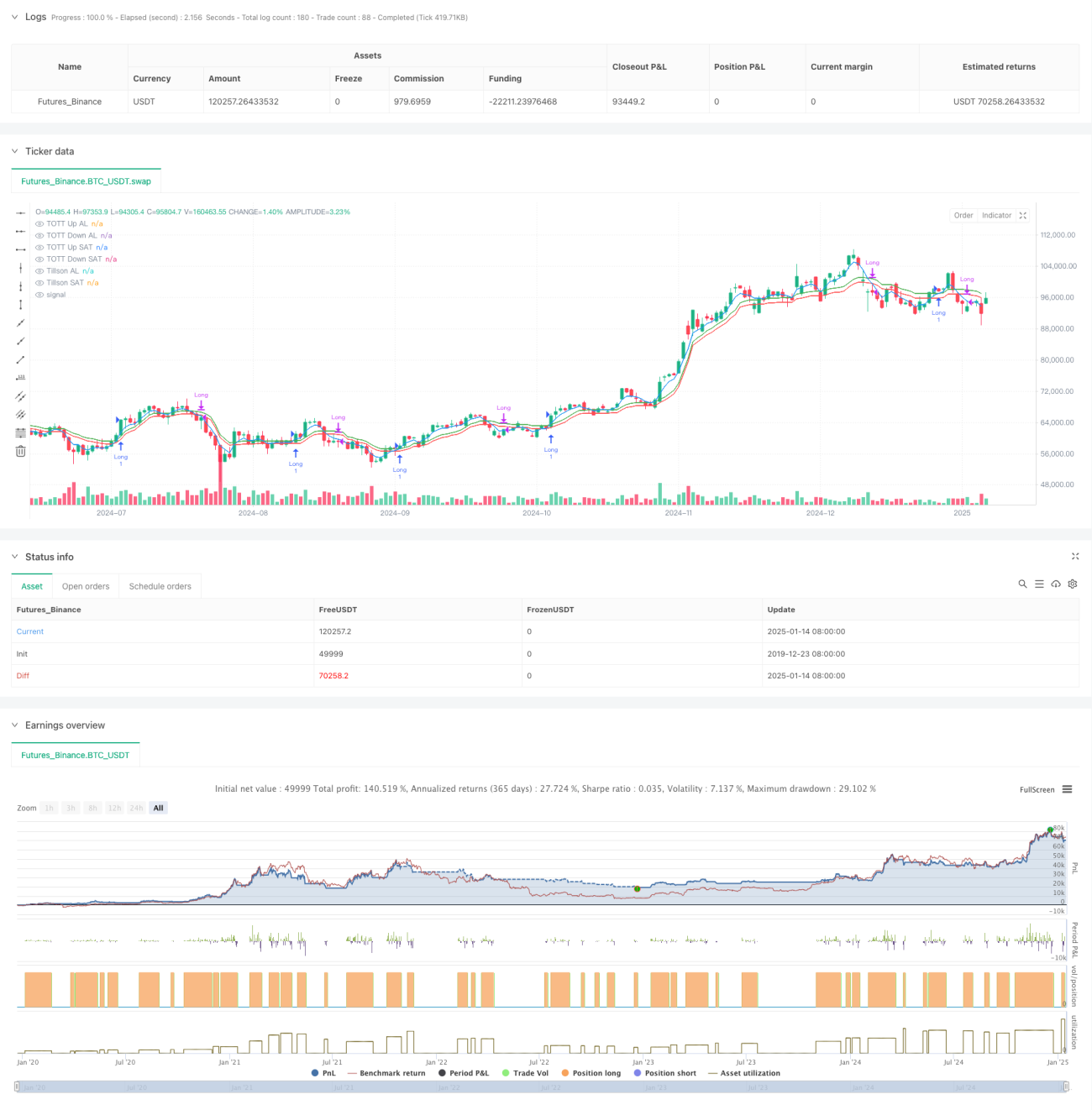

Gambaran Keseluruhan

Strategi ini adalah sistem pengesanan arah aliran berdasarkan penunjuk Tillson T3 dan Pengesan Trend Dioptimumkan Berganda (TOTT). Ia mengoptimumkan penjanaan isyarat dagangan dengan menggabungkan pengayun momentum Williams %R. Strategi ini menggunakan tetapan parameter beli dan jual yang berasingan, membolehkan pelarasan kepekaan yang fleksibel mengikut keadaan pasaran yang berbeza, meningkatkan kebolehsuaian strategi.

Prinsip Strategi

Strategi ini terdiri daripada tiga komponen teras:

- Penunjuk Tillson T3 - ini adalah varian Purata Pergerakan Eksponen (EMA) yang dioptimumkan, menghasilkan garis arah aliran yang lebih licin melalui pengiraan EMA berwajaran berganda.

- Pengesan Trend Dioptimumkan Berganda (TOTT) - alat pengesanan arah aliran yang menyesuaikan secara adaptif berdasarkan tingkah laku harga dan pekali turun naik, mengira jalur atas dan bawah di bawah keadaan beli dan jual.

- Penunjuk Williams %R - pengayun momentum yang digunakan untuk mengenal pasti keadaan terlebih beli dan terlebih jual.

Logik penjanaan isyarat dagangan:

- Keadaan beli: Apabila garis T3 menembusi jalur atas TOTT dan Williams %R lebih besar daripada -20 (terlebih jual)

- Keadaan jual: Apabila garis T3 menembusi ke bawah jalur bawah TOTT dan Williams %R lebih besar daripada -70

Kelebihan Strategi

- Kestabilan isyarat yang kuat - melalui pemprosesan pelicinan berganda penunjuk T3, risiko penembusan palsu dapat dikurangkan dengan berkesan

- Kebolehsuaian yang baik - reka bentuk parameter beli dan jual yang berasingan membolehkan pengoptimuman bebas untuk keadaan pasaran yang berbeza

- Kawalan risiko yang lengkap - menggabungkan Williams %R sebagai pengesahan kedua, meningkatkan kebolehpercayaan dagangan

- Visualisasi yang jelas - strategi menyediakan sokongan visualisasi carta yang komprehensif, memudahkan analisis dan penilaian

Risiko Strategi

- Kelewatan pembalikan arah aliran - pelicinan berganda penunjuk T3 boleh menyebabkan kelewatan isyarat

- Tidak sesuai untuk pasaran berayun - dalam fasa pengukuhan sisi, mungkin menghasilkan terlalu banyak isyarat dagangan

- Kepekaan parameter yang tinggi - memerlukan pelarasan parameter yang kerap untuk persekitaran pasaran yang berbeza

Cadangan kawalan risiko:

- Memperkenalkan mekanisme henti rugi

- Menetapkan had volum dagangan

- Menambah penapis pengesahan arah aliran

Arah Pengoptimuman Strategi

- Pengoptimuman parameter dinamik - membangunkan mekanisme pelarasan parameter adaptif

- Menambah pengiktirafan persekitaran pasaran - memperkenalkan penunjuk kekuatan arah aliran

- Menambah baik pengurusan risiko - menambah henti rugi dan ambil untung dinamik

- Meningkatkan penapisan isyarat - menyepadukan lebih banyak penunjuk teknikal untuk pengesahan

Kesimpulan

Ini adalah strategi pengesanan arah aliran yang berstruktur lengkap dan logik yang jelas. Melalui gabungan penunjuk T3 dan TOTT, serta penapisan Williams %R, strategi ini menunjukkan prestasi cemerlang dalam pasaran yang mempunyai arah aliran. Walaupun terdapat sedikit kelewatan, melalui pengoptimuman parameter dan penambahbaikan pengurusan risiko, strategi ini mempunyai nilai praktikal dan ruang pengembangan yang baik.

- 1