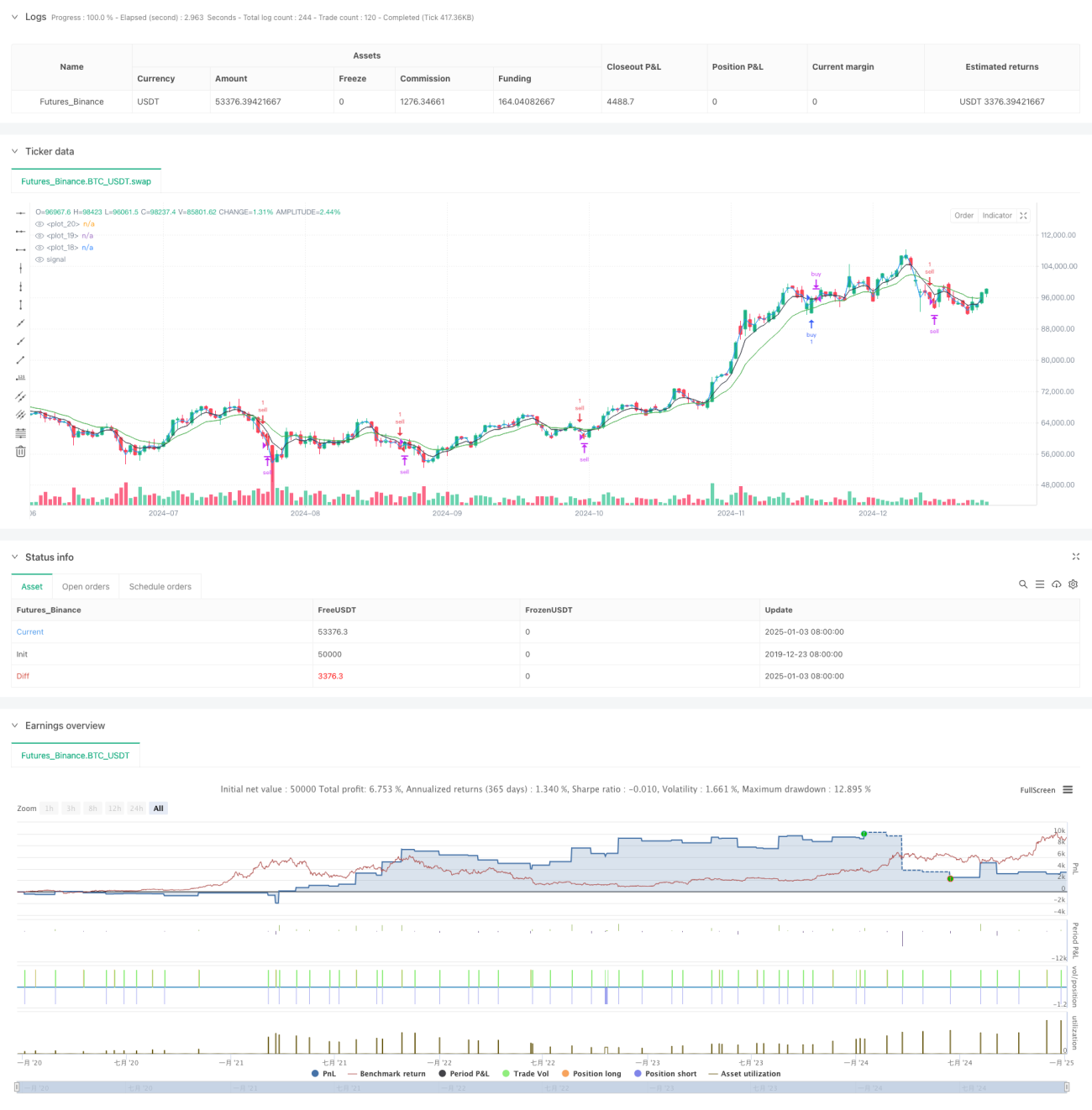

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

//@version=6

strategy("S1", overlay=true)

fastEMA = ta.ema(close, 5)- 1