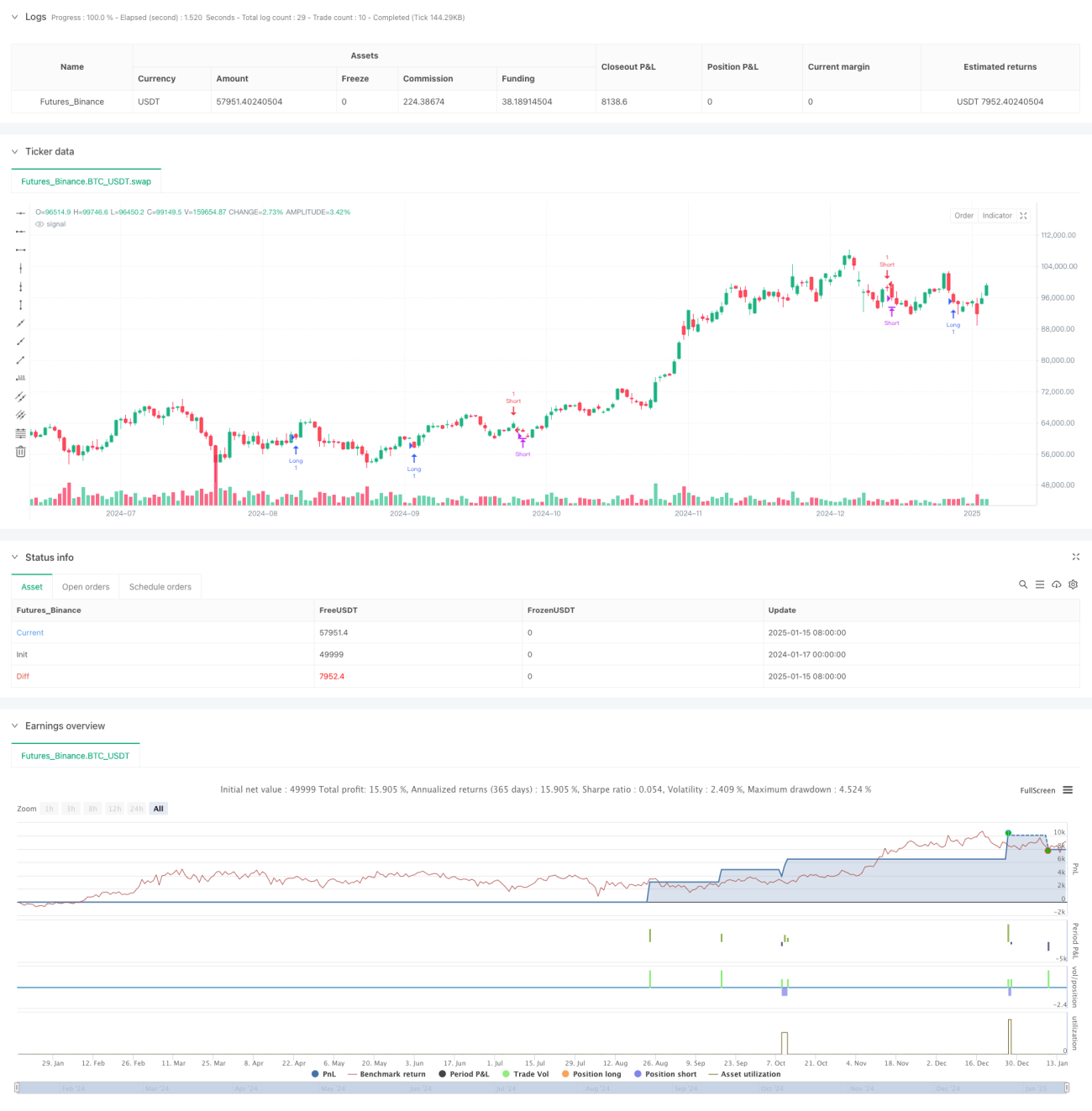

Sistem Strategi Kuantitatif Momentum Trend Dua Penunjuk

Gambaran Keseluruhan

Strategi ini merupakan sistem perdagangan kuantitatif yang menggabungkan Indeks Kekuatan Relatif (RSI) dan Purata Bergerak (MA), menggunakan sinergi kedua-dua indikator untuk mengenal pasti arah aliran pasaran dan peluang perdagangan. Sistem ini juga mengintegrasikan penapis volum dan turun naik untuk meningkatkan kebolehpercayaan isyarat perdagangan. Idea utama strategi adalah untuk menentukan arah aliran melalui persilangan purata bergerak cepat dan purata bergerak perlahan, sambil menggunakan RSI untuk mengesahkan momentum, seterusnya membentuk rangka kerja keputusan perdagangan yang lengkap.

Prinsip Strategi

Strategi ini menggunakan mekanisme pengesahan isyarat dua lapis:

- Lapisan Pengesahan Trend: Menggunakan persilangan Purata Bergerak Cepat (FastMA) dan Purata Bergerak Perlahan (SlowMA) untuk menilai arah aliran pasaran. Apabila garis cepat menembusi garis perlahan dari bawah, ia dianggap sebagai pengesahan arah aliran menaik; apabila garis cepat jatuh di bawah garis perlahan dari atas, ia dianggap sebagai pengesahan arah aliran menurun.

- Lapisan Pengesahan Momentum: Menggunakan indikator RSI sebagai alat pengesahan momentum. Dalam arah aliran menaik, RSI dikehendaki di bawah 50, menunjukkan pasaran masih mempunyai ruang untuk kenaikan; dalam arah aliran menurun, RSI dikehendaki di atas 50, menunjukkan pasaran masih mempunyai ruang untuk penurunan.

- Penapis Perdagangan: Dengan menetapkan ambang minimum bagi volum dan turun naik ATR, isyarat perdagangan yang tidak mempunyai kecairan atau turun naik yang mencukupi akan ditapis.

Kelebihan Strategi

- Pengesahan Isyarat Pelbagai Dimensi: Dengan menggabungkan indikator trend dan momentum, kebarangkalian isyarat palsu dikurangkan.

- Pengurusan Risiko Lengkap: Mengintegrasikan fungsi henti rugi dan ambil untung, membolehkan penetapan titik kawalan risiko berdasarkan peratusan.

- Mekanisme Penapis Fleksibel: Penapis volum dan turun naik boleh diaktifkan atau dinyahaktifkan mengikut keadaan pasaran.

- Mekanisme Tutup Automatik: Apabila isyarat pembalikan dikesan, kedudukan akan ditutup secara automatik untuk mengelakkan pegangan berlebihan.

Risiko Strategi

- Risiko Pasaran Tidak Menentu: Dalam pasaran yang bergerak mendatar, isyarat penembusan palsu mungkin kerap berlaku.

- Risiko Gelinciran: Apabila pasaran berubah secara mendadak, harga pelaksanaan sebenar mungkin menyimpang jauh daripada harga pencetus isyarat.

- Kepekaan Parameter: Keberkesanan strategi sangat bergantung pada penetapan parameter; persekitaran pasaran yang berbeza mungkin memerlukan kombinasi parameter yang berbeza.

Arah Pengoptimuman Strategi

- Pelarasan Parameter Dinamik: Memperkenalkan mekanisme parameter adaptif yang melaraskan tempoh purata bergerak dan ambang RSI secara dinamik berdasarkan turun naik pasaran.

- Sistem Wajaran Isyarat: Membina sistem pemarkahan kekuatan isyarat, memberikan wajaran berbeza berdasarkan prestasi indikator yang berbeza.

- Pengelasan Persekitaran Pasaran: Menambah modul pengenalpastian persekitaran pasaran, menggunakan strategi perdagangan yang berbeza dalam keadaan pasaran yang berbeza.

- Peningkatan Kawalan Risiko: Memperkenalkan mekanisme henti rugi dinamik yang melaraskan kedudukan henti rugi secara automatik berdasarkan turun naik pasaran.

Kesimpulan

Strategi ini membina sistem perdagangan yang agak lengkap dengan menggunakan indikator trend dan momentum secara menyeluruh. Kelebihan sistem terletak pada mekanisme pengesahan isyarat berlapis dan sistem pengurusan risiko yang komprehensif. Walau bagaimanapun, dalam aplikasi sebenar, perhatian perlu diberikan kepada kesan persekitaran pasaran terhadap prestasi strategi, dan pengoptimuman parameter perlu dilakukan berdasarkan situasi sebenar. Melalui penambahbaikan dan pengoptimuman berterusan, strategi ini dijangka dapat mengekalkan prestasi yang stabil dalam pelbagai persekitaran pasaran.

- 1