Strategi Ambil Untung Pelbagai Peringkat EMA-ADX untuk Pengesanan Trend Dinamik

Gambaran Keseluruhan

Strategi ini merupakan sistem dagangan pengikut trend yang menggabungkan indikator EMA dan ADX, dengan pengurusan modal dioptimumkan melalui pengambilan untung berperingkat dan stop loss bergerak. Strategi menggunakan purata bergerak EMA untuk menentukan arah trend, indikator ADX sebagai penapis kekuatan trend, dan mereka bentuk mekanisme pengambilan untung tiga lapisan untuk merealisasikan keuntungan secara berperingkat, sambil menggunakan ATR untuk melaras kedudukan stop loss secara dinamik bagi mengawal risiko.

Prinsip Strategi

Logik teras strategi merangkumi beberapa bahagian utama:

- Menggunakan EMA 50 tempoh untuk menentukan arah trend; harga menembusi ke atas EMA membuka posisi beli, menembusi ke bawah membuka posisi jual.

- Menapis trend lemah melalui indikator ADX 14 tempoh; apabila ADX > 20, trend disahkan sah.

- Mengira kedudukan stop loss dinamik berdasarkan ATR 14 tempoh; untuk posisi beli, harga terendah tolak 1 ATR; untuk posisi jual, harga tertinggi tambah 1 ATR.

- Menggunakan mekanisme pengambilan untung tiga lapisan:

- Lapisan pertama: 30% kedudukan mengambil untung pada 1 kali ATR.

- Lapisan kedua: 50% kedudukan mengambil untung pada 2 kali ATR.

- Lapisan ketiga: 20% kedudukan menggunakan pengambilan untung bergerak pada 3 kali ATR.

- Apabila harga mencapai kedudukan pengambilan untung lapisan kedua, semua baki kedudukan akan ditutup secara automatik.

Kelebihan Strategi

- Reka bentuk pengambilan untung berbilang lapisan dapat mengunci keuntungan tepat pada masanya tanpa terlepas pergerakan pasaran besar.

- Mekanisme stop loss bergerak dapat menyesuaikan diri dengan turun naik pasaran, memberikan kawalan risiko dinamik.

- Penapis ADX berkesan mengelakkan isyarat palsu dalam pasaran berayun.

- Persilangan harga dengan EMA memberikan isyarat masuk yang jelas.

- Pengambilan untung secara berperingkat mengurangkan turun naik emosi, membantu pelaksanaan strategi jangka panjang.

Risiko Strategi

- Dalam pasaran berayun, mungkin kerap masuk dan keluar menyebabkan peningkatan kos.

- EMA sebagai indikator ketinggalan mungkin tidak bertindak balas dengan cepat semasa pembalikan mendadak.

- Ambang ADX tetap mungkin perlu diselaraskan dalam persekitaran pasaran yang berbeza.

- Pengambilan untung berbilang lapisan mungkin mengurangkan kedudukan terlalu awal dalam trend sehala.

Langkah mitigasi:

- Ambang ADX boleh dilaraskan secara dinamik berdasarkan kitaran pasaran yang berbeza.

- Pertimbangkan untuk menambah indikator pengesahan trend.

- Lakukan pengoptimuman parameter yang lebih terperinci pada nisbah pengambilan untung.

Arah Pengoptimuman Strategi

- Memperkenalkan indikator volum untuk mengukuhkan pengesahan trend.

- Melaraskan ambang ADX secara dinamik mengikut turun naik pasaran.

- Mengoptimumkan nisbah peruntukan kedudukan bagi lapisan pengambilan untung.

- Menambah penggredan kekuatan trend yang sepadan dengan strategi pengambilan untung berbeza.

- Mempertimbangkan faktor bermusim dan penilaian kitaran pasaran.

Kesimpulan

Ini adalah strategi pengikut trend yang lengkap dari segi struktur dan jelas dari segi logik, mengimbangi pulangan dan risiko melalui pengambilan untung berperingkat dan stop loss dinamik. Reka bentuk strategi secara keseluruhan mematuhi prinsip asas perdagangan kuantitatif, mempunyai kebolehlanjutan dan ruang pengoptimuman yang baik. Dengan pelarasan parameter yang munasabah serta peningkatan dan pengoptimuman, strategi ini berpotensi untuk mengekalkan prestasi stabil dalam pelbagai persekitaran pasaran.

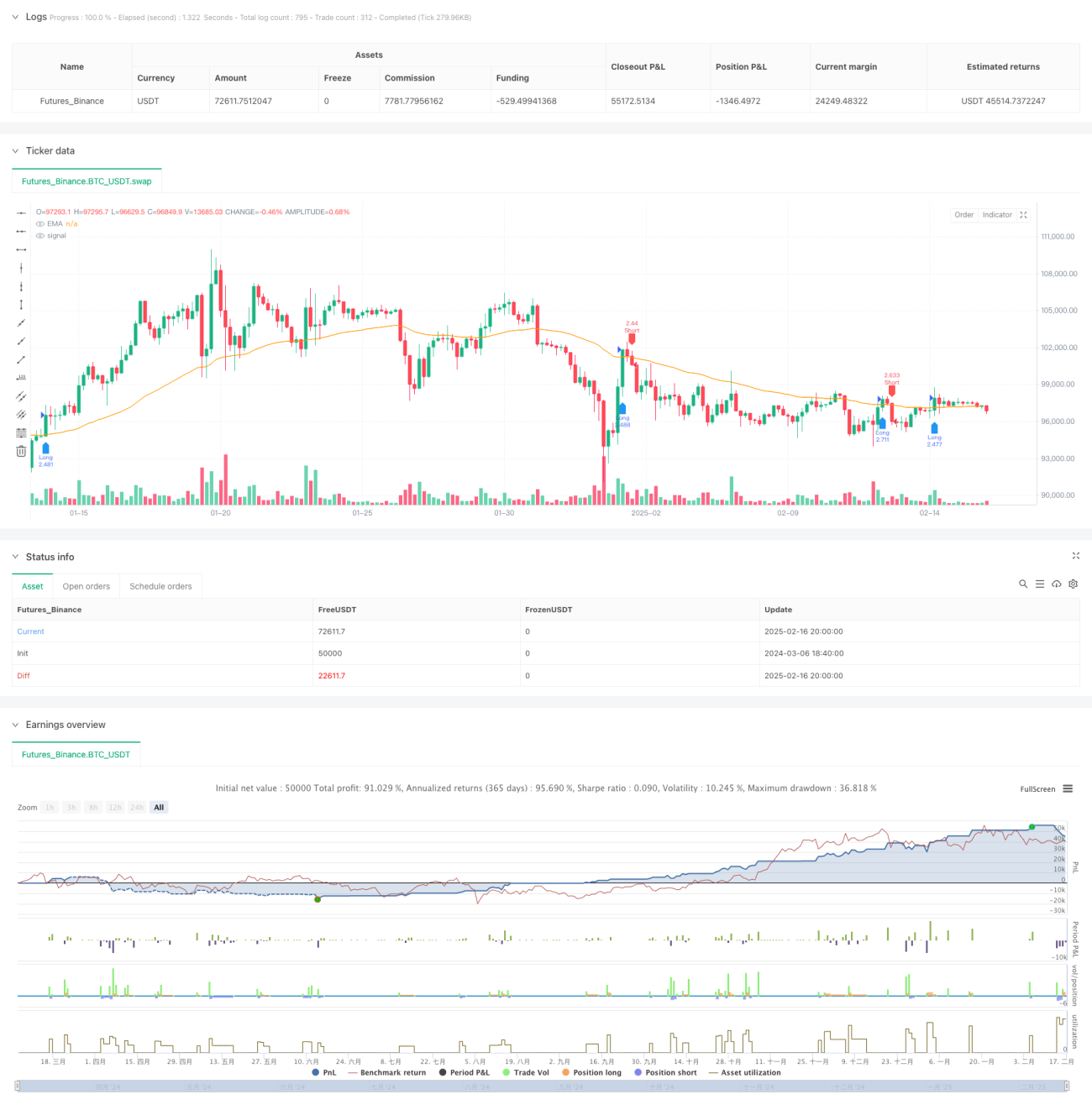

/*backtest

start: 2024-03-06 18:40:00

end: 2025-02-17 00:00:00

period: 4h

basePeriod: 4h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("BTC Optimized Strategy v6", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=250)

// === 參數設定 ===- 1